QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Medical FPC- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Medical FPC market, including market size, share, demand, industry development status, and forecasts for the next few years.

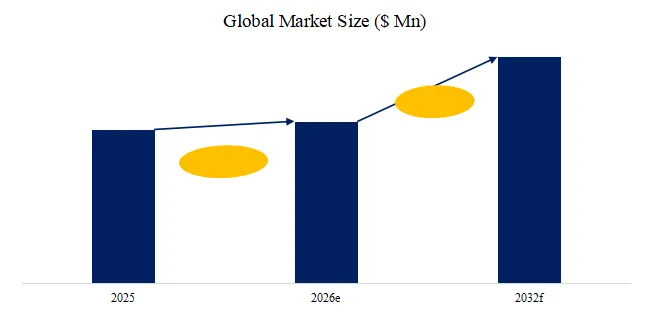

The global market for Medical FPC was estimated to be worth US$ 2303 million in 2025 and is projected to reach US$ 3350 million, growing at a CAGR of 5.5% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5999576/medical-fpc

Medical FPC Market Summary

Medical FPC is a flexible circuit board specially designed for medical scenes. With its unique flexibility, high reliability and biocompatibility, it has become a key component for miniaturization, intelligence and precision of modern medical equipment.

According to the new market research report “Global Medical FPC Market Report 2026-2032″, published by QYResearch, the global Medical FPC market size is projected to grow from USD 2303.14 million in 2025 to USD 3350 million by 2032, at a CAGR of 5.5% during the forecast period.

Table. Global Medical FPC Main Manufacturers

| Headquarter | Company | Business Introduction | |

| Japan | Mektec Corporation | Mektec Corporation is a global manufacturer of flexible printed circuit boards (FPCs). The company is dedicated to the research, development, production, and sales of FPCs, providing high-precision FPCs and related assembly and mechatronic modules to industries such as communications, consumer electronics, automotive, and medical worldwide. Mektec leverages its long-standing expertise in materials technology and processes to support the application of its products in miniaturization, lightweighting, and high-reliability scenarios. | |

| China Taiwan | Flexium | Flexium is a professional manufacturer of flexible printed circuit boards (FPCs) and one of the world’s leading manufacturers in the FPC field. The company primarily designs, develops, manufactures, and sells flexible printed circuit boards, including single-sided, double-sided, multilayer, and rigid-flex boards. It also provides module assembly and post-processing services, with products widely used in communications, computer, consumer electronics, industrial, automotive, and medical markets. | |

| Guangdong, China | Victory Giant Technology | Victory Giant Technology is a high-end printed circuit board (PCB) manufacturer. The company specializes in the R&D, production, and sales of high-density PCBs, covering a full range of PCB products including rigid circuit boards, flexible circuit boards, and rigid-flex boards. Its products are widely used in industries such as communications, computers and peripherals, consumer electronics, automotive electronics, industrial control, LED, and medical equipment. In recent years, Victory Giant has demonstrated outstanding performance in areas such as AI computing power and high-end servers and is gradually entering the global high-end PCB supply chain. | |

| Guangdong, China | Kinwong Electronic | Kinwong Electronic is a national high-tech enterprise specializing in the research, development, production, and sales of printed circuit boards (PCBs) and high-end electronic materials. The company’s products cover multilayer boards, thick copper boards, high-frequency and high-speed boards, metal-based PCBs, double-sided/multilayer flexible circuit boards, high-density flexible circuit boards, HDI boards, rigid-flex boards, special material PCBs, substrate-like boards, and packaging substrates, serving multiple downstream industries such as communications, automotive electronics, consumer electronics, industrial control, and medical equipment. With multiple production bases and offices both domestically and internationally, Kinwong Electronic is one of the world’s leading PCB suppliers. | |

| Korea | Interflex | Interflex Co., Ltd. is a manufacturer of flexible printed circuit boards. The company focuses on research, development, production, and sales of electronic interconnect products such as flexible circuits, rigid-flex hybrid circuits, and touch panels. Its products are widely used in smartphones, tablets, wearable devices, automotive electronics, displays, home appliances, and medical devices. | |

| Guangdong, China | Sun & Lynn | Sun & Lynn is a leading manufacturer of electronic interconnect products in China. The company primarily manufactures printed circuit boards (PCBs), high-density interconnects (HDI), metal substrates, thick copper boards, flexible printed circuit boards (FPCs), and rigid-flex boards, providing highly reliable products and one-stop services to industries such as communications, new energy, security, industrial control, automotive electronics, and medical equipment. Its products are sold to numerous markets worldwide. | |

| Singapore | Topsun | Topsun Electronic is a high-tech enterprise specializing in the design and manufacture of flexible printed circuit boards (FPCs). The company offers single-sided, double-sided, multilayer, and rigid-flex FPC products, widely used in mobile displays, smartphones/tablets, touch and camera modules, optical devices, and medical equipment. It is certified to ISO9001, ISO14001, ISO/TS16949, and ISO13485 quality management systems. | |

| Japan | Sumitomo Electric Printed Circuits | Sumitomo Electric Printed Circuits is a business entity specializing in the research and development and manufacturing of flexible printed circuit boards (FPCs), and is one of the world’s earliest entrants into the FPC field. The company has production bases in Japan and overseas, developing and mass-producing various types of FPC products, including ultra-fine lines, high-frequency/low-dielectric FPCs, automotive and high-reliability FPCs, applied in multiple high-value-added fields such as smart terminals, wearable devices, robotics, medical devices, and aerospace. Leveraging the strong material development and technological accumulation of the Sumitomo Electric Group, its FPC products combine material innovation and manufacturing technology advantages to serve customers in the global electronics industry. | |

| Austria | AT&S | AT&S Austria Technologie & Systemtechnik AG is an Austrian manufacturer of high-end electronic interconnect solutions and a leading global manufacturer of high-end printed circuit boards and integrated circuit substrates. The company’s products encompass advanced interconnect products such as multilayer boards, HDI, flexible and rigid-flex boards, and IC substrates, widely used in high-tech fields such as mobile devices, automotive electronics, industrial applications, aerospace, 5G communications, and medical applications. AT&S continues to drive the development of miniaturization and high-density interconnect technologies. | |

| Switzerland | DYCONEX | DYCONEX AG is a high-end printed circuit board manufacturer. The company focuses on the design and manufacture of high-density interconnects, flexible, rigid-flex hybrid, and high-frequency/high-reliability PCBs, particularly providing customized, miniaturized, and high-reliability interconnect solutions for demanding applications in medical devices, aerospace, industrial, and semiconductor sectors. Products comply with IPC Class III standards and possess significant advantages in miniaturization, precision wiring, and advanced materials technologies. | |

Above data is based on report from QYResearch: Global Medical FPC Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Supply Chain Analysis of Medical FPCs:

Upstream: The core is high-reliability materials: PI substrate (such as DuPont Kapton), electrolytic/rolled copper foil, halogen-free cover film, medical-grade adhesives and surface treatment chemicals. Strict requirements are placed on biocompatibility (ISO 10993), sterilability (EO/γ/high-temperature steam), and low leaching.

Midstream: FPC manufacturers with cleanroom capabilities, micro-wires (≤50μm), impedance control, and multi-layer rigid-soft bonding capabilities are required. They must pass ISO 13485 and customer audits, emphasizing batch traceability and consistency.

Downstream: Medical device OEMs and module manufacturers, used in endoscopes, wearable monitoring, ultrasound probes, minimally invasive surgical instruments, and implant/interventional device connections. The overall characteristics are small-batch, multi-variety production, deep R&D collaboration, and strong binding of validation and registration. The entry barrier lies in material validation and quality systems, while profit margins depend on technological complexity and long-term supporting relationships.

Key Drivers:

The main drivers for medical FPCs stem from technological innovation and market demand in the medical industry. Medical devices are increasingly miniaturized and lightweight, requiring compact and reliable designs for flexible circuits. The rapid popularization of smart healthcare and remote monitoring has driven demand for high-reliability, low-power FPCs to support real-time data acquisition and transmission. The aging population and chronic disease management trends have promoted the growth of wearable devices and implantable medical electronics, expanding the application scope of flexible circuits. Technological innovations such as the integration of IoT, AI, and flexible electronics have made medical devices more powerful and intelligent, driving the evolution of FPCs towards high performance. Advances in biocompatible materials and advanced manufacturing processes ensure the safety and durability of FPCs in the human body environment, meeting stringent medical certification standards. Simultaneously, increased global investment and policy support in the healthcare sector have accelerated the penetration of FPCs in diagnostic, therapeutic, and health monitoring devices. These factors collectively drive the continued expansion of the medical FPC market.

Key Obstacles:

The main obstacles to medical FPCs lie in their extremely high technical and market entry barriers. Medical applications place near-stringent demands on flexible circuits, requiring products to pass rigorous long-term biocompatibility and in vitro/in vivo stability tests. This results in lengthy and uncertain development cycles, with high certification costs and time investment being the primary hurdles. The manufacturing process is extremely complex, requiring reliable interconnection of multiple layers of high-precision circuitry within a very small space, and ensuring long-term performance stability under harsh environments such as bending and contact with bodily fluids. Any minute defect can lead to catastrophic consequences, thus placing high demands on the production environment and materials. The extreme requirements for purity and process control directly drive-up manufacturing costs. Compared to consumer electronics, the medical market typically has limited procurement volumes for individual products, but strong customization demands. This makes it difficult for companies to effectively reduce costs through large-scale production, squeezing profit margins under intense market competition. Furthermore, upstream high-end raw materials such as specialized polyimide films and specialty adhesives still rely to some extent on imports, posing potential risks to the self-control of the supply chain. The inherent conservatism of the medical industry also makes the verification and introduction of new suppliers very slow, resulting in extremely high customer loyalty. These factors collectively constitute significant challenges to the industry’s development.

Industry Development Opportunities:

The medical FPC industry is ushering in unprecedented development opportunities. The global wave of digital transformation and intelligent upgrading in the healthcare industry has provided a broad stage for flexible circuits. The continued popularization of wearable health monitoring devices, such as continuous glucose meters and smart ECG patches, directly drives the demand growth of high-precision and high-reliability medical FPCs. The promotion of telemedicine and home care models has made lightweight and flexible medical terminal devices a trend, further expanding market space. In the field of high-end medical equipment, the precision development of surgical robots, high-end endoscopes, and imaging equipment is inseparable from special FPC solutions that can achieve three-dimensional assembly and high-speed signal transmission, which constitutes an important value growth point. In terms of technological innovation, cutting-edge explorations such as biodegradable flexible electronics and epidermal electronics are opening up the imagination space for future implantable and transient electronic devices, bringing long-term growth potential to the industry. At the same time, the promotion of new medical infrastructure in China and the policy guidance of domestic substitution of high-end medical devices have created a window of opportunity for local supply chain companies to enter the mainstream market. The increasingly close collaborative innovation of upstream and downstream industries in materials, processes, and design is jointly driving the industry towards higher performance, higher integration, and higher reliability.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Medical FPC market is segmented as below:

By Company

Mektec Corporation

Flexium

Victory Giant Technology

Kinwong Electronic

Interflex

Sun & Lynn

Topsun

Sumitomo Electric Printed Circuits

AT&S

DYCONEX

Segment by Type

Single-layer FPC

Double-layer FPC

Multilayer FPC

Rigid-Flex PCB

Segment by Application

Medical Imaging Equipment

Endoscope

Wearable Medical Equipment

Implantable Medical Equipment

Others

Each chapter of the report provides detailed information for readers to further understand the Medical FPC market:

Chapter 1: Introduces the report scope of the Medical FPC report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Medical FPC manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Medical FPC market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Medical FPC in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Medical FPC in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Medical FPC competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Medical FPC comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Medical FPC market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Medical FPC Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Medical FPC Market Research Report 2026

Global Medical FPC Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp