QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Electric Vehicle Battery Swapping Services- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Electric Vehicle Battery Swapping Services market, including market size, share, demand, industry development status, and forecasts for the next few years.

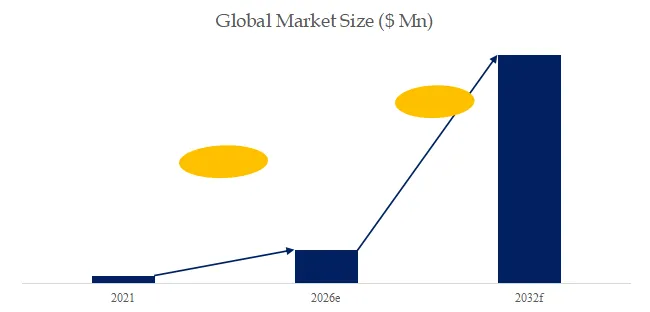

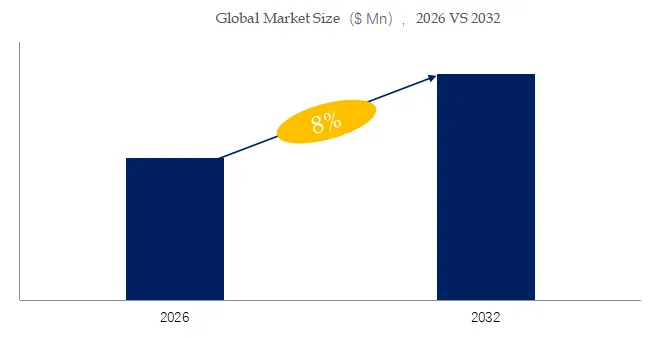

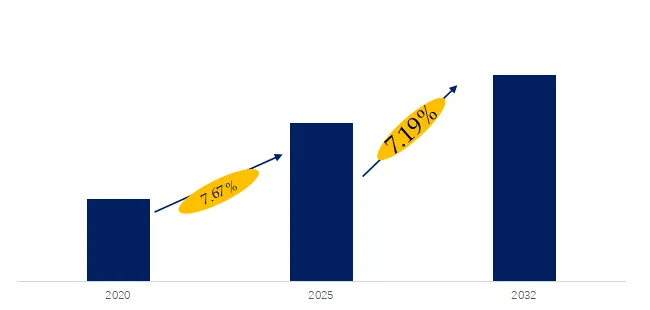

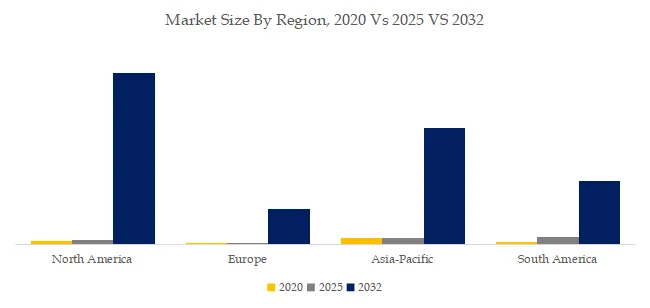

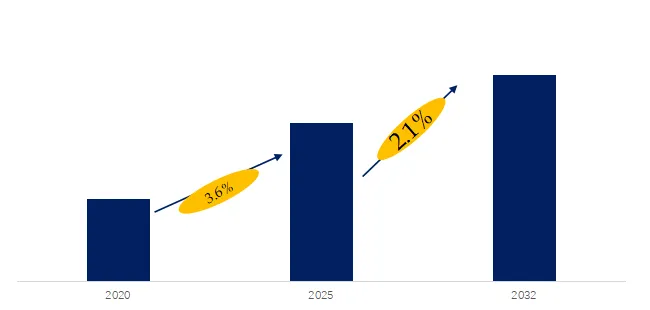

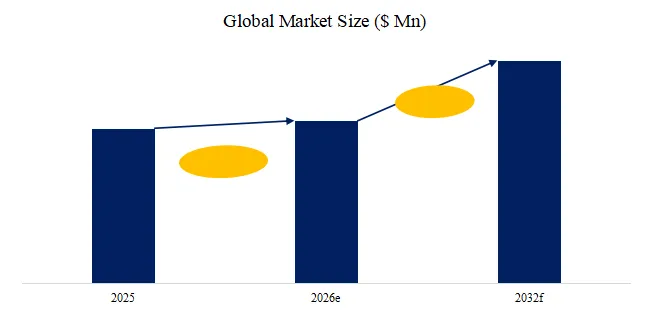

The global market for Electric Vehicle Battery Swapping Services was estimated to be worth US$ 3974 million in 2025 and is projected to reach US$ 12028 million, growing at a CAGR of 17.0% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6035741/electric-vehicle-battery-swapping-services

Figure00001. 1. Electric Vehicle Battery Swapping Service Market Summary

Electric vehicle battery swapping service refers to the rapid replacement of electric vehicle batteries through dedicated battery swapping stations, rather than traditional charging. This service is typically offered at swapping stations, where vehicle owners exchange their electric vehicle’s battery for a fully charged one. The entire process is quick and convenient, avoiding long charging waits. Battery swapping services are widely used in shared electric vehicles, taxis, and electric logistics vehicles. By swapping batteries, owners can significantly improve the efficiency of their electric vehicles and reduce time lost due to battery charging. Compared to charging, battery swapping offers higher energy efficiency and faster response times, becoming an important supplement and optimization solution for the electric vehicle industry.

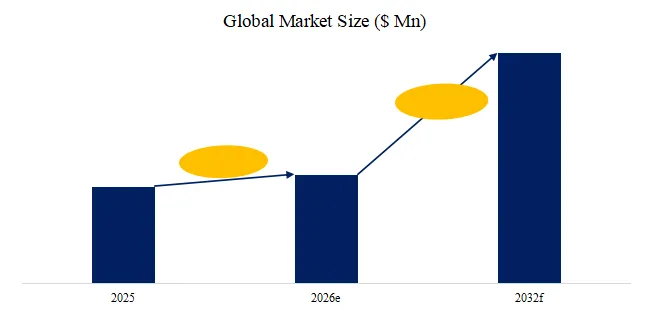

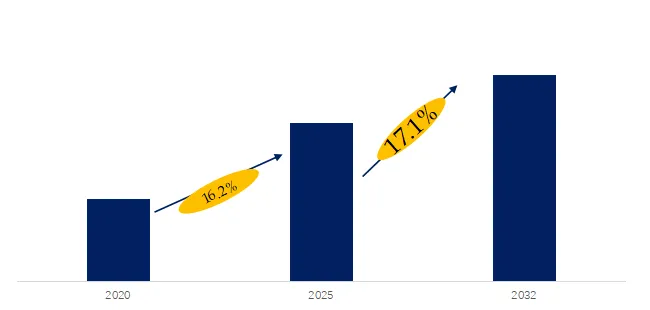

According to the latest research report from QYResearch, in terms of market size, the global Electric Vehicle Battery Swapping Service market size is projected to grow from USD 4.0 billion in 2025 to USD 4.7 billion by 2032, at a CAGR of 17% during the forecast period.

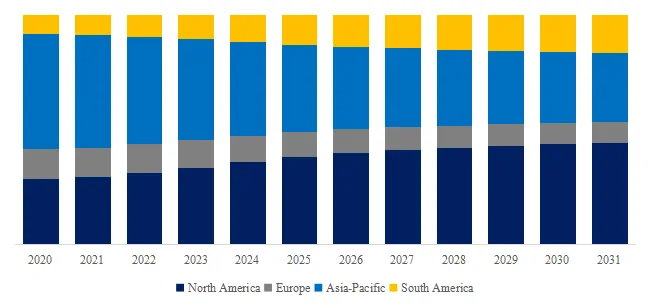

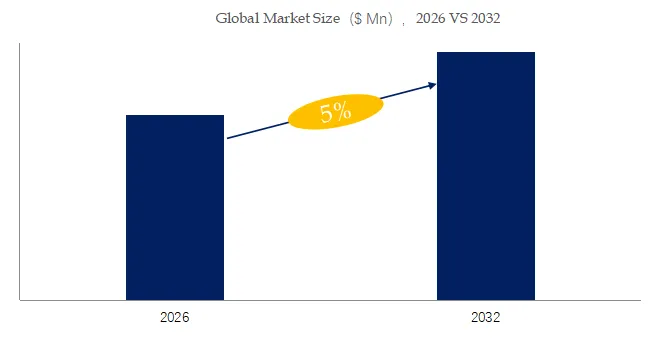

Figure00002. Global Electric Vehicle Battery Swapping Service Market Revenue Growth Rate, 2021-2032

Above data is based on report from QYResearch: Global Electric Vehicle Battery Swapping Service Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

2 Introduction of Major Manufacturers of Electric Vehicle Battery Swapping Service

| Serial Number | Company |

| 1 | Swobbee |

| 2 | Battery Smart |

| 3 | Gogoro |

| 4 | Oyika |

| 5 | IONEX |

| 6 | China Tower Co.,Ltd. |

| 7 | Yugu Technology |

| 8 | Shenzhen Immotor Technology Co., Ltd. |

| 9 | Huan Huan |

| 10 | Mandian-future |

| 11 | Duduhuandian |

| 12 | Shanghai 982 IoT Technology Co., Ltd. |

| 13 | Swap Energi Indonesia |

| 14 | Gachaco |

| 15 | ARUN PLUS(Swap & Go) |

| 16 | Blueshark |

| 17 | Bangchak (Winnonie) |

| 18 | Hello-inc |

| 19 | Cosbike |

| 20 | Guodong Power |

| 21 | Hthuandian |

| 22 | Zhizutech(Zhizukj) |

| 23 | Spiro |

Source: Third-party data, QYResearch Research Team

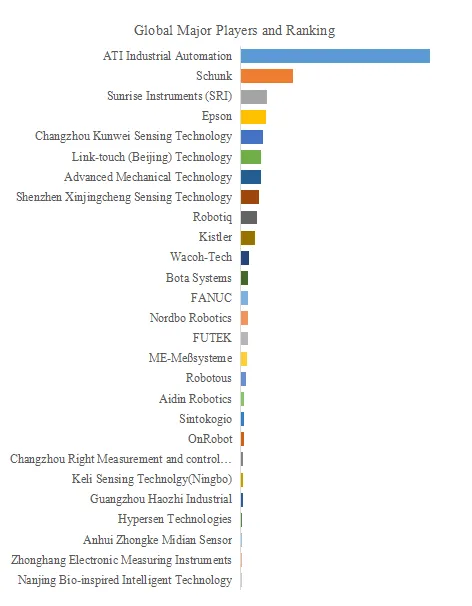

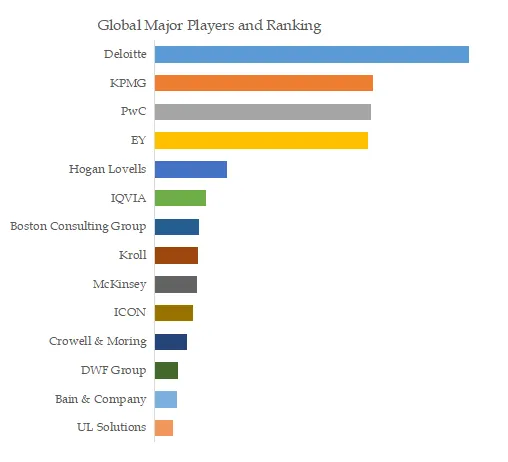

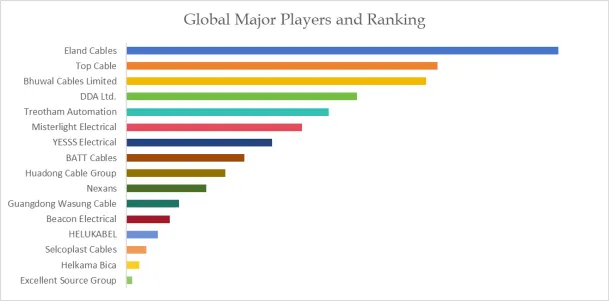

According to a survey by QYResearch’s Leading Enterprise Research Center, global Electric Vehicle Battery Swapping Service manufacturers include Swobbee, Battery Smart, Gogoro, Oyika, IONEX, etc. By 2025, the top five global manufacturers will hold approximately 25% of the market share.

Introduction to Key Companies

Company 1

| Swobbee | Description |

| Company Introduction | Swobbee is an innovative technology company specializing in battery swapping services for electric vehicles, particularly in the two-wheeled electric vehicle sector. Swobbee is committed to providing an efficient and convenient battery swapping network to address the battery range issues faced by electric vehicle users during long-distance travel. Through its smart swapping stations, Swobbee provides convenient battery swapping services for electric bicycle and electric motorcycle users in urban and rural areas, eliminating waiting times for charging and improving travel efficiency. Swobbee’s solutions not only promote green travel but also foster sustainable urban transportation. |

| Product Introduction | Swobbee’s electric vehicle battery swapping service offers users of two-wheeled electric vehicles an innovative and fast battery swapping experience. Users can quickly swap batteries at Swobbee’s swapping stations, eliminating waiting times at traditional charging stations. The service covers a wide range of urban areas and supports various types of electric bicycles and electric motorcycles. Swobbee also monitors battery health in real time through an intelligent system to ensure an efficient and safe swapping process. This service not only improves the convenience of electric vehicle users’ travel but also promotes the development of green and environmentally friendly transportation, contributing to low-carbon travel. |

Source: Third-party data, QYResearch Research Team

Company 2

| Battery Smart | Description |

| Company Introduction | Battery Smart is a company focused on providing battery swapping services for electric vehicles, committed to promoting sustainable electric mobility through intelligent battery management and a shared battery swapping platform. Through its innovative network of swapping stations, the company enables electric motorcycle and electric bicycle users to conveniently swap batteries anytime, anywhere, avoiding the limitations of traditional charging infrastructure. Battery Smart’s services not only address range anxiety but also increase the adoption rate of electric vehicles, contributing to the achievement of green transportation and energy conservation goals. |

| Product Introduction | Battery Smart’s electric vehicle battery swapping service provides a convenient battery replacement solution for two-wheeled electric vehicles, aiming to optimize the electric vehicle user experience. Users simply go to a Battery Smart swapping station and quickly exchange their fully charged batteries using smart devices, avoiding waiting time for charging. This service network covers multiple cities and supports various brands and models of electric motorcycles and electric bicycles. By monitoring battery health in real time, Battery Smart ensures the efficiency and safety of its service, making electric mobility more convenient and environmentally friendly. |

Source: Third-party data, QYResearch Research Team

Company 3

| Gogoro | Description |

| Company Introduction | Gogoro is a leading global smart electric mobility solutions company, focusing on developing electric motorcycles, battery swapping technology, and related services. Through its innovative battery swapping platform, Gogoro provides users with a fast electric vehicle battery swapping service, eliminating charging station wait times and making electric mobility more efficient and environmentally friendly. The company is committed to promoting sustainable urban development and reducing carbon emissions. Gogoro’s products and services not only change personal mobility but also promote green transportation and smart city development, gaining recognition in multiple markets worldwide. |

| Product Introduction | Gogoro’s electric vehicle battery swapping service is one of its innovative core products, designed specifically for two-wheeled electric vehicle users, solving the time-sensitive problem of traditional charging infrastructure. Gogoro’s battery swapping station network widely covers multiple cities, allowing users to quickly swap batteries in minutes using its intelligent system. Gogoro’s batteries are not only highly efficient and long-lasting but also monitor battery health in real time through an intelligent management system. This service eliminates range anxiety for electric motorcycle and electric bicycle users, improving the convenience and reliability of travel and promoting the adoption of green mobility. |

Source: Third-party data, QYResearch Research Team

3 Electric Vehicle Battery Swapping Service Industry Chain Analysis

| Industry Chain | Description |

| Upstream | The upstream of the battery swapping service industry chain for two-wheeled electric vehicles mainly includes the R&D and production of lightweight power batteries, the manufacturing of battery swapping cabinets and smart hardware, and the development of battery management systems and IoT communication modules. Battery manufacturers focus on producing standardized, swappable lithium battery packs, emphasizing lightweight design, high cycle life, and safety performance to adapt to high-intensity usage scenarios such as those of food delivery riders. Battery swapping equipment suppliers provide modular smart battery swapping cabinets, integrating charging compartments, mechanical locking mechanisms, temperature-sensing fire suppression systems, and user interfaces. IoT companies provide 4G/5G communication modules, smart control boards, and cloud platform access services, enabling real-time battery status uploading, remote monitoring of battery swapping cabinets, and user identification. The technological maturity of the upstream segment directly determines the operational efficiency and asset security of the battery swapping service. |

| Midstream | The midstream of the industry chain is the core operational link of the two-wheeled battery swapping service, encompassing the investment and layout of the battery swapping network, urban site operation and maintenance, full lifecycle management of batteries, and user subscription services. Battery swapping operators densely deploy battery swapping cabinets in core business districts, food delivery hubs, and around communities, building a “3-kilometer battery swapping circle,” and ensuring a balanced battery inventory at each network point through self-developed scheduling algorithms. Battery asset management companies hold battery assets using a “lease-to-own” model, offering monthly rental packages to riders while also handling daily battery maintenance, health monitoring, and the reuse of decommissioned batteries. Midstream operators also need to establish strategic partnerships with food delivery platforms and logistics companies, embedding battery swapping services into rider workflows to reduce the cost per swap through economies of scale and using battery data to inform upstream product iterations. |

| Downstream | The downstream industry chain covers professional users, primarily on-demand delivery riders, as well as the emerging individual commuters. Riders in food delivery, express delivery, and fresh food delivery industries are extremely sensitive to energy replenishment efficiency, swapping batteries 2-3 times daily, making them the primary group with a strong need for battery swapping services and the main consumers. As battery swapping network density increases and user habits develop, residents in surrounding communities and shared electric bicycle operators are also beginning to integrate into the battery swapping system. Downstream services have also spawned diversified value-added businesses such as battery leasing installment plans, vehicle + battery packages, rider accident insurance, battery swapping station advertising space, and battery data services. Leveraging their high-density community locations, battery swapping stations are gradually being upgraded into smart terminals at the city’s edge, integrating energy replenishment, retail, and convenient services. |

Source: Third-party data, QYResearch Research Team

4 Electric Vehicle Battery Swapping Service Industry Development Trends, Opportunities, Obstacles and Industry Barriers

Development Trends:

1. Southeast Asia becomes a core engine of global growth. Southeast Asian countries, represented by Indonesia, Vietnam, and Thailand, are becoming hotspots for battery swapping services globally, driven by their large electric two-wheeler fleets and government policies banning motorcycles. Indonesia has attracted local battery swapping startups like Gorila and Swap to accelerate their deployments, and the density of battery swapping networks in core cities like Jakarta continues to increase. Motorcycles are the primary mode of transportation in ASEAN countries, and battery swapping is rapidly evolving from a peripheral supplement to a mainstream energy replenishment method.

2. Battery standardization moves from corporate alliances to regional consensus. To overcome compatibility bottlenecks in battery swapping promotion, Southeast Asian countries are promoting regional battery exchange standards. The ASEAN Battery Swapping Alliance, initiated by Indonesia, unites local and international automakers and battery manufacturers to jointly develop unified battery pack specifications and interface protocols. This development path, prioritizing regional standards, is replicating the successful experience of two-wheeled battery swapping in China, clearing technical obstacles for large-scale deployment.

3. Operating models are undergoing a deep transformation towards “Battery as a Service.” The BaaS (Battery as a Service) model is rapidly gaining popularity in the global two-wheeled battery swapping market. Users don’t need to purchase batteries; they can enjoy unlimited battery swaps by paying a monthly subscription fee. This model significantly reduces the cost of purchasing a vehicle for users, while entrusting battery assets to professional operators for centralized management, maintenance, and tiered utilization. Local startups like Gorila have established dense battery swapping networks in several core urban areas of Indonesia using the BaaS model, with the daily number of swaps continuously increasing.

Development Opportunities:

1. The essential market for users without charging stations. In China, approximately 50%-60% of households cannot install private charging stations due to a lack of fixed parking spaces or property restrictions. As the penetration rate of new energy vehicles continues to increase, the energy replenishment problem for this large group is becoming increasingly prominent. For them, relying on public charging stations involves uncertainties such as queuing and poor compatibility. Battery swapping, offering “certain energy replenishment,” has become a highly attractive solution.

2. Vehicle-battery separation lowers the barrier to entry. The Battery as a Service (BaaS) model allows users to purchase a vehicle without buying a battery, only paying a monthly subscription fee, significantly reducing the initial purchase cost of new energy vehicles. Over 80% of NIO’s new users choose the BaaS + battery swapping model. Simultaneously, the battery is centrally managed by the operator, facilitating maintenance and upgrades. In the future, once solid-state batteries or sodium-ion batteries are commercialized, existing users can directly replace them with new batteries.

3. The optimal path for commercial vehicle electrification. For high-frequency usage scenarios such as taxis, ride-hailing vehicles, and logistics vehicles, the efficiency advantage of the battery swapping model is extremely significant. Commercial vehicles with tight operating schedules cannot withstand long charging times, while a 3-5 minute battery swap can ensure near-uninterrupted operation, significantly improving uptime and return on investment. Heavy-duty truck battery swapping networks have already begun trunk line construction in Jiangxi and other regions.

Hindering Factors:

1. Cross-brand battery compatibility remains a challenge. Currently, battery pack sizes, interface standards, and communication protocols among different brands of electric two-wheelers are incompatible, creating significant ecosystem barriers. Battery swapping operators must stock multiple types of batteries, significantly increasing inventory pressure and operational complexity. Even within the same regional market, Honda, Yamaha, and local brands use different battery specifications, preventing users from swapping batteries across brands and operators, thus limiting network effects.

2. Cultivating user battery swapping habits is costly. Southeast Asian users are accustomed to free charging at home or on the street and have limited acceptance of monthly subscription-based battery swapping models. Cultivating users’ willingness to pay requires substantial market education investment, while simultaneously ensuring that the battery swapping network density reaches a critical point of “anytime, anywhere swapping,” otherwise users will find it difficult to develop a dependency. This “chicken and egg” dilemma presents new entrants with significant initial customer acquisition challenges.

3. Battery asset theft and security operation risks. In some emerging markets, battery assets in battery swapping stations face security risks such as theft and damage. Long-term use of batteries in high-temperature and high-humidity environments also poses a risk of thermal runaway, placing higher demands on operators’ asset protection capabilities and security monitoring systems.

Barriers:

1. High Capital Investment Barrier: While the construction cost of a single battery swapping station is lower than that of a car battery swapping station, covering core urban areas requires hundreds of locations and thousands of batteries, with initial investments often reaching tens of millions of US dollars. Local startups like Gorila have relied on multiple rounds of financing to support their expansion, but new entrants without substantial capital support will find it difficult to build an effective network density in the short term, creating a natural financial barrier.

2. Barriers Related to Localized Operations and Government Relationships: Battery swapping businesses are highly dependent on local infrastructure resources, requiring partnerships with power companies, shopping malls, convenience stores, gas stations, and other property owners to acquire prime locations. Simultaneously, various countries have strict regulatory requirements for battery imports, waste battery recycling, and telecommunications equipment (IoT modules), making it difficult for companies without local government relations and compliance capabilities to operate. Early entrants have secured core resources through government-enterprise cooperation.

3. Technological Barriers Related to Battery Management and Second-hand Utilization. Battery lifecycle management involves core technologies such as charging and discharging strategy optimization, real-time health monitoring, and screening and repurposing of retired batteries, directly impacting asset returns. Battery swapping operators need capabilities in battery pack design, BMS development, and tiered utilization; otherwise, they face risks of shortened battery life and increased safety hazards. This technological accumulation requires long-term R&D investment and scenario-based data validation, making it difficult for new entrants to replicate in the short term.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Electric Vehicle Battery Swapping Services market is segmented as below:

By Company

Swobbee

Battery Smart

Gogoro

Oyika

IONEX

China Tower Co.,Ltd.

Yugu Technology

Shenzhen Immotor Technology Co., Ltd.

Huan Huan

Mandian-future

Duduhuandian

Shanghai 982 IoT Technology Co., Ltd.

Swap Energi Indonesia

Gachaco

ARUN PLUS(Swap & Go)

Blueshark

Bangchak (Winnonie)

Hello-inc

Cosbike

Guodong Power

Hthuandian

Zhizutech(Zhizukj)

Spiro

Segment by Type

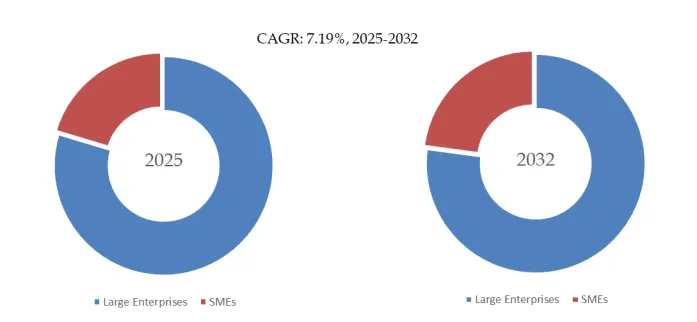

Traditional Automaker Operation Model

Third-Party Independent Operator Model

Government Cooperation Model

Segment by Application

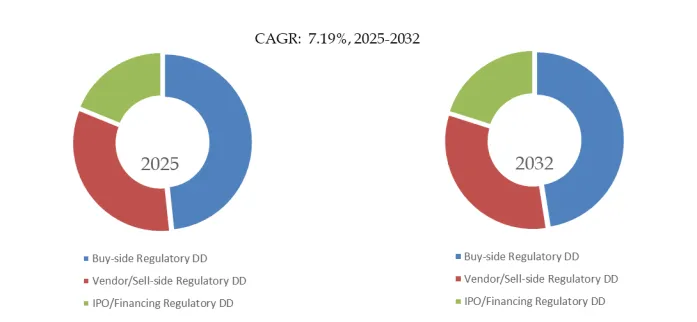

Commercial Vehicle

Passenger Vehicle

Each chapter of the report provides detailed information for readers to further understand the Electric Vehicle Battery Swapping Services market:

Chapter 1: Introduces the report scope of the Electric Vehicle Battery Swapping Services report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Electric Vehicle Battery Swapping Services manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Electric Vehicle Battery Swapping Services market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Electric Vehicle Battery Swapping Services in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Electric Vehicle Battery Swapping Services in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Electric Vehicle Battery Swapping Services competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Electric Vehicle Battery Swapping Services comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Electric Vehicle Battery Swapping Services market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Electric Vehicle Battery Swapping Service – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Electric Vehicle Battery Swapping Service Market Research Report 2026

Global Electric Vehicle Battery Swapping Services Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Electric Vehicle Battery Swapping Services Market Research Report 2026

Global Electric Vehicle Battery Swapping Services Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Two-Wheeled Electric Vehicle Battery Swapping Service Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Two-Wheeled Electric Vehicle Battery Swapping Service Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Two-Wheeled Electric Vehicle Battery Swapping Service – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Two-Wheeled Electric Vehicle Battery Swapping Service Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp