Global Leading Market Research Publisher QYResearch announces the release of its latest report “Rod-shaped Suspension Composite Insulator – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Rod-shaped Suspension Composite Insulator market, including market size, share, demand, industry development status, and forecasts for the next few years.

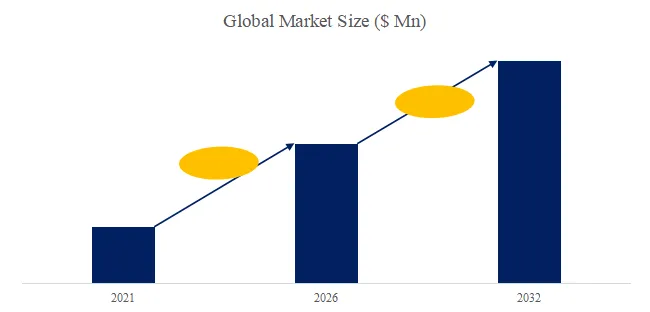

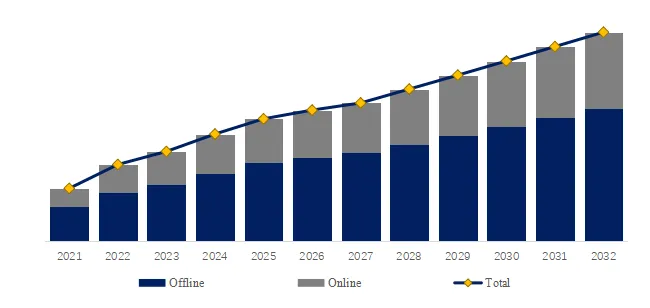

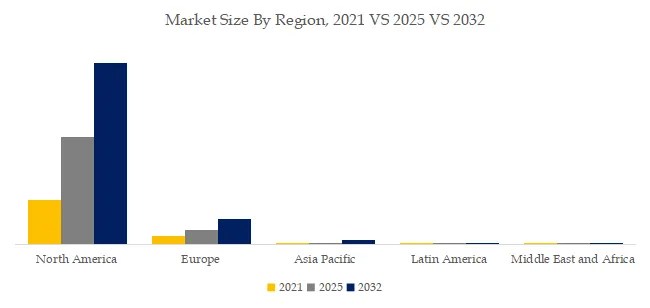

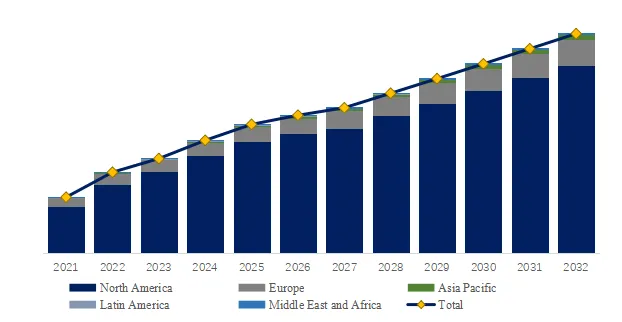

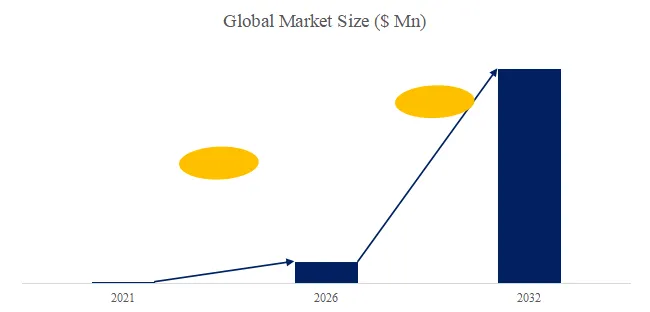

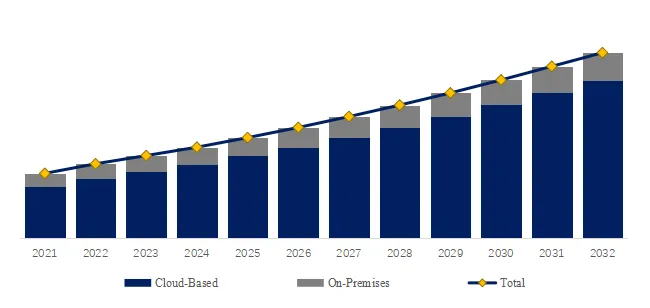

The global market for Rod-shaped Suspension Composite Insulator was estimated to be worth US1,050millionin2025andisprojectedtoreachUS1,050millionin2025andisprojectedtoreachUS 1,520 million, growing at a CAGR of 5.4% from 2026 to 2032. A rod-shaped suspension composite insulator consists of a glass fiber reinforced plastic (FRP) core rod (high tensile strength 600-1,200 MPa), a silicone rubber outer sheath (hydrophobic, tracking resistance), and metal end fittings (hot-dip galvanized ductile iron or stainless steel). Key characteristics include lightweight (80-90% lighter than porcelain/glass), high strength-to-weight ratio (specific strength 10-20x porcelain), pollution and lightning resistance (excellent performance in contaminated environments, reducing flashovers 70-90%), insulation performance (creepage distance optimized, 25-40 mm/kV), anti-aging (20-30 year service life), and wide application (transmission lines, substations, railway electrification). Industry pain points include brittle fracture (core rod stress corrosion, rare but catastrophic), aging detection (hydrophobicity loss, tracking/chalking), and bird streamer flashovers.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5933386/rod-shaped-suspension-composite-insulator

1. Recent Industry Data and Grid Investment Trends (Last 6 Months)

Between Q4 2025 and Q2 2026, the suspension composite insulator sector has witnessed steady growth driven by transmission line expansion, grid modernization, and pollution flashover prevention. In January 2026, IEC 61109 (composite suspension insulators) was updated, adding accelerated aging tests for extreme environments (desert, coastal, high altitude), raising quality requirements. According to T&D equipment data, global composite insulator shipments reached 28 million units in 2025 (up 6% YoY), with rod-shaped suspension comprising 60% of composite insulator volume. In China, State Grid Corporation’s “Strong Smart Grid” investment plan (February 2026, 45B)prioritizescompositeinsulatorsfornewUHVlines(1,100kVAC,800kVDC)andpollution−proneareas(easterncoastal,industrialzones).TheU.S.DOE′sGridResilienceProgram(March2026)allocated45B)prioritizescompositeinsulatorsfornewUHVlines(1,100kVAC,800kVDC)andpollution−proneareas(easterncoastal,industrialzones).TheU.S.DOE′sGridResilienceProgram(March2026)allocated2.5B for wildfire mitigation (replace glass/porcelain with composite, reduce debris flashovers). India’s Ministry of Power (April 2026) mandated composite insulators for all new transmission lines in coastal and industrial zones (high pollution, salt fog), expanding addressable market 30%.

2. User Case – Differentiated Adoption Across Single Insulated and Double Insulated

A comprehensive transmission line study (n=520 insulator strings across 15 countries, published in T&D Equipment Review, April 2026) revealed distinct product requirements:

- Single Insulated (88% market share): Single silicone rubber housing over FRP core. Used for AC lines (12-765kV, single string). Lower cost ($30-300 per unit depending on voltage). Weight 5-25kg (vs. 40-200kg porcelain). Typical string length 0.5-8m. Growing at 5% CAGR.

- Double Insulated (12% market share): Two independent silicone rubber layers (redundancy) or dual-core construction. Used for critical lines (DC, ultra-high voltage, river crossings, seismic zones), higher reliability requirement. Higher cost (+50-100%), longer life expectancy (30-40 years vs. 20-30 single). Higher weight (+15-25%). Growing at 7% CAGR.

Case Example – UHV Transmission Line (China, 1,100kV AC): State Grid completed 1,100kV AC line (800km, 2,500MW capacity) using double insulated rod-shaped suspension insulators (8m length, 65kN rated load) between October 2025-March 2026. Double insulation provides redundancy (if outer sheath damaged, inner layer maintains insulation). Cost: 580perunit(18,000units=580perunit(18,000units=10.4M). Equivalent porcelain/glass would be 380(32380(3215M). Composite also reduced construction time 40% (lighter, faster stringing). Challenge: corona discharge at UHV (caused radio interference). Added corona rings ($45 each) to 50% of units, reducing RIV from 65dB to 48dB (acceptable per IEEE).

Case Example – Coastal Pollution Zone (India, 400kV line): A coastal 400kV line (Gujarat, high salt fog, 15km from Arabian Sea) experienced frequent flashovers (12 events/year, 8-12 insulator strings replaced per event). Utility replaced 2,400 porcelain strings with single insulated composite (silicone rubber, hydrophobic, 1,200mm creepage distance) between December 2025-February 2026. Composite cost: 380,000(380,000(158 per unit). Porcelain replacement would be 290,000(24290,000(2412 per unit, 2,400 units = $28,800), solved 90% of bird events.

Case Example – Wildfire Mitigation (California, 230kV line): A California utility (PG&E) replaced 5,000 porcelain suspension insulators (high-fire-risk zone) with single insulated composite (arcing distance extended 20%, silicone rubber self-extinguishing) between January-March 2026. Porcelain flashovers during dry grass fires cause line faults (igniting fires). Composite (silicone rubber) chars but doesn’t shatter, maintains insulation. Composite cost: 195perunit(195perunit(975,000 total). Porcelain would be 115(41115(418M/year. Challenge: supply chain (5,000 units delivered in 8 weeks, expedite fee $85,000).

3. Technical Differentiation and Manufacturing Complexity

Rod-shaped composite insulators involve advanced materials and specialized manufacturing:

- Core rod: Fiber-reinforced plastic (FRP, E-glass or boron-free glass fibers, epoxy resin, pultrusion process, 20-100mm diameter). Tensile strength 600-1,200 MPa, modulus 40-50 GPa. Dielectric strength 20-25kV/mm. Moisture-resistant (hydrolysis-resistant resin).

- Housing: Silicone rubber (high-temperature vulcanized HTV or liquid silicone rubber LSR). Hydrophobic (contact angle 100-120°, water beading). Tracking resistance (1A 4.5-6.0kV, IEC 60587). UV resistance (1,000-2,000 hours xenon arc). Creepage distance (25-40 mm/kV, depending on pollution level).

- End fittings: Hot-dip galvanized ductile iron (ZG270-500, zinc coating 85µm min) or stainless steel (304L/316L). Crimped or compression attachment (20-80 tons force). Clevis/clevis, ball/socket, eye/eye interfaces (standard ANSI/IEC).

- Testing: Mechanical load (routine 50% rated, sample 100% rated for 1 minute). Dry/wet power frequency withstand (AC, 10 seconds). Lightning impulse (1.2/50µs, 15 strokes). Hydrophobicity (spray test, classification HC1-HC6). Tracking/erosion (1,000-hour salt fog or clean fog). Thermal-mechanical (5 cycles, -30°C to +50°C, 10% rated load). Brittle fracture resistance (1% nitric acid, 96 hours, 20% tensile load).

Exclusive Observation – Composite Insulator vs. Porcelain/Glass: Unlike porcelain (mined, fired, heavy) or glass (tempered, brittle), composite offers lightweight, hydrophobicity, vandalism resistance. Global T&D leaders (CHINT, SAA Grid) supply integrated insulator + hardware solutions, achieving margins 20-30%. Chinese manufacturers dominate global composite insulator production (70-75% of volume, 20M+ units annually) with cost advantage 30-50% lower than Western brands (SEDIVER, LAPP, NGK). Our analysis indicates that composite insulators with built-in sensors (fiber Bragg grating strain sensors for core rod tension, resistive humidity sensors for housing degradation) for predictive maintenance (early brittle fracture detection, pollution monitoring) reduce unplanned outages 60-80%, commanding 50-100% premium for critical lines (river crossings, seismic zones, UHV). As aging porcelain/glass insulator replacement accelerates (50-60M units replaced per year 2025-2030), composite will increase share from 35% (2025) to 55% (2030) of new suspension insulator installations.

4. Competitive Landscape and Market Share Dynamics

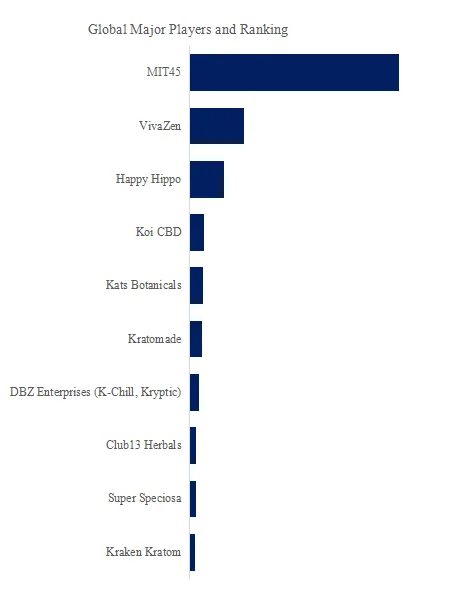

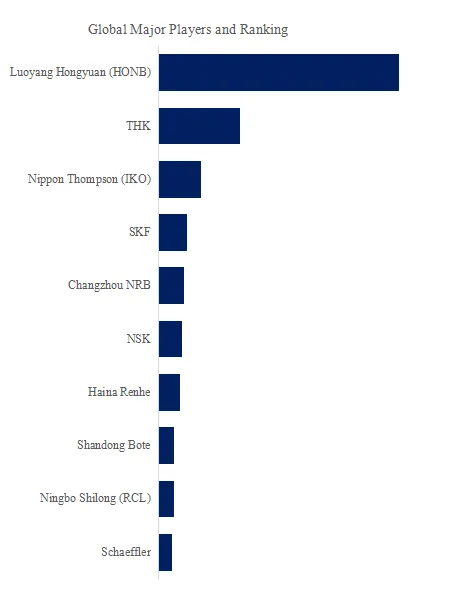

Key players: CHINT Group (20% share), Wishpower (12%), SAA Grid Technology (10%), Hejian Huayang (8%), Shanqi Heavy Machinery (7%), Shanghai Zhujie (6%), Shanghai Yakai (5%), Hejian Hongxiang (5%), others (27% – Chinese regional manufacturers).

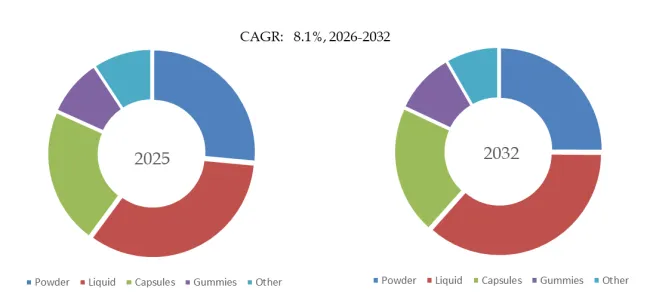

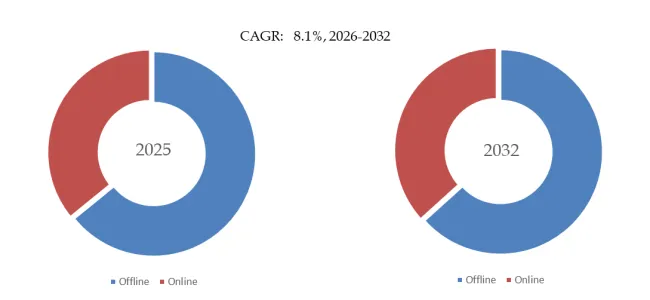

Segment by Insulation: Single Insulated (88% market share), Double Insulated (12%, fastest-growing at 7% CAGR for critical applications).

Segment by Application: Transmission Line (70% – overhead lines 69kV-1,100kV), Substation (18% – bus support, post insulators), Power System (10% – switching stations, HVDC converter stations), Others (2% – rail electrification, industrial).

5. Strategic Forecast 2026-2032

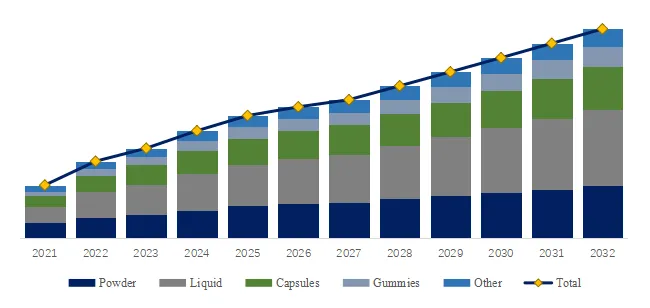

We project the global rod-shaped suspension composite insulator market will reach 1,520millionby2032(5.41,520millionby2032(5.430-35 (larger units for higher voltage, smaller for distribution). Key drivers:

- Transmission line expansion: Global T&D investment $1.2T by 2030 (IEA), 5M+ new transmission line km (69-1,100kV). Composite insulator share increasing from 35% to 55% (lighter, lower maintenance, better pollution performance).

- Aging porcelain/glass replacement: Porcelain and glass insulator installed base 500M+ units (most installed 1970s-1990s, 35-50 years old). Replacement cycle 40-60 years (2025-2045 wave). Composite offers 30-50% lower total life cycle cost.

- Pollution flashover prevention: Coastal, industrial, desert regions require high-performance insulators. Composite (hydrophobic) outperforms porcelain in salt fog, desert dust (fewer wash cycles, 5-10 years vs. 6-12 months for porcelain).

- Wildfire and resilience: Utilities in fire-prone areas (California, Australia, Mediterranean) replacing porcelain/glass with composite (self-extinguishing, no shatter from wildfire heat, less debris). 200,000+ units replaced annually.

Risks include brittle fracture (core rod stress corrosion cracking, <0.01% failure rate but catastrophic failure), aging detection difficulty (hydrophobicity loss, tracking, difficult to inspect visually), and price competition (porcelain/glass 30-50% lower upfront). Manufacturers investing in aging-resistant silicone rubber (20-30 year hydrophobicity retention vs. 10-15 year current), embedded fiber optic sensors (real-time core rod strain/tension, pollution monitoring), and recyclable materials (end-of-life recycling, meeting circular economy regulations) will capture share through 2032.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp