QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “ESD Shipping Boxes- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global ESD Shipping Boxes market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for ESD Shipping Boxes was estimated to be worth US$ million in 2024 and is forecast to a readjusted size of US$ million by 2031 with a CAGR of %during the forecast period 2025-2031.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/4567253/esd-shipping-boxes

ESD Shipping Boxes Market Summary

ESD shipping boxes were developed to address the problem of electrostatic discharge (ESD) buildup and subsequent damage to ESD-sensitive products such as electronic components and semiconductor wafers during transportation and storage. Since the establishment of ESD protection standards in the 1980s, they have evolved into core protective equipment covering various structures, including injection molded and hollow boards, and are widely used in electronics manufacturing, automotive electronics, semiconductors, and medical equipment. They release static charge through conductive materials, preventing potential differences.

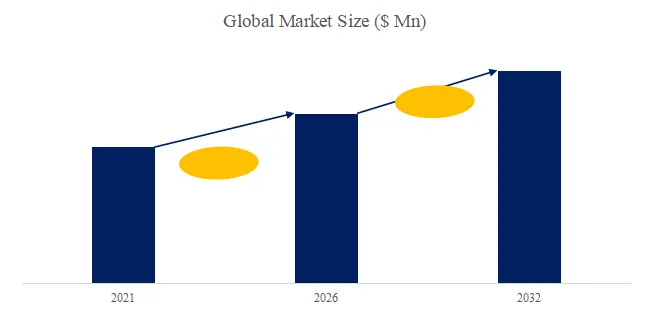

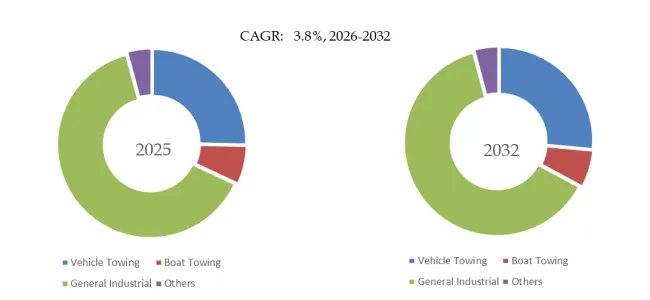

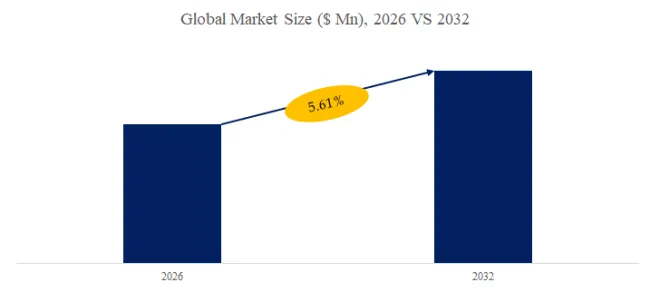

According to the new market research report “Global ESD Shipping Boxes Market Report 2021-2032”, published by QYResearch, the global ESD Shipping Boxes market size is projected to reach USD 0.78 billion by 2032, at a CAGR of 5.6% during the forecast period.

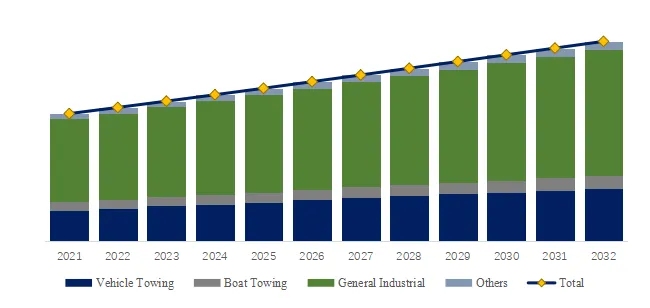

Figure00001. Global ESD Shipping Boxes Market Size (US$ Million), 2026-2032

Above data is based on report from QYResearch: Global ESD Shipping Boxes Market Report 2021-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

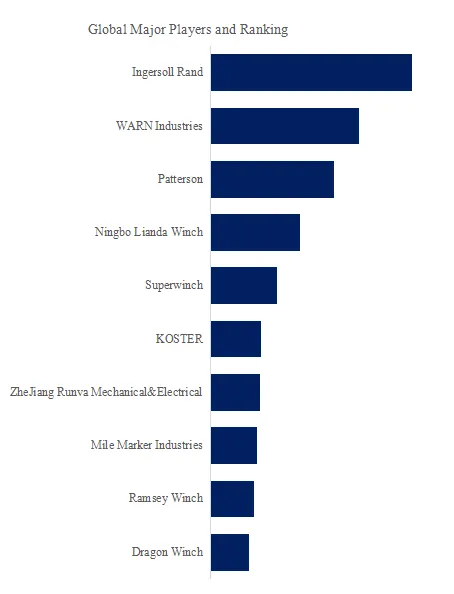

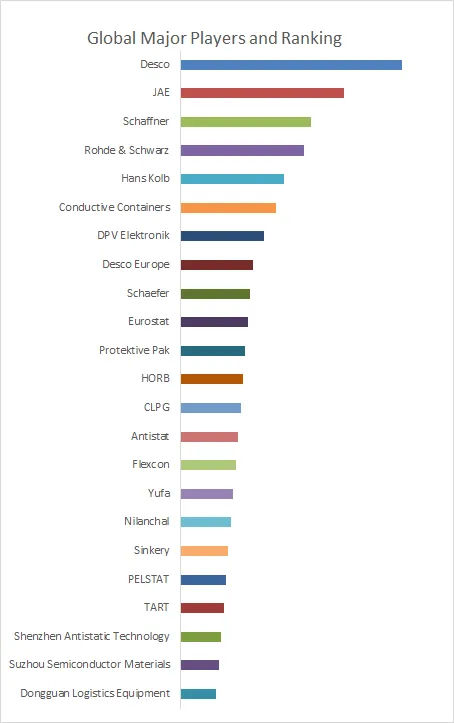

Figure00002. Global ESD Shipping Boxes Top 23 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global ESD Shipping Boxes Market Report 2021-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

Table 1. ESD Shipping Boxes Industry Chain Analysis

| Item | Description | |

| Upstream | Conductive Polypropylene | Conductive polypropylene is an antistatic polymer composite material made by blending and modifying polypropylene (PP) as the matrix resin with conductive fillers, conductive carbon black, or high-molecular conductive agents. While maintaining the advantages of polypropylene such as light weight, impact resistance, corrosion resistance, and easy molding, it imparts a stable surface resistivity, enabling it to dissipate static electricity and prevent static buildup. It is the main structural material for manufacturing ESD shipping boxes, providing a safe physical and ESD protection environment for static-sensitive components. |

| Carbon Nanotubes | Carbon nanotubes are one-dimensional nanoscale carbon materials formed by the hexagonal network of carbon atoms. They possess extremely high aspect ratios and excellent conductivity and mechanical properties. In ESD shipping boxes, they serve as highly efficient conductive additives. Even very low addition amounts can form a continuous conductive network within the polypropylene matrix, achieving uniform, stable, and low-penetration-limit static dissipation performance. Simultaneously, it improves the strength and heat resistance of the box, avoiding problems such as easy aging, resistance drift, and component contamination associated with traditional antistatic materials. It is a core modified component of high-end ESD packaging materials. | |

| Downstream | Electronics Manufacturing | ESD transport boxes are standard transport and storage containers for electrostatically sensitive components such as chips, wafers, PCBs, connectors, and sensors in the electronic manufacturing process. They effectively suppress the generation and release of static electricity, preventing electrostatic breakdown and dust accumulation that could cause device failure. They are widely used in SMT (Surface Mount Technology), packaging and testing, component assembly, and material handling to ensure the yield and reliability of electronic product manufacturing. |

| Automotive Electronics | Automotive electronics (such as ECUs, control modules, automotive chips, sensors, and wiring harness connectors) have stringent requirements for electrostatic and environmental reliability. ESD transport boxes are used throughout the entire process of automotive electronic component production, packaging, and delivery to vehicle manufacturers, providing stable electrostatic and mechanical protection. They meet the anti-static, anti-collision, moisture-proof, and aging-resistant requirements of automotive-grade components during transportation and storage, ensuring the safety and stability of automotive electronic systems. | |

| Medical Electronics | Medical electronic equipment (such as monitor modules, diagnostic chips, precision sensors, and implantable devices) is highly precise and directly related to life safety. ESD transport cases provide an anti-static, clean, disinfection-resistant, and pollution-free storage and transportation environment, preventing electrostatic damage to sensitive circuits while meeting the cleanliness and reliability requirements of the medical industry, ensuring the precision, safety, and lifespan of medical electronic equipment. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2025

Table 2. ESD Shipping Boxes Industry Policy Analysis

| Policy | Description | |

| 1 | “Electronic Components – Semiconductor Devices – Long-Term Storage – Part 6: Packaged or Coated Components” | This standard explicitly stipulates that packaged semiconductor devices must be transported using anti-static packaging materials (surface resistivity 1×10⁴~1×10¹¹Ω), and requires controlled temperature and humidity during transport (e.g., nitrogen protection for wafer transport, temperature 20-25℃, humidity <40% RH), while also establishing a traceability system for expiration dates. This standard directly relates to the material performance indicators of ESD transport boxes and the entire transportation process control. |

| 2 | EU EN 55024 Standard | It stipulates that information technology equipment (including electronic equipment in transport) must pass electrostatic discharge (ESD) immunity testing (contact discharge ±4kV, air discharge ±8kV), and requires the equipment to meet electromagnetic compatibility standards in the 0Hz-400GHz frequency band. This standard mandates EU market access and directly affects the design verification of ESD transport boxes exported to Europe. |

| 3 | “Silicon Wafer Packaging and Marking” | For upstream semiconductor silicon wafer products, regulations stipulate that transportation packaging must employ clean processes (such as anti-static blister packs + cardboard boxes for secondary packaging), and require packaging materials to pass anti-static performance verification (such as surface resistance testing). This standard directly regulates the material selection and structural design of silicon wafer transport boxes. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2025

Table 3. ESD Shipping Boxes Industry Development Trends

| Development Trends | Description | |

| 1 | Intelligent and Digital Upgrades | The proportion of products with built-in temperature, humidity, and static dissipation time monitoring chips increased from 12% in 2022 to 35% in 2025, enabling real-time transmission of environmental data to the cloud for dynamic risk warnings. Furthermore, RFID or QR code technology enables full lifecycle tracking, ensuring controllable exposure time for moisture-sensitive devices (MSDs). |

| 2 | Environmentally Friendly Materials and Circular Economy | The annual penetration rate of bio-based conductive plastics is increasing by 9%, replacing traditional toner/PP composite materials. If 100% recyclable HDPE is used, it can be recycled more than 500 times, complying with EU RoHS and China’s “dual-carbon” strategy. In addition, hollow board assembled models are 35% lighter than injection-molded models, and the foldable design reduces volume by 60% after folding, lowering logistics costs by 40%, making them suitable for cross-border e-commerce distribution scenarios. |

| 3 | Expanded Applications in Multiple Fields | The wafer-specific box can be used with 300mm cassettes, and its performance degradation is ≤5% in environments ranging from -40℃ to 85℃; the high-temperature resistant model can also be used with high-voltage components for new energy vehicles and has passed a 1.2-meter drop test; the medical electronics-specific box complies with FDA certification and has annual sales of over 1.2 million units. |

Source: Secondary Sources, Press Releases, Expert Interviews and QYResearch, 2025

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The ESD Shipping Boxes market is segmented as below:

By Company

Hans Kolb

Conductive Containers

DPV Elektronik

Desco Europe

Schaefer

Eurostat

Protektive Pak

HORB

CLPG

Antistat

Flexcon

Yufa

Nilanchal

Sinkery

PELSTAT

TART

Segment by Type

Corrugated ESD Shipping Boxes

Plastic ESD Shipping Boxes

Foam-lined ESD Shipping Boxes

Segment by Application

Electronics and Semiconductors

Telecommunications

Medical Devices

Others

Each chapter of the report provides detailed information for readers to further understand the ESD Shipping Boxes market:

Chapter 1: Introduces the report scope of the ESD Shipping Boxes report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of ESD Shipping Boxes manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various ESD Shipping Boxes market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of ESD Shipping Boxes in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of ESD Shipping Boxes in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth ESD Shipping Boxes competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides ESD Shipping Boxes comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides ESD Shipping Boxes market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global ESD Shipping Boxes Market Outlook, In‑Depth Analysis & Forecast to 2031

Global ESD Shipping Boxes Sales Market Report, Competitive Analysis and Regional Opportunities 2025-2031

Global ESD Shipping Boxes Market Research Report 2025

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp