Introduction: Solving Range and Safety Challenges for Hydrogen Fuel Cell Vehicles

Hydrogen fuel cell electric vehicles (FCEVs) offer zero-emission driving with refueling times comparable to gasoline (3–5 minutes) and driving ranges exceeding 300–400 miles. However, storing hydrogen onboard presents significant engineering challenges: hydrogen has extremely low volumetric energy density (one-third that of natural gas at same pressure), requires high-pressure containment (350–700 bar / 5,000–10,000 psi), and demands absolute leak-tightness and impact resistance. Vehicle-mounted hydrogen storage systems (hydrogen storage tanks or bottles) solve these challenges using advanced Type IV composite cylinders (carbon fiber wrapped polymer liner) that are lightweight, high-strength, and certified to international safety standards (ISO 19881, EC79, GTR13). This article presents vehicle-mounted hydrogen storage system market research, offering insights into storage types, material technologies, and applications for automotive engineers and infrastructure investors.

Global Market Outlook and Product Definition

Global Leading Market Research Publisher QYResearch announces the release of its latest report *“Vehicle-mounted Hydrogen Storage System (Hydrogen Storage Tank or Hydrogen Storage Bottle) – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”*. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Vehicle-mounted Hydrogen Storage System market, including market size, share, demand, industry development status, and forecasts for the next few years.

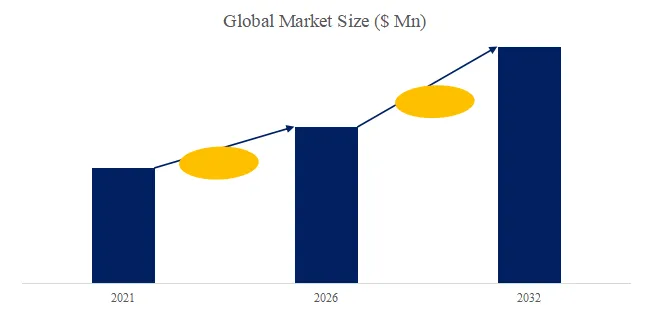

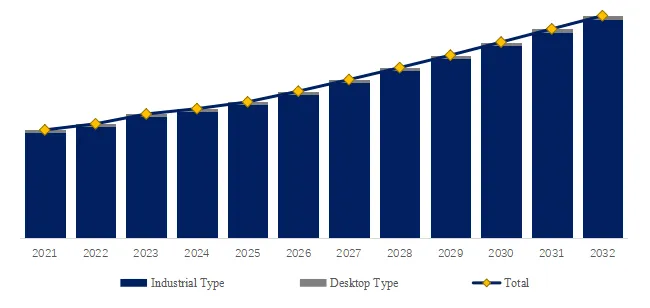

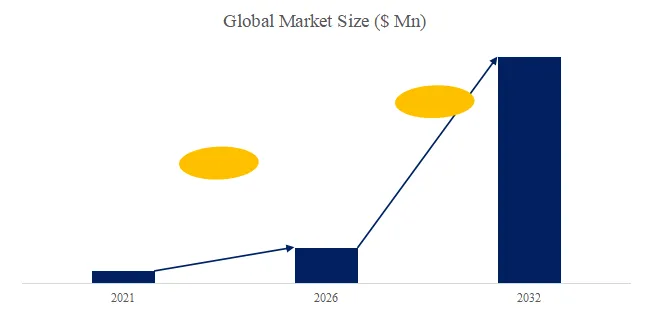

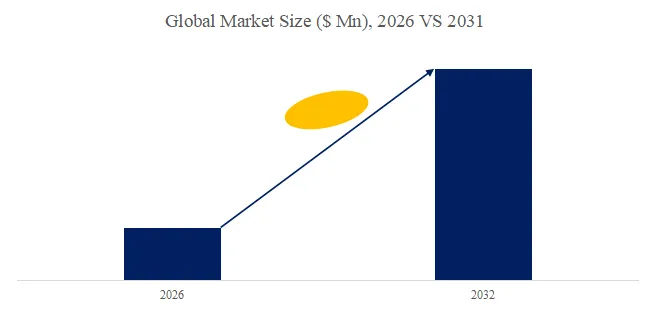

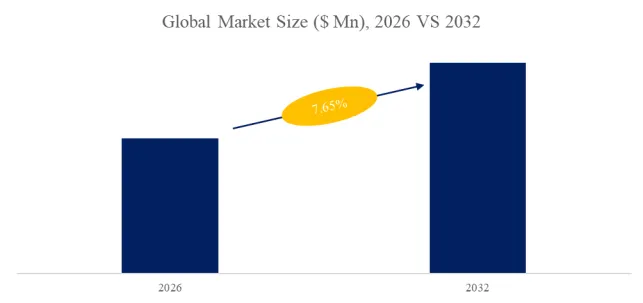

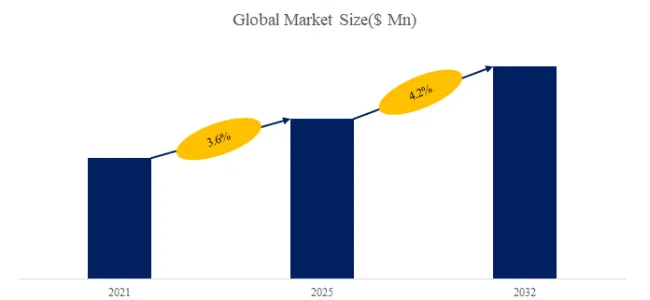

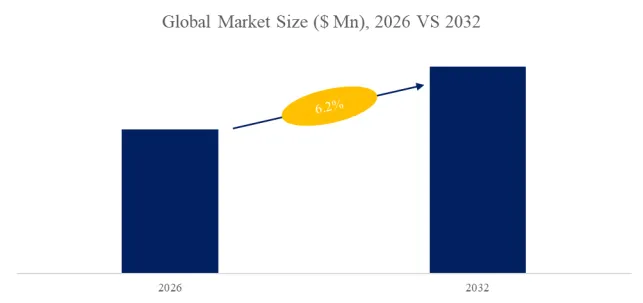

The global market for Vehicle-mounted Hydrogen Storage System was estimated to be worth US980millionin2025andisprojectedtoreachUS980millionin2025andisprojectedtoreachUS 4,200 million by 2032, growing at a CAGR of 23.1% from 2026 to 2032.

Product Definition: The vehicle-mounted hydrogen storage system (hydrogen storage tank or hydrogen storage bottle) is a device that stores hydrogen inside a vehicle. Hydrogen storage tanks or bottles are made of high-strength materials (carbon fiber composite, aluminum liner, polymer liner), and their design and manufacturing must meet international standards (ISO 19881, EC79, GTR13, ANSI HGV 2) to ensure safety and reliability. Hydrogen is a clean, efficient energy source that can reduce vehicle emissions and fossil fuel dependence. With continued technology development and cost reduction, vehicle-mounted hydrogen storage systems will see wider adoption.

Key Safety and Performance Standards:

| Standard | Region | Key Requirements |

|---|---|---|

| ISO 19881 | International | Gaseous hydrogen land vehicle fuel containers |

| EC79/EC 406 | Europe | Hydrogen-powered vehicle component approval |

| GTR13 | UN Global | Hydrogen and fuel cell vehicle safety |

| ANSI HGV 2 | USA | Compressed hydrogen gas containers |

Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/5933408/vehicle-mounted-hydrogen-storage-system–hydrogen-storage-tank-or-hydrogen-storage-bottle

Key Market Drivers and FCEV Expansion

1. Fuel Cell Electric Vehicles (FCEV) (55% of market demand): Toyota Mirai, Hyundai Nexo, Honda CR-V e:FCEV, BMW iX5 Hydrogen, and heavy-duty trucks (Hyundai XCIENT, Nikola Tre) require 3–10 hydrogen storage tanks per vehicle. Global FCEV fleet exceeded 75,000 units in 2025; projected to reach 500,000+ by 2030 (Hyundai, Toyota, Daimler Truck, Volvo, China’s Foton, SAIC).

2. Heavy-Duty and Commercial Transport (30% of market demand): Class 8 hydrogen trucks, buses, trains (Alstom Coradia iLint), and port equipment require larger storage capacity (50–100 kg hydrogen per vehicle). Heavy-duty is fastest-growing segment (35% CAGR).

3. Industrial and Material Handling (10% of market demand): Hydrogen forklifts (Toyota, Hyster-Yale, Linde, Crown) use onboard storage for warehouse operations. Over 50,000 hydrogen forklifts in operation globally by 2025.

4. Aerospace and Marine (5% of market demand): Hydrogen aviation and maritime prototypes in development; longer-term market.

Regional Consumption: Asia-Pacific leads with 52% market share (South Korea 22%, Japan 18%, China 12%), driven by government hydrogen strategies and FCEV production. North America holds 20% (California, heavy-duty trucks). Europe accounts for 18% (Germany, France, UK, Scandinavia). China is fastest-growing at 35% CAGR.

Market Segmentation: Storage Type and Application

By Hydrogen Storage Type:

| Type | Market Share (2025) | Pressure | Gravimetric Density (wt%) | Volumetric Density (g/L) | Applications | Growth Rate |

|---|---|---|---|---|---|---|

| Gas Hydrogen (Compressed) – Type III | 25% | 350-700 bar (5,000-10,000 psi) | 3.5–4.5% | 25–35 | Early FCEVs (older models), buses | 18% |

| Gas Hydrogen (Compressed) – Type IV | 65% (largest, fastest-growing) | 350-700 bar | 5.0–6.5% | 35–45 | All current FCEVs (Toyota Mirai, Hyundai Nexo), heavy trucks | 25% |

| Liquid Hydrogen (Cryogenic) | 8% | 1-5 bar (cryogenic, -253°C) | 10–15% (higher) | 50–60 | Heavy trucks (Nikola), aviation, marine | 20% |

| Solid Hydrogen (Metal Hydride) | 2% | Low pressure (<10 bar) | 1–2% (low) | 40–60 | Niche (forklifts, stationary) | 15% |

Type IV Composite Cylinder Construction: Polymer liner (typically high-density polyethylene or polyamide) for hydrogen permeation barrier, wrapped with carbon fiber/epoxy composite (structural strength), then outer protective layer (glass fiber or polymer). Type IV is the industry standard for modern FCEVs due to lowest weight (50-70% lighter than all-metal Type I/II) and highest gravimetric density.

By Application:

| Application | Market Share (2025) | Key Requirements | Typical Storage Capacity | Growth Rate |

|---|---|---|---|---|

| Industrial (Forklifts, Port Equipment) | 10% | Low pressure (350 bar), smaller tanks (1-5 kg H₂) | 1–5 kg | 20% |

| Energy (FCEV, Heavy Trucks, Buses, Trains) | 85% | High pressure (700 bar), large tanks (5-50 kg H₂), long cycle life (15,000+ fills) | 5–50 kg | 24% |

| Others (Marine, Aerospace) | 5% | Liquid hydrogen (cryogenic), large capacity (50-200+ kg) | 50–200+ kg | 30% |

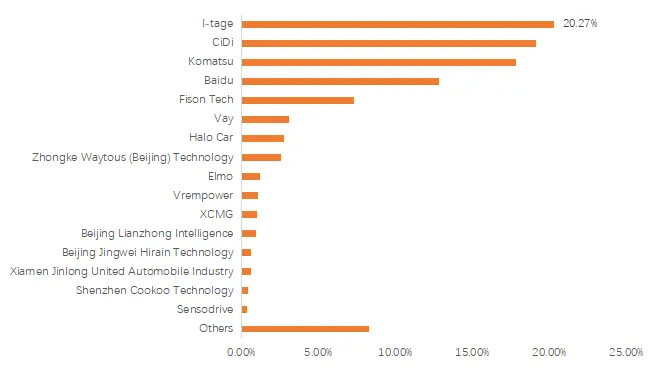

Competitive Landscape and Key Players (2025–2026 Update)

Market moderately concentrated, with top 15 players holding 55% share. Leading companies include:

| Company | Headquarters | Market Share | Key Specialization |

|---|---|---|---|

| Hexagon Purus | Norway | 12% | Type IV composite cylinders; heavy-duty truck and bus leader |

| Luxfer Gas Cylinders | UK/USA | 10% | Type III and Type IV; automotive and industrial |

| Toyota | Japan | 8% | Captive production for Mirai; also supplies other OEMs |

| Faurecia (Michelin JV Symbio) | France | 7% | Hydrogen storage systems for heavy-duty |

| Plastic Omnium | France | 6% | Type IV tanks; European market leader |

| NPROXX (Cummins JV) | Germany | 5% | Heavy-duty rail and truck storage |

| ILJIN Composite | South Korea | 5% | Type IV tanks for Hyundai Nexo (captive + external) |

| Linde Group | Germany | 4% | Integrated storage + fueling infrastructure |

| Air Liquide | France | 4% | Cryogenic liquid hydrogen storage (marine, aviation) |

| Jiangsu Guofu Hydrogen Energy | China | 4% | Domestic Chinese leader; Type III and Type IV |

| CIMC Enric Holdings | China | 3% | Large-scale composite cylinders; industrial and transport |

| Sinoma Science & Technology | China | 3% | Carbon fiber and composite cylinder manufacturing |

Other players: Worthington Industries, MSA, ECS, JMC, YAPP Automotive Systems, Jindun, Quantum Fuel Systems, JFE Holdings, Steelhead Composites, JG Automotive, Doosan, MAHYTEC, Shandong Auyan New Energy Technology, Beijing Jingcheng Machinery Electric, Beijing Kotech Technology, Shanghai Sunwise Energy Systems.

User Case Example (FCEV Passenger – Toyota Mirai): Toyota Mirai (2021–2025 model) uses three Type IV hydrogen storage tanks (one under rear seats, two in rear trunk). Total capacity: 5.6 kg H₂ at 700 bar. Tank specifications: carbon fiber/epoxy composite with polyamide liner, outer diameter 350-400mm, length 800-1,200mm. Weight: 85 kg (tanks only). Range: 402 miles (EPA). Refueling time: 3–5 minutes. Tank certification: 15-year life, 15,000 fills, burst pressure 2.25x operating (1,575 bar), leak rate <1 NmL/hour/L. Cost per tank (2025): 2,800–3,500.Toyotatargetfor2030:2,800–3,500.Toyotatargetfor2030:1,500–2,000 per tank (50% reduction).

User Case Example (Heavy-Duty Truck – Hyundai XCIENT Fuel Cell): Hyundai XCIENT Class 8 hydrogen truck uses 10 Type IV tanks (700 bar, total 35 kg H₂). Tanks mounted along chassis rails (both sides). Range: 400+ miles (GVW: 80,000 lbs). Refueling: 15–20 minutes (higher flow rate than passenger cars). Tank cycle life: 20,000 fills (fleet operation: 10+ years). Certified to ECE R134 (European) and FMVSS 304 (US). Fleet operator (Swiss) reports 98% uptime, with tank inspection every 2 years (visual, pressure test). Tank cost: 25,000–35,000pertruck(2025).Target:25,000–35,000pertruck(2025).Target:12,000–15,000 by 2030.

Technology Spotlight: Type IV Composite vs. Type III Metal-Lined Cylinders

| Parameter | Type III (Aluminum Liner + Carbon Fiber Wrap) | Type IV (Polymer Liner + Carbon Fiber Wrap) |

|---|---|---|

| Liner material | Aluminum (6061) | Polymer (HDPE, polyamide, PA6/PA66) |

| Weight (70L, 700 bar) | 80–100 kg | 50–70 kg |

| Gravimetric density (wt% H₂) | 3.5–4.5% | 5.0–6.5% |

| Hydrogen permeation | Very low | Low (liner acts as permeation barrier) |

| Operating temperature | -40°C to +85°C | -40°C to +85°C (polyamide has higher limit than HDPE) |

| Cost (per kg H₂ capacity) | $2,500–3,500/kg H₂ | $2,000–2,800/kg H₂ |

| Cycle life (fills) | 10,000–15,000 | 10,000–15,000 |

| Market share (2025) | 25% (declining) | 65% (increasing, fastest-growing) |

Manufacturing Process (Type IV):

- Liner blow molding or injection molding (polyamide/HDPE).

- Neck machining (metal boss for valve attachment).

- Filament winding (carbon fiber/epoxy resin wound over liner in helical and hoop patterns).

- Curing (heat to crosslink epoxy, 120-150°C).

- Hydrostatic testing (1.5x operating pressure, 1,050 bar for 700 bar tank).

- Burst testing (sample from each batch, 2.25x operating pressure, 1,575 bar).

- Helium leak testing (<1 NmL/hour/L).

- Approval and certification (ISO 19881, EC79, GTR13).

Technical Challenge: Carbon Fiber Cost and Availability. Carbon fiber represents 60-75% of Type IV tank cost. High-quality aerospace-grade carbon fiber (T700, T800) is used. Market demand for carbon fiber is growing faster than supply. New capacity coming online (Toray, Teijin, Mitsubishi, Hexcel, Solvay, Zoltek) but lead times for new production lines are 3–5 years. Hydrogen storage consumes 15% of global carbon fiber by 2030 (up from 3% in 2025). Recycling of end-of-life tanks (carbon fiber reclamation) is developing but not yet commercial at scale.

User Case Example (Bus – Hydrogen Fuel Cell Bus): New Flyer Xcelsior CHARGE H2 bus (US) uses 6 Type IV tanks (700 bar, total 30 kg H₂). Tanks roof-mounted (enables more interior space for passengers). Range: 300 miles (urban driving). Each tank: 200L volume, 110kg weight. Tank cost (2025): 12,000pertank(12,000pertank(72,000 total). FTA Low-No Program grant covers 40% of vehicle cost. Bus operators report 8-year tank life, 20,000 operating hours between inspections.

Industry-Specific Insights: Passenger FCEV vs. Heavy-Duty Truck vs. Bus Storage Requirements

| Parameter | Passenger FCEV (Mirai, Nexo) | Heavy-Duty Truck (Class 8) | Transit Bus |

|---|---|---|---|

| Typical H₂ capacity | 5–6 kg | 30–50 kg | 20–40 kg |

| Number of tanks | 2–3 | 8–12 | 5–8 |

| Pressure | 700 bar | 700 bar (350 bar for older) | 350-700 bar |

| Tank placement | Under seats, trunk | Chassis rails (sides) | Roof |

| Refueling time | 3–5 minutes | 15–25 minutes | 10–15 minutes |

| Tank cycle life | 15,000 fills (15 years) | 20,000 fills (10-12 years) | 15,000 fills (12 years) |

| Cost per kg H₂ capacity (2025) | $2,200–2,800 | $2,000–2,500 | $2,300–2,900 |

| 2030 cost target per kg | $1,200–1,800 | $1,000–1,500 | $1,200–1,800 |

Exclusive Observation: The 350 bar vs. 700 bar Trade-off. Heavy-duty trucks in Europe and Asia prefer 700 bar (higher range, more refueling stations). North American heavy-duty trucks initially adopted 350 bar due to simpler infrastructure (lower compressor cost), but the industry is converging to 700 bar (higher range, better TCO). 350 bar tanks are 20-30% cheaper (lower carbon fiber content) but store 50% less hydrogen for same volume, requiring more tanks or more frequent refueling. New truck models (2024+) standardize on 700 bar.

Technical Challenge: Thermoplastic vs. Thermoset Liners for Type IV Tanks.

| Liner Material | Advantages | Disadvantages | Adoption |

|---|---|---|---|

| HDPE (High-Density Polyethylene) | Lower cost, good permeation resistance | Lower temperature limit (-40°C to +85°C), less compatible with high-pressure cycling | Established (Hexagon Purus, Plastic Omnium) |

| Polyamide (PA6, PA66, PA610) | Higher temperature limit (-40°C to +120°C), better resistance to hydrogen embrittlement | Higher cost, moisture absorption (hygroscopic) | Emerging (Toyota, ILJIN, NPROXX) |

Polyamide liners are gaining share for high-cycle applications (heavy-duty truck, bus) due to higher temperature tolerance (better for fast filling). HDPE remains dominant for passenger FCEVs.

User Case Example (Rail – Alstom Coradia iLint Hydrogen Train): Alstom Coradia iLint (world’s first hydrogen passenger train) operates in Germany (Lower Saxony, 14 trains). Each train has two fuel cell modules (400 kW total) and 5 Type IV roof-mounted tanks (700 bar, total 50 kg H₂). Range: 1,000 km (621 miles) on flat terrain. Refueling: 15 minutes at terminal stations. Tank cost (2025): 25,000pertank(25,000pertank(125,000 total). The trains have replaced diesel units, reducing CO₂ emissions by 4,400 tons/year per train. Tank life: 12 years. Alstom reports 95% availability; tanks inspected annually (visual, acoustic emission).

Future Outlook and Strategic Recommendations (2026–2032)

Based on forecast calculations:

- CAGR of 23.1% (explosive growth from 12% in 2021–2025), driven by FCEV production scaling (500,000+ vehicles by 2030), heavy-duty truck decarbonization (zero-emission vehicle mandates in California, EU, China, Japan), and hydrogen fueling infrastructure expansion.

- Type IV composite cylinders will dominate (85% share by 2030), with Type III declining to 10% (legacy, specialty).

- 700 bar systems will become standard for all FCEV and heavy-duty (95% of new vehicles by 2030).

- Average selling price per kg H₂ capacity expected to decline from 2,500/kgin2025to2,500/kgin2025to1,200-1,500/kg by 2030 (carbon fiber cost reduction, manufacturing scale, design optimization).

- Asia-Pacific remains largest market (52% share), with China growing fastest (35% CAGR) due to government hydrogen subsidies and domestic manufacturing.

Strategic Recommendations:

- For Automotive OEMs (FCEV Programs): Specify Type IV 700 bar tanks for new vehicle platforms (best weight-to-storage ratio). For passenger cars, target tank cost <2,000pervehicle(2,000pervehicle(0.30-0.40/Wh equivalent). For heavy-duty trucks, negotiate long-term supply agreements with carbon fiber manufacturers (lead times: 12–18 months). Validate tank integration for crash safety (UN R134, FMVSS 304) early in design cycle.

- For Tank Manufacturers: Scale Type IV production capacity to meet 2030 demand (20x 2025 volumes). Invest in polyamide liner technology for high-cycle applications. Reduce carbon fiber waste (filament winding optimization, dry fiber placement) to lower cost. Develop tank refurbishment and end-of-life recycling programs (carbon fiber reclamation) to address upcoming service life expirations (first generation tanks 2015–2020 now reaching 15-year life).

- For Fleet Operators (Truck, Bus, Rail): For heavy-duty trucks, specify 700 bar tanks (future-proof for longer range, infrastructure convergence). Validate tank inspection procedures (visual, acoustic emission, hydrostatic) with local regulators. Plan tank replacement at 15-year/20,000-cycle intervals.

- For Investors: Hydrogen storage is the fastest-growing segment in the hydrogen value chain (23% CAGR). Target Type IV tank manufacturers with secured carbon fiber supply chains (Hexagon Purus, NPROXX, Faurecia, Plastic Omnium). Chinese manufacturers (Guofu, CIMC, Sinoma) poised for domestic market growth. Monitor carbon fiber capacity announcements (new lines from Toray, Teijin, Zoltek) as supply/demand balance impacts tank pricing.

- Monitor technology developments: Type V tanks (linerless all-composite) are emerging for stationary storage; may transition to onboard by 2030 (lower weight, higher pressure). Liquid hydrogen (cryogenic) for heavy-duty trucks (Nikola) and aviation (ZeroAvia) may capture 15-20% of heavy segment by 2035 if liquefaction efficiency improves (currently 30-40% energy loss). Solid hydrogen (metal hydride, MOF) for forklifts and low-pressure applications remains niche.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp