Expanded PVC Sheet Market Summary

Understanding Expanded PVC Sheets — Material Strengths Driving Adoption

Expanded PVC sheets are a class of closed-cell, lightweight, foam-like PVC boards prized for a blend of properties:

High strength-to-weight ratio

Excellent moisture and corrosion resistance

UV stability and durability for outdoor exposure

Ease of cutting, fabrication, and printing

Thermoformability and surface finish versatility

These properties make them ideal for a variety of applications from signage and displays to architectural interiors and light construction panels. The broader PVC foam sheet market — which overlaps significantly with expanded PVC — is valued in tens of billions of dollars globally, reflecting strong end-use demand across sectors such as building, automotive, and furniture & interior design.

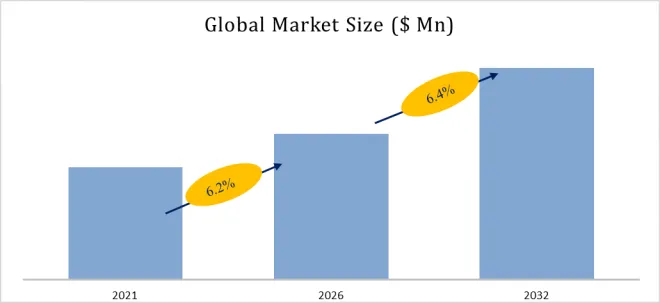

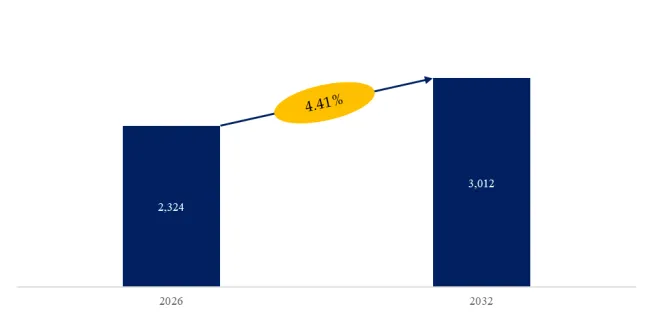

The global Expanded PVC Sheet market is on a steady growth path, with the market size expected to expand from approximately US$ 2.15 billion in 2025 to about US$ 3.01 billion by 2032, registering a compound annual growth rate (CAGR) of 4.41% from 2026 to 2032. This growth reflects the material’s expanding adoption in diversified end-use industries and its unique balance of performance and cost-effectiveness, even as the broader polymer sheet markets evolve under technological and sustainability pressures.

Figure00001. Global Expanded PVC Sheet Market Size (US$ million), 2026-2033

Above data is based on report from QYResearch: Global Expanded PVC Sheet Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Market Snapshot: Size, Growth & Competitive Landscape

2025 Market Size (Forecast): ~US$ 2.15 billion

2032 Market Size (Forecast): ~US$ 3.01 billion

Projected CAGR (2026-2032): 4.41%

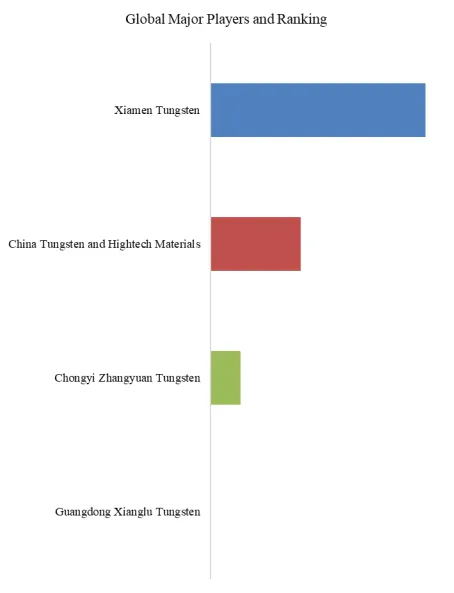

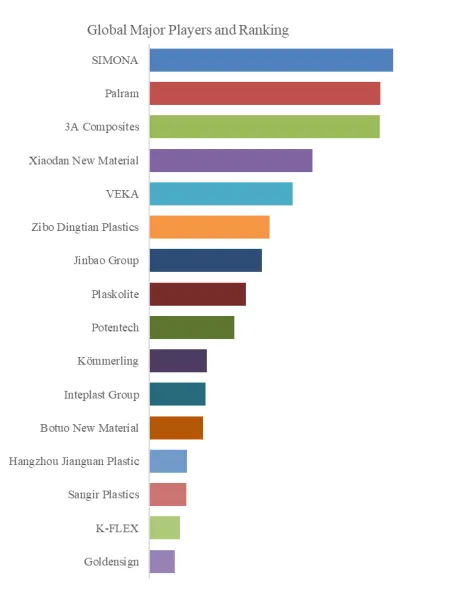

Top Players: SIMONA, Palram, 3A Composites, Xiaodan New Material, VEKA, Zibo Dingtian Plastics, Jinbao Group, Plaskolite, Potentech, Kömmerling, Inteplast Group, BoDo Plastics, Hangzhou Jianguan Plastic, Sangir Plastics, K-FLEX, Goldensign, etc.

Market Share (Top 5 Companies, 2025): ~12.21%

This landscape suggests a moderately fragmented global industry, where no single company dominates — creating room for specialization, regional champions, and technological differentiation.

Figure00002. Global Expanded PVC Sheet Top 16 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Expanded PVC Sheet Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Key Growth Drivers

1. Broad Sector Demand Across Industries

The expanded PVC sheet’s versatility underpins its broad adoption:

Construction & Building Materials: Lightweight partitions, ceiling panels, wall cladding.

Signage & Advertising: Weather-resistant, printable boards.

Furniture & Interiors: Moisture-resistant boards for shelves, cabinets, fixtures.

Transportation: Lightweight interior panels and trim components.

Demand is fueled by global trends in urbanization, infrastructure development, and lightweight material preferences, each driving growth in building and construction, automotive interiors, and commercial signage sectors.

2. Performance + Cost Efficiency Balance

Unlike heavier solid boards, expanded PVC sheets combine mechanical resilience with low density, enabling manufacturers and fabricators to cut costs without compromising structural performance. This strength-to-weight advantage also aligns with sustainability goals — lighter materials reduce product life-cycle emissions when transported, installed, or recycled.

Moreover, the expanded PVC segment benefits from broader market trends in the PVC family, where raw PVC resin markets are themselves forecast to grow significantly through the decade, driven by construction and infrastructure uses.

3. Rising Infrastructure and Urbanization in Emerging Regions

Asia-Pacific — led by China, Southeast Asia, and India — remains the fastest-growing regional market for PVC foam and sheet products due to rapid urban infrastructure expansion and manufacturing scale-ups. Emerging economies are investing in building upgrades, advertising & display networks, and automotive interiors — each application creating additional demand.

Industry Challenges & Root Pain Points

Despite favorable fundamentals, the Expanded PVC Sheet market does face structural challenges that influence pricing, adoption rates, and technology strategies:

1. Raw Material Price Volatility

PVC resin prices — the dominant raw material for expanded PVC sheets — can fluctuate based on global petrochemical supply dynamics, energy costs, and regulatory shifts in chlorine and ethylene feedstock markets. Such volatility impacts manufacturer margins and downstream pricing stability.

2. Environmental & Regulatory Pressures

PVC materials (including expanded forms) face increasing scrutiny over environmental and lifecycle impacts. While performance attributes remain strong, concerns persist regarding chlorine-based chemistries, end-of-life disposal, and recyclability — especially in markets with strict environmental regulations. This drives manufacturers to innovate more eco-friendly formulations and closed-loop recycling practices.

The global PVC market at large has seen increased adoption of sustainability initiatives and recycling systems — with producers exploring bio-based plasticizers and reduced additives to improve environmental profiles.

3. Competitive Fragmentation & Margin Pressure

With the top five players accounting for just over 12% of revenues, the market remains dispersed, with many regional and specialized manufacturers competing on price, customization, and niche end-use applications. This fragmentation supports diversity but can also compress margins and slow global scale advantages.

Innovation Vectors & Future Trends

1. Sustainable PVC & Green Chemistry

Manufacturers are increasingly investing in eco-friendly formulations and recycling technologies to address environmental concerns and meet regulatory expectations. Adoption of bio-based additives, recyclates, and closed-loop processes will be differentiators in customer procurement decisions.

2. Customization & Value-Added Services

As end-use industries demand tailored thicknesses, textures, and finishes, producers who offer just-in-time fabrication services, custom cut-to-size boards, and integrated printing solutions will capture higher value share.

3. Integration with Digital Manufacturing

Advanced fabrication technologies, including CNC machining, laser cutting, and digital printing, are increasingly used with expanded PVC sheets — enabling rapid prototyping and bespoke signage production that traditional materials cannot match.

Outlook: A Stable Growth Path with Strategic Transition Potential

The global Expanded PVC Sheet market’s projected steady growth (CAGR ~4.41%) reflects confidence in its performance advantages and industrial breadth. While raw material volatility, regulatory pressures, and fragmented competition temper profit outlooks, opportunities exist in sustainable product innovation, custom solutions, and regional manufacturing expansion.

As infrastructure and commercial signage capacities rise — especially in Asia-Pacific and emerging markets — expanded PVC sheets are well positioned to balance traditional material replacement opportunities with next-generation, eco-aligned product portfolios.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp