QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “AI Insurance Claims Software- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global AI Insurance Claims Software market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for AI Insurance Claims Software was estimated to be worth US$ 115 million in 2025 and is projected to reach US$ 191 million, growing at a CAGR of 7.2% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5797592/ai-insurance-claims-software

AI Insurance Claims Software Market Summary

AI Insurance Claims Software is a software system that utilizes AI technologies such as computer vision, natural language processing, and machine learning to automate and intelligently decide on the entire insurance claims process. It transforms the traditional, lengthy, and error-prone claims process, which relies heavily on manual review, into a highly efficient, accurate, and standardized intelligent process by automatically identifying and extracting key information from claims materials, intelligently assessing and processing losses, identifying fraud risks, and optimizing the claims process. This software directly addresses the core challenges of high operating costs, poor customer experience, and significant fraud losses in the insurance industry. It can significantly shorten claims cycles, reduce claims expenses, improve payout accuracy, and enhance customer satisfaction, making it a key technological tool for the insurance industry to achieve digital transformation and cost reduction. Its core value lies in restructuring the traditionally human-driven claims process into a “data-driven, model-assisted, human-machine collaborative” intelligent decision-making system, thereby significantly shortening claims processing cycles, reducing fraud losses, optimizing customer experience, and improving operational efficiency. The system typically consists of image recognition modules (damage assessment photo analysis), text parsing modules (medical reports, accident descriptions), risk scoring engines (fraud detection), predictive models (claim amount estimation), and workflow automation platforms (case assignment and tracking). It enables end-to-end intelligence from claim reporting and document review to damage assessment, claims processing, and settlement payment. In major insurance lines such as auto, health, property, agricultural, accident, and liability insurance, AI Insurance Claims Software has become a core lever for insurance company digital transformation, with technological evolution focused on improving model accuracy, enhancing explainability, multi-modal data fusion, and deepening generative AI applications.

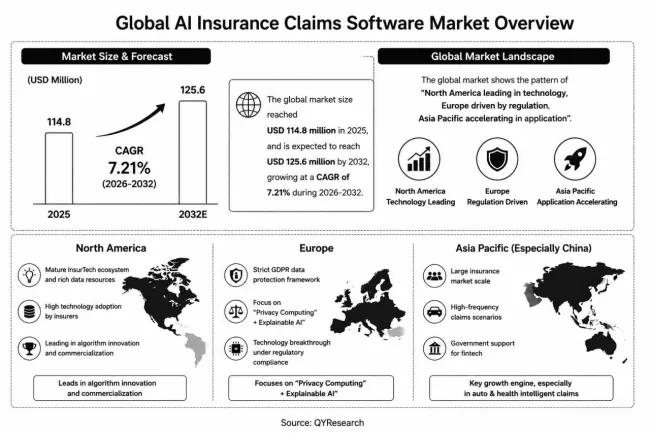

Driven by the accelerating digital transformation of the global insurance industry, continuously rising claims costs, and increasing customer expectations for instant service, the AI Insurance Claims Software market is undergoing a strategic transformation—from an “assistive tool” to a “core claims decision-making engine.” According to the latest data from QYResearch, the global market size reached US

114.8million in 2025 and is projected to climb to US 125.6 million by 2026, registering a steady CAGR of 7.21% from 2026 to 2032.

This growth is underpinned by three core factors: the urgent need of global insurance companies to compress claims operating costs and enhance fraud detection capabilities, breakthroughs in AI technologies for image recognition and text understanding, and regulatory requirements for claims transparency and fairness driving technology investment. However, the impact of global trade landscape changes in 2025 on the supply chain of AI computing chips and cloud services, coupled with challenges in insurance data privacy compliance and model explainability, is profoundly shaping the product structure and competitive landscape of the global AI Insurance Claims Software market. This report analyzes product functional classification, technology roadmap differentiation, and industry application characteristics, providing data-driven insights for strategic decision-making.

The global market presents a pattern of “North America leading in technology, Europe driven by regulation, and Asia-Pacific accelerating in application.” North America, its mature insurtech venture capital ecosystem, rich data resources, and high technological adoption rates among insurers, is at the forefront of algorithmic innovation and commercial deployment of AI Insurance Claims Software. Europe, under the strict GDPR data protection framework, focuses on breakthroughs in “privacy computing + explainable AI.” The Asia-Pacific region (especially China), relying on its huge insurance market scale, high-frequency claims scenarios, and government support for fintech, has become the core engine of global market growth, releasing significant incremental space particularly in the areas of auto and health insurance intelligent damage assessment.

Figure00001. Global AI Insurance Claims Software Market Size

Above data is based on report from QYResearch: Global AI Insurance Claims Software Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Technology Characteristics & Product Classification

The core technological value of AI Insurance Claims Software lies in transforming the “judgment-decision” stages of the traditional claims process, which rely on human experience, into quantifiable, reproducible, and optimizable model prediction processes, achieving the unity of efficiency improvement and risk control. Key technological trends include: 1. Enhanced multi-modal fusion capability, evolving from image or text analysis to joint reasoning across multiple data types such as “images + text + tables + voice.” For example, in auto insurance claims, simultaneously analyzing accident photos, dashcam video, police reports, and policyholder call recordings; 2. Deep embedding of generative AI into the claims process, using large language models to achieve automatic summarization of accident descriptions, assistance in drafting claims review opinions, automatic generation of claims reports, and natural language interaction with customers; 3. Extension of models from “post-event detection” to “pre-event early warning,” predicting fraud probability, estimation deviation, and litigation risk at the case intake stage based on historical data and real-time features, enabling differentiated allocation of claims resources.

By Deployment Type:

On Premise Software: Installed on the insurer’s own servers or private cloud, data remains within the insurer’s network boundary, meeting financial-grade data security and compliance requirements. Suitable for large insurance groups, state-owned insurers sensitive to data sovereignty, and institutions with customization capabilities. Advantages include data isolation and strong customizability, but disadvantages include high initial procurement costs, complex system maintenance, and longer AI model update cycles. Estimated average price: 300,000−1,000,000 USD per suite (priced by modules and user count).

Cloud-Based Software (SaaS): Provides AI claims functions on a subscription basis. Insurers do not need to build their own AI infrastructure, calling model services via APIs or web interfaces. Suitable for small and medium-sized insurers, internet insurance platforms, and projects for rapid AI capability validation. Advantages include low initial investment, rapid deployment, and continuous model updates, but require assessment of network latency, cross-border data compliance, and vendor lock-in risk. SaaS models are typically priced by API call or case volume, with estimated average price: 0.50−5 USD per case.

By Claims Process:

Automated Reporting and Processing: Automatically receives claims, classifies cases, extracts key information, and assigns adjusters or claims specialists through OCR, NLP, and conversational AI.

Optimized Damage Assessment and Estimation: Identifies damaged components via computer vision and estimates repair costs and medical expenses via predictive models, damage assessment recommendations for claims reviewer reference or automatic approval.

Optimized Claims Processing and Fraud Detection: Screens anomalous cases through rule engines + machine learning models, discovers fraud networks via knowledge graphs, and outputs risk scores and investigation recommendations.

Optimized Claims Settlement and Payment: Automatically calculates claim amounts, verifies policy terms, triggers payment processes, and supports direct payment integration with hospitals and repair shops.

Actual Procurement & Application Characteristics

The procurement process for AI Insurance Claims Software involves claims departments, IT departments, data departments, and compliance departments of property/casualty and life insurers. The process is highly specialized and depends on the enterprise’s IT architecture, data foundation, and business priorities, centering on model accuracy, system integration capability, data security compliance, and ROI assessment.

In the early procurement stage, insurers typically conduct a Proof of Concept (POC), testing the supplier’s model on the insurer’s sample data to evaluate core metrics such as model accuracy, recall, false positive rate, and processing speed. Suppliers must also pass security audits to meet insurer requirements for network security, data privacy, and model explainability. After validation, insurers typically adopt a hybrid model of annual subscription + pay-per-use or one-time procurement + maintenance service. Large insurance groups tend toward on-premise deployment + customized development to protect data and model intellectual property; small and medium-sized insurers prefer SaaS models to reduce initial investment.

In terms of procurement structure, auto and health insurance, due to their high claim volumes and standardized processes, have the highest penetration rates of AI claims software. Long-tail lines such as agricultural and liability insurance, due to high data unstructuredness and case volumes, are still in the exploration stage for AI applications. In the post-procurement phase, insurers continuously require suppliers to provide model retraining and version updates based on production performance (e.g., accuracy drift, false positive rate changes), forming a complete application system of “POC validation—pilot launch—full rollout—continuous optimization. ”

Tariff Policies & Supply Chain Restructuring

Changes in the global trade landscape in 2025 are having structural impacts on the AI Insurance Claims Software market:

1. AI Computing Chip Supply Chain Risks Transmit to the Software Layer. Training and inference of AI claims models rely on high-performance GPUs (especially NVIDIA series). Chip export controls may lead to higher computing costs or delivery delays for AI software suppliers in some regions. This drives companies in emerging markets like China to accelerate adaptation to domestic AI chips and promote the development of model lightweighting techniques (distillation, pruning, quantization), reducing dependence on high-end GPUs.

2. Cross-Border Cloud Service Regulation Affects SaaS Delivery Models. Insurance is a highly data-sensitive industry, and countries have increasingly strict regulations on financial data going abroad. Some countries require insurance customer data to be stored and processed domestically, forcing multinational AI software suppliers to establish localized cloud deployment nodes or partner with local cloud service providers in different markets, increasing delivery complexity and compliance costs.

3. Open Source Model Ecosystem Reduces Technology Dependency Risk. As the capabilities of open-source large models such as Llama, Qwen, and DeepSeek improve, insurers and AI software suppliers have more “non-proprietary” options when building claims NLP modules, reducing dependence on specific commercial APIs and enhancing supply chain resilience.

4. Model Intellectual Property Protection and Regionalization Strategies. Some insurers require AI model training and inference to be conducted entirely within their controllable environment to prevent leakage of commercially sensitive information through API calls. This promotes the popularity of “model local delivery” models rather than solely cloud API services.

Market Participant Competitive Landscape Analysis

Global participants in the AI Insurance Claims Software market exhibit a distinct multi-regional pattern of “North American innovators leading, European vertical specialists thriving, and Asia-Pacific giants competing across boundaries.”

North America is home to the most innovation-driven companies focused exclusively on insurance claims AI. Shift Technology (France/Global, leader in insurance fraud detection and claims automation, serving over 300 insurers worldwide), CLARA Analytics (NLP-based claims case management and risk prediction platform), EvolutionIQ (claims guidance and predictive analytics for disability and personal injury insurance), Tractable (UK/Global, benchmark enterprise in computer vision-based vehicle and property damage assessment), Claim Genius (auto insurance AI damage assessment) and image recognition), Gradient AI (predictive models for underwriting and claims optimization), Omni (claims experience and automation platform), Affinda (intelligent document processing for claims document recognition), Aiclaim (claims automation), and Assured (disability insurance claims platform). Legacy insurance software giants Guidewire Software and EIS Group are also integrating AI capabilities into their core systems, extending into claims through ecosystem partnerships or self-developed modules.

Europe and Asia-Pacific are also highly active. Qantev (health insurance claims AI, focusing on medical data analytics), Strala (AI-based claims and underwriting automation), Sprout (claims management platform), SS&C Blue Prism (RPA+AI for claims workflow automation), and Damco (cargo and logistics insurance claims) have built advantages in their respective niches. In Asia-Pacific, Ping An Technology (leveraging Ping An Group’s extensive claims scenarios and data to develop AI damage assessment and anti-fraud systems covering auto and health insurance), ZhongAn Technology (internet insurtech vendor providing SaaS AI claims platform), Sompo Japan (Japanese property insurer with self-developed AI claims system for auto and property insurance), and Newgen (business process automation + AI serving insurance clients across multiple countries) are key players. Additionally, EvolutionIQ focuses on disability insurance claims guidance and is growing rapidly in North America.

Downstream end demand is primarily composed of property insurers, health insurers, and comprehensive insurance groups. Auto and health insurance, due to their high claim frequency and relative standardization, are the most concentrated areas for AI claims software deployment. Agricultural, liability, and accident insurance also show significant incremental growth in specific markets and regions. The overall competitive ecosystem features “core system suppliers horizontally integrating AI capabilities” coexisting with “vertical AI newcomers deeply empowering claims scenarios.”

Future Development Outlook

In the future, AI Insurance Claims Software will continue to evolve around three main themes: claims process unmanned, risk assessment front-loading, and personalized customer experience, achieving broader market coverage driven by technological maturity, data ecosystem development, and regulatory framework improvement.

In the auto insurance claims field, with standardization of accident photo collection and digitization of repair price databases, AI damage assessment will upgrade from a “support tool” to an “autonomous engine,” enabling fully automatic claims for low-complexity cases (no human intervention from reporting to settlement). Simultaneously, the integration of video damage assessment and remote inspection will further improve case processing efficiency.

In the health/medical insurance claims field, with the standardization of electronic medical records and improved AI understanding of medical text, medical document review, cost reasonableness verification, and diagnosis-treatment plan matching analysis will achieve high automation. Generative AI will assist claims specialists in quickly understanding complex medical histories and treatment logic, shortening training cycles and improving decision-making consistency.

In the fraud detection field, the integration of knowledge graphs + graph neural networks + anomaly detection models will build a “real-time dynamic fraud risk network,” achieving the leap from “case-level” screening to “entity-level” (individuals, repair shops, hospitals, lawyers) relationship insight, significantly improving detection rates for gang fraud.

In the generative AI and agentic AI integration direction, future AI claims systems will be able to understand natural language instructions (e.g., “process Xiao Wang’s auto claim from last night”), automatically plan and execute required steps, and proactively request manual assistance with recommendations when encountering edge cases, achieving true “human-machine collaboration.”

In overseas markets, Chinese AI Insurance Claims Software companies (Ping An Technology, ZhongAn Technology, etc.) are leveraging scenario-validated technological capabilities to expand into Southeast Asia, the Middle East, and other markets, but must address differentiated challenges such as insurance regulation, language/culture, and data localization across different countries.

Overall, the AI Insurance Claims Software industry remains in a phase of parallel technology-driven and scenario-deepening growth. With the deepening of insurer digital transformation, continuous improvement of AI model capabilities, and rising customer expectations for instant claims, the long-term growth certainty of the industry is strong. AI Insurance Claims Software is expected to gradually upgrade from a “claims efficiency tool” to an “insurance operations intelligent hub.”

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The AI Insurance Claims Software market is segmented as below:

By Company

Affinda

Aiclaim

Assured

CLARA Analytics

Damco

EvolutionIQ

Gradient AI

Newgen

Qantev

Shift Technology

Sprout

SS&C Blue Prism

Strala

Ping An Technology

ZhongAn Technology

Tractable

Omni

Claim Genius

Guidewire Software

EIS Group

Sompo Japan

Segment by Type

On Premise Software

Cloud-Based Software

Segment by Application

Car Insurance Claims

Health Insurance/Medical Insurance Claims

Property Insurance Claims

Agricultural Insurance Claims

Accident Insurance Claims

Liability Insurance Claims

Others

Each chapter of the report provides detailed information for readers to further understand the AI Insurance Claims Software market:

Chapter 1: Introduces the report scope of the AI Insurance Claims Software report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of AI Insurance Claims Software manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various AI Insurance Claims Software market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of AI Insurance Claims Software in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of AI Insurance Claims Software in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth AI Insurance Claims Software competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides AI Insurance Claims Software comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides AI Insurance Claims Software market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global AI Insurance Claims Software Market Outlook, In‑Depth Analysis & Forecast to 2032

Global AI Insurance Claims Software Market Research Report 2026

Global AI Insurance Claims Software Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp