QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Non-ferrous Metal Recycling Solutions- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Non-ferrous Metal Recycling Solutions market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for Non-ferrous Metal Recycling Solutions was estimated to be worth US$ million in 2024 and is forecast to a readjusted size of US$ million by 2031 with a CAGR of %during the forecast period 2025-2031.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/3643986/non-ferrous-metal-recycling-solutions

1. Non-ferrous Metal Recycling Solutions Market Summary

Non-ferrous metal recycling solutions refer to comprehensive technologies and services that minimize resource waste and reduce environmental pollution through the recycling, processing, and reuse of scrap non-ferrous metals. These solutions involve multiple stages, including the collection, sorting, smelting, refining, and reprocessing of scrap metals, aiming to transform waste metal materials into reusable raw materials, thereby achieving a circular economy and sustainable development. With increasingly scarce resources and stringent environmental policies, non-ferrous metal recycling has become a vital industry globally, playing a crucial role, particularly in sectors such as electronic waste, automotive, construction, and packaging.

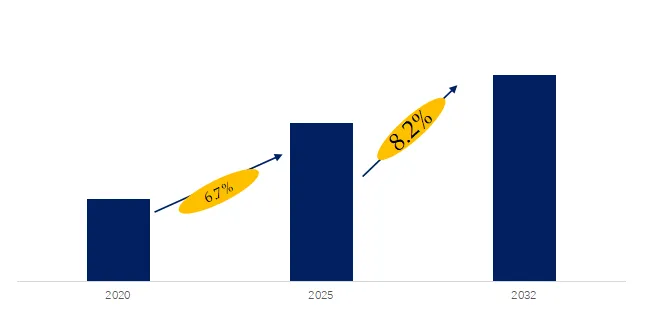

According to the latest research report from QYResearch, in terms of market size, the global Non-ferrous Metal Recycling Solutions market size is projected to grow from USD 50 billion in 2025 to USD 54 billion by 2032, at a CAGR of 8.2% during the forecast period.

Figure00001. Global Non-ferrous Metal Recycling Solutions Market Revenue Growth Rate, 2021-2032

Above data is based on report from QYResearch: Global Non-ferrous Metal Recycling Solutions Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

2 Introduction of Major Manufacturers of Non-ferrous Metal Recycling Solutions

| Serial Number |

Company |

| 1 |

SMS group GmbH |

| 2 |

Steinert |

| 3 |

Harmony Enterprises |

| 4 |

Recco Non Ferro Metals |

| 5 |

Rubicon |

| 6 |

Wanless Waste Management |

| 7 |

WARD |

| 8 |

Cohen |

| 9 |

Jansen Recycling Group |

| 10 |

JLM Metal Recycling & Auto Parts |

| 11 |

Moffatt Scrap Iron & Metal |

| 12 |

GLR Advanced Recycling |

| 13 |

Ferrous Processing & Trading |

| 14 |

Fortum |

Source: Third-party data, QYResearch Research Team

According to a survey by QYResearch’s Leading Enterprise Research Center, global Non-ferrous Metal Recycling Solutions manufacturers include SMS group GmbH, Steinert, Harmony Enterprises, Recco Non Ferro Metals, Rubicon, etc. By 2025, the top five global manufacturers will hold approximately 26% of the market share.

Introduction to Key Companies

Company 1

| SMS group GmbH |

Description |

| Company Introduction |

SMS group GmbH is a leading global industrial engineering company specializing in metal processing equipment and technology solutions, with particularly strong capabilities in the steel and non-ferrous metals industries. Through innovative technologies and equipment, the company provides efficient production and processing systems to global clients, helping them optimize production processes and improve product quality. SMS group’s solutions cover multiple areas from metallurgy to automation, committed to driving sustainable development and green production. The company boasts a strong global service network, ensuring client success in various markets. |

| Product Introduction |

SMS group GmbH offers advanced non-ferrous metal recycling solutions, dedicated to improving recycling efficiency and quality. Its technologies include efficient smelting, sorting, and refining processes that maximize recovery rates and reduce environmental impact. The company employs innovative equipment and intelligent technologies to ensure the efficient extraction and reuse of non-ferrous metals. SMS group’s recycling systems are suitable for various non-ferrous metals, including aluminum and copper, helping companies achieve resource recycling, reduce production costs, and comply with increasingly stringent environmental standards. |

Source: Third-party data, QYResearch Research Team

Company 2

| Steinert |

Description |

| Company Introduction |

Steinert is a leading global company specializing in material sorting and recycling technologies, providing innovative solutions for non-ferrous metal recycling, waste treatment, and mineral sorting. The company utilizes advanced magnetic separation, X-ray sorting, and spectroscopy technologies to provide efficient and precise sorting and recycling equipment for clients across various industries. Steinert’s products are widely used in the mining, recycling, and waste management sectors, helping clients improve resource utilization and optimize production processes. The company is committed to promoting sustainable development and developing environmentally friendly and energy-saving technological solutions. |

| Product Introduction |

Steiner’s non-ferrous metal recycling solutions utilize advanced material sorting technologies to help clients efficiently recycle non-ferrous metals. Through technologies such as magnetic separation, X-ray sorting, and laser sorting, Steinert’s equipment can accurately extract precious metals such as copper, aluminum, and nickel from waste. These solutions not only improve recycling efficiency but also ensure the extraction of high-quality metals, meeting stringent environmental requirements. Steinert’s systems help clients reduce waste disposal costs and achieve resource recycling, thereby promoting a green economy and sustainable development. |

Source: Third-party data, QYResearch Research Team

Company 3

| Harmony Enterprises |

Description |

| Company Introduction |

Harmony Enterprises is a company specializing in providing waste treatment and recycling equipment, committed to innovation and sustainable development. The company provides clients with a diverse range of waste compression and recycling solutions, with particular expertise in non-ferrous metal recycling and waste management. Harmony Enterprises helps businesses achieve efficient waste recycling, reduce operating costs, and improve resource utilization through its advanced technologies. The company serves a wide range of industries, including waste treatment, recycling, waste management, and environmental protection, driving global circular economy and environmental protection goals. |

| Product Introduction |

Harmony Enterprises’ non-ferrous metal recycling solutions offer efficient waste compression and sorting technologies to help businesses recover precious metals such as aluminum, copper, and steel. Through its innovative waste compression and recycling equipment, Harmony helps customers reduce waste volume and increase metal recovery rates. Its product designs prioritize energy efficiency and environmental protection, ensuring minimal environmental impact during processing. Through intelligent and automated technologies, Harmony Enterprises’ solutions make non-ferrous metal recycling more efficient, economical, and environmentally compliant, helping businesses achieve their sustainability goals. |

Source: Third-party data, QYResearch Research Team

3 Non-ferrous Metal Recycling Solutions Industry Chain Analysis

| Industry Chain |

Description |

| Upstream |

The upstream of the non-ferrous metal recycling industry chain mainly includes a scrap metal recycling network, dismantling and sorting enterprises, and the collection of social and industrial waste. The recycling network encompasses scrap recycling stations, auto dismantling plants, electronic waste processing companies, and building demolition companies, responsible for collecting waste containing non-ferrous metals such as copper, aluminum, lead, and zinc from scrapped vehicles, waste electronic products, construction waste, and industrial scrap. The upstream segment also involves preliminary manual or mechanical dismantling, sorting, and packaging to remove impurities such as plastics and rubber, providing raw materials for downstream processing. The coverage density, sorting accuracy, and logistics efficiency of the recycling network directly determine the raw material supply capacity of the entire industry chain and are the starting point for industry operation. |

| Midstream |

The midstream of the industry chain is the core processing stage of metal recycling, including intelligent sorting, pyrometallurgical or hydrometallurgical processes, refining and purification, and the production of recycled materials. Modern sorting plants employ advanced technologies such as AI visual recognition, X-ray fluorescence spectroscopy, and eddy current separation to accurately separate mixed waste into different categories of pure metal components. Smelting enterprises transform waste metals into standard products such as recycled copper, recycled aluminum, and recycled lead through processes like smelting and electrolysis. Some high-end production lines can also produce high-quality materials such as aerospace-grade recycled aluminum alloys and electronic-grade recycled copper. The technological level of the midstream segment determines the metal recovery rate, product purity, and energy consumption and environmental protection indicators, making it the core of value creation in the industrial chain. |

| Downstream |

The downstream of the industrial chain covers various application scenarios for recycled metals and a service system derived from the circular economy. Major users include processing companies in industries such as automobile manufacturing, building materials, electronics, and packaging materials, which use recycled copper and aluminum to produce end products such as parts, profiles, and cables. Driven by dual carbon targets, more and more brands are committing to using green recycled materials, and the downstream market is shifting from price-oriented to low-carbon value-oriented. Furthermore, the downstream has extended to professional services such as recycled metal carbon footprint certification, green supply chain consulting, international waste trade, and futures hedging, forming a complete circular economy industrial ecosystem. |

Source: Third-party data, QYResearch Research Team

4 Non-ferrous Metal Recycling Solutions Industry Development Trends, Opportunities, Obstacles and Industry Barriers

Development Trends:

1. The market continues to expand, with a trillion-dollar sector rapidly taking shape. The global metal recycling market is experiencing steady growth. This expansion is mainly due to increasing awareness of the depletion of metal reserves and the continued rise in demand for recycled metals from end-use industries such as automotive, construction, and electronics. Recycling, as a process of dual importance to industry and the environment, is evolving from a peripheral supplement to a mainstream supply model.

2. Green transformation has become a global consensus, with significant regional differences in development paths. Against the backdrop of global carbon reduction, recycled metals have become a key resource for the steel and non-ferrous metals industries. By 2025, 63 countries worldwide had incorporated recycled metal utilization into their carbon neutrality assessment systems. However, there are significant differences between developing and developed countries in terms of resource endowment, policy systems, and technological capabilities. Resource-sufficient countries are actively investing in new technologies, while resource-importing countries face import dependence and the risk of overcapacity. Regional differentiation is reshaping the global industrial landscape.

3. Technological innovation and digitalization are empowering industries to improve quality and efficiency. Intelligent inspection, standardized quality control, and low-carbon process innovation have become common choices for the industry to address challenges. The integration of technologies such as artificial intelligence, machine learning, the Internet of Things, and blockchain is optimizing recycling processes, improving compliance, enhancing inventory management, and increasing decision-making accuracy. Digital tools are driving supply chain transparency, providing strong support for carbon footprint traceability and green certification, and the industry is undergoing a comprehensive upgrade from traditional manual sorting to intelligent precision recycling.

Development Opportunities:

1. Dual-carbon goals drive essential demand for green metals. Driven by the deepening implementation of dual-carbon goals and the rapid development of the new energy industry, the resource security value and low-carbon emission reduction attributes of recycled metals are becoming increasingly prominent. The implementation of EU carbon tariffs and carbon neutrality policies in various countries makes green recycled metals a significant advantage in export trade. Recycling can significantly reduce energy consumption, greenhouse gas emissions, and minimize the extraction of new resources, making it a more sustainable option.

2. Emerging fields expand high-value applications. The application scenarios for recycled metals in emerging fields such as the “new three pillars” (new energy equipment, lithium batteries, and wind power equipment), the low-altitude economy, and robotics are constantly expanding. Strong demand for recycled metals from industries such as automotive, construction, electronics, and packaging confirms their cost-effectiveness and superior performance. Advances in recycling technology have improved the purity of these materials, enabling recycled metals to directly enter high-end manufacturing fields such as aerospace and precision electronics, driving the industry’s transformation from simple “quantity increase” to high-quality “quality improvement.”

3. Asia Pacific becomes the fastest-growing emerging market. Due to accelerating economic growth, the Asia Pacific region is expected to become the world’s largest and fastest-growing metal recycling market. The increasing demand for metals from emerging countries such as India and China is strongly boosting market development in the region. Southeast Asia and South Asia, leveraging their geographical advantages, have become emerging global raw material distribution markets. India imports an average of 1.8 million tons of recycled aluminum raw materials annually, while Thailand’s scrap aluminum exports have surged by 76% year-on-year.

Hindering Factors:

1. International trade barriers are reshaping the global trade landscape. The global recycled metals market is experiencing unprecedented regulatory volatility in 2026. The US has implemented a 10% comprehensive import tariff, the EU is considering restricting scrap exports, and Malaysia has imposed an absolute ban on e-waste imports. These policies are reshaping traditional scrap trade flows, leading to increased compliance costs, blocked arbitrage opportunities, and a highly uncertain international trade environment for market participants. Traditional aluminum scrap trade flows are being completely reshaped.

2. Fluctuations in primary metal prices impact recycling economics. One of the main limiting factors affecting the global recycled metals market is the volatility of raw material metal prices, which leads to fluctuations in recycling operations. When primary metal market prices fall, the economic incentive for recycling decreases, forcing recyclers to reduce processing volumes or lower profit margins. The complex sorting and processing of mixed metals further increases operational difficulty and costs, and regulatory barriers and insufficient recycling infrastructure in some regions exacerbate these challenges.

3. Alloy melting leads to technical bottlenecks in downgraded recycling. While chemically stable metals such as copper can be recycled without loss of quality, steel and aluminum are often alloyed with elements that are difficult to separate, leading to downgraded recycling and quality degradation. Aluminum recycling faces alloy-related limitations, requiring precise separation by alloy type to maintain material quality. Without fine sorting, recycled output is often downgraded, limiting its usability and market value. These thermodynamic and technological constraints are compounded by other structural limitations.

Barriers:

1. Capital Scale and Global Network Deployment Barriers: Advanced sorting and traceability systems require upfront investment, but in the absence of a clear business model, stable demand, or effective incentives, these investments struggle to yield reasonable returns. In uncertain markets, companies are reluctant to shift resources away from established production methods. International giants are accelerating mergers and acquisitions to compete for high-quality raw material resources, leading to a restructuring of the global recycled metal raw material trade landscape. The density of the recycling network directly impacts raw material acquisition capabilities, creating natural capital and scale barriers.

2. Technological R&D and Sorting Capability Barriers: The application level of technologies such as intelligent sorting and low-energy smelting directly determines metal recovery rates and product quality stability. Even if secondary processes are technically feasible, demand structures often still reinforce the use of virgin materials. The application of recycled materials is limited by insufficient buyer interest, high dismantling costs, and unstable supply quality. Virgin materials are typically cheaper, of guaranteed quality, and supported by long-term procurement practices, limiting the market coverage of recycled alternatives.

3. Environmental Compliance and Policy Regulatory Barriers: Governments worldwide have implemented strict regulations to curb illegal mining and the exploitation of metal reserves. While these measures have positively impacted industry growth, they have also significantly raised compliance thresholds. The EU’s Basel Convention amendments have imposed strict controls on the trade of electronic waste resources, and Malaysia has extremely stringent requirements for the SIRIM purity of imported waste. High compliance costs exclude non-compliant companies, and only those with robust environmental systems and compliance capabilities can establish themselves in the international market.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Non-ferrous Metal Recycling Solutions market is segmented as below:

By Company

SMS group GmbH

Steinert

Harmony Enterprises

Recco Non Ferro Metals

Rubicon

Wanless Waste Management

WARD

Cohen

Jansen Recycling Group

JLM Metal Recycling & Auto Parts

Moffatt Scrap Iron & Metal

GLR Advanced Recycling

Ferrous Processing & Trading

Fortum

BIG – Brannon Industrial Group

Segment by Type

Electrolytic Deposition

Precipitation

Non-ferrous Metal Sensor

Segment by Application

Steel

Iron

Aluminum

Alloy

Others

Each chapter of the report provides detailed information for readers to further understand the Non-ferrous Metal Recycling Solutions market:

Chapter 1: Introduces the report scope of the Non-ferrous Metal Recycling Solutions report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Non-ferrous Metal Recycling Solutions manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Non-ferrous Metal Recycling Solutions market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Non-ferrous Metal Recycling Solutions in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Non-ferrous Metal Recycling Solutions in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Non-ferrous Metal Recycling Solutions competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Non-ferrous Metal Recycling Solutions comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Non-ferrous Metal Recycling Solutions market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Non-ferrous Metal Recycling Solutions Sales Market Report, Competitive Analysis and Regional Opportunities 2025-2031

Global Non-ferrous Metal Recycling Solutions Market Outlook, In‑Depth Analysis & Forecast to 2031

Global Non-ferrous Metal Recycling Solutions Market Research Report 2025

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp