QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Ultra-High Purity Aluminum- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Ultra-High Purity Aluminum market, including market size, share, demand, industry development status, and forecasts for the next few years.

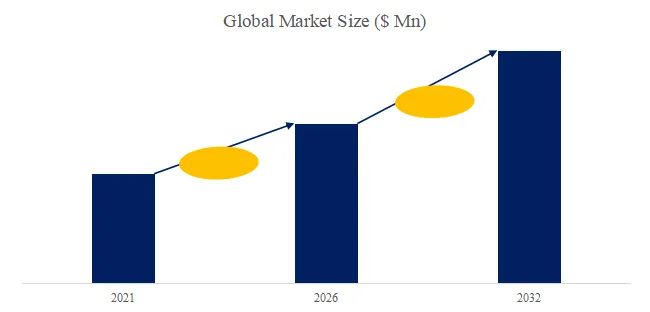

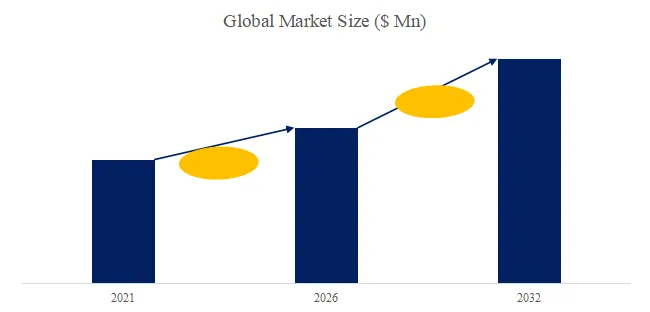

The global market for Ultra-High Purity Aluminum was estimated to be worth US$ 264 million in 2025 and is projected to reach US$ 513 million, growing at a CAGR of 8.6% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6605743/ultra-high-purity-aluminum

Ultra-High Purity Aluminum Market Summary

Ultra-High Purity Aluminum: From High-Purity Metal to a Strategic Base Material for Advanced Electronics

Ultra-high purity aluminum generally refers to aluminum materials with purity of 5N and above, meaning aluminum content of no less than 99.999%. Its value is not defined merely by a higher nominal purity figure, but by much tighter trace-impurity control, a cleaner elemental profile, stronger lot-to-lot consistency, and better traceability. Commercially, it can be supplied in multiple forms depending on downstream processing needs, including ingots, rods, slabs, and deposition-oriented upstream materials, serving semiconductors, display manufacturing, electronic components, and selected high-end functional-material applications. It is no longer a marginal premium product within the aluminum industry; it is increasingly being established as a critical base-material platform in advanced manufacturing.

The Market Center of Gravity Is Moving Upward, and Ultra-High Purity Aluminum Is Emerging as a Distinct High-End Growth Curve

Within the broader high purity aluminum market, 5N-and-above material is no longer just a supplementary premium layer. It is increasingly forming an independent high-end growth curve in value terms. According to QYResearch’s newly released Global Ultra-High Purity Aluminum Market Report 2025-2031, the global Ultra-High Purity Aluminum market is expected to reach USD 0.51 billion by 2031, registering a CAGR of 8.4% during the forecast period. This outlook is highly consistent with the strong expansion trend shown in the attached market report for 5N and 6N-and-above materials. The attachment indicates that in 2025, 5N material generated USD 186.02 million in revenue and 6N and above generated USD 77.83 million, together accounting for 48.69% of the total high purity aluminum market. By 2032, the combined value of these two categories is projected to rise to about USD 512.66 million. In other words, ultra-high purity aluminum has already moved from being the technological high ground of the sector to becoming a core engine of industry-wide value creation.

The importance of this shift is structural. Traditional high purity aluminum markets are largely built around scalable 4N supply, while the 5N-and-above segment reflects a deeper electronic-material identity and far stronger specification requirements. The key competitive question is no longer who can expand tonnage, but who can continuously deliver higher-purity, lower-impurity, and more stable material into semiconductor, display, and precision-electronics value chains. In QYResearch’s perspective, ultra-high purity aluminum is not simply an upgraded form of high purity aluminum; it is an upstream strategic platform within the advanced electronics materials system.

Figure00001. Global Ultra-High Purity Aluminum Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Ultra-High Purity Aluminum Market Report 2025-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

5N Defines Commercial Scale, While 6N-and-Above Defines the Technological and Profit Ceiling

The 5N tier remains the core commercial battlefield. The attached report states that 5N marks a major transition from general high-purity metal into ultra-high-purity electronic material. Key impurities such as Si, Fe, and Cu are tightened from the tens-of-ppm range in 4N material to low single-digit ppm or around 1 ppm in 5N material. That makes 5N better suited for applications requiring stronger thin-film quality, conductive-layer stability, and electrical consistency, including semiconductor-related materials, FPD/LCD material systems, and higher-specification electronic-material applications. By 2025, 5N accounted for 34.33% of total high purity aluminum market revenue and had already become one of the most important sources of value growth.

By contrast, 6N and above belong to a smaller but much more premium category. The report notes that 6N-grade material controls most metallic impurities in the 0.2–0.6 ppm range and is directly associated with higher conductivity, higher reflectivity, and low-temperature applications such as superconducting stabilizers. This means that 6N and above are not simply “purer aluminum,” but materials intended for extreme-performance, cryogenic, highly sensitive, and specialty functional uses. Their market size is smaller, but their significance for technological barriers, customer tiering, and industry profit structure is disproportionately high.

Semiconductor and Display Demand Is Repricing the Strategic Role of the Material

The strongest attraction of ultra-high purity aluminum lies in its close alignment with the upgrade cycle of semiconductors and next-generation display industries. The attached report shows that “Semiconductor and FPD Materials” had already become the largest application segment in 2025, reaching USD 194.52 million, clearly ahead of capacitor foil and other applications, and is projected to rise to USD 386.38 million by 2032. That makes it the single most important growth engine in the market.

Company product positioning reinforces the same trend. KM Aluminium has publicly disclosed that its 5N5 material is used as source material for semiconductor sputtering targets, while its 5N0 material serves LCD and OLED sputtering-target source-material applications. Nantong TADE’s product footprint spans 5N to 6N5 and extends into multiple ultra-high-purity forms aimed at semiconductor, flat-panel display, photovoltaic, and advanced thin-film material chains. The market is therefore no longer buying high purity aluminum simply as a metal; it is buying a material platform capable of supporting advanced deposition, precision manufacturing, and long-term process stability.

The Real Barrier Lies in Process Stability, Defect Control, and Customer Qualification

The difficulty of competing in ultra-high purity aluminum has never been just about achieving 5N purity. The attachment emphasizes that market-entry barriers are increasingly defined by a combination of purity control, defect control, microstructure control, product-form capability, and customer qualification, rather than by nominal purity alone. As purity levels rise, the cost center shifts away from basic metal feedstock and energy toward more complex refining routes, stricter testing and validation, lower tolerance for process deviation, and much longer customer qualification cycles. In semiconductor, flat-panel-display, and precision-electronics applications, customers care not only about purity, but about long-term consistency, reliable supply, and compatibility with existing processes.

This is why the industry is not suited to rough, extensive capacity expansion. Once a supplier enters a core supply chain through long-term qualification, it tends to gain stronger customer stickiness and better specification-based pricing power. What looks like a materials market is, in reality, a competition among process platforms, testing capability, product-form engineering, and collaborative application-development strength.

Key Company Strategies Are Diverging, and the Market Is Entering a New Stage of Coexistence among Scale Leaders, Specialists, and Platform Groups

The development path of key companies shows that the competitive landscape is rapidly differentiating. In 2025, Xinjiang Joinworld and Chinalco formed the first tier with high purity aluminum revenues of USD 179.72 million and USD 116.00 million respectively. Norsk Hydro, Nippon Light Metal, KM Aluminium, Sumitomo Chemical, and RUSAL made up the second tier, while Nantong TADE and Sakai aluminium occupied a more specialized third tier. This structure shows that the industry is no longer governed by a single form of purity competition; multiple competitive models are now coexisting.

Xinjiang Joinworld represents the path of a scale leader moving toward platform integration. Chinalco reflects the industrial amplification power of an integrated aluminum group expanding into high-purity materials. Nantong TADE is closer to a specialist ultra-high-purity electronic materials company extending into higher-value downstream forms. KM Aluminium is a representative case of a focused supplier deeply embedded in semiconductor and display sputtering-target feedstock chains. At the same time, Japanese players such as Sumitomo Chemical and Nippon Light Metal continue to maintain strong influence in premium 5N and 6N segments through their high-specification material-definition capability and long-term application know-how. Overall, future competition will increasingly revolve around process stability, product-form capability, customer qualification depth, vertical integration, and platform-level coordination.

Drivers, Constraints, and Direction Are Evolving Together, Pushing the Industry into a Value-First Competitive Cycle

The main growth drivers of ultra-high purity aluminum are becoming increasingly clear. First, continuous upgrading in semiconductors, displays, and precision electronic materials is raising upstream material standards. Second, deeper penetration of 5N-and-above material into high-value applications means that growth is increasingly driven by value upgrading rather than pure tonnage expansion. Third, stronger customer requirements for localization, delivery stability, and sustainable supply favor leading producers with robust manufacturing systems and long certification histories.

At the same time, the constraints remain equally clear. Refining routes are complex, yield pressure is high, and analytical requirements are strict, making rapid replication difficult for new entrants. Orders are often customized and project-based, so market expansion is constrained by downstream qualification cycles. As purity continues to rise, yield loss, process fluctuation, and equipment-utilization issues become more severe. For that reason, ultra-high purity aluminum is unlikely to become a price-war market. Instead, it is moving into a value-first competition cycle defined by technical capability, application integration, and industrial coordination.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Ultra-High Purity Aluminum market is segmented as below:

By Company

Xinjiang Joinworld Co., Ltd.

Aluminum Corporation of China Limited

Nantong TADE Electronic Material Technology Co., Ltd.

Norsk Hydro ASA

United Company RUSAL, International Public Joint-Stock Company

Sumitomo Chemical Co., Ltd.

Nippon Light Metal Company, Ltd.

Sakai aluminium Corporation

C-KOE Metals, L.P.

Marumae Co., Ltd.

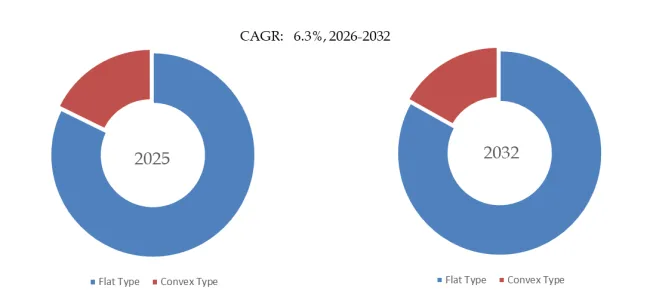

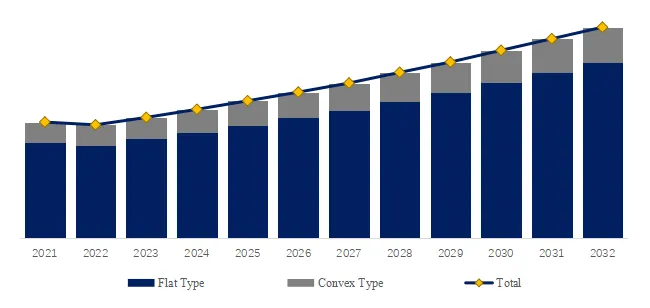

Segment by Type

5N Grade

6N and Above

Segment by Application

Semiconductor and FPD Materials

Capacitor Foil

Storage and Precision Electronic Materials

Others

Each chapter of the report provides detailed information for readers to further understand the Ultra-High Purity Aluminum market:

Chapter 1: Introduces the report scope of the Ultra-High Purity Aluminum report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Ultra-High Purity Aluminum manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Ultra-High Purity Aluminum market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Ultra-High Purity Aluminum in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Ultra-High Purity Aluminum in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Ultra-High Purity Aluminum competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Ultra-High Purity Aluminum comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Ultra-High Purity Aluminum market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Ultra-High Purity Aluminum Market Research Report 2026

Global Ultra-High Purity Aluminum Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Ultra-High Purity Aluminum Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Ultra High Purity Aluminum Ingots Market Research Report 2026

Global Electronic Grade Ultra-High-Purity Aluminum Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Electronic Grade Ultra-High-Purity Aluminum Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Electronic Grade Ultra-High-Purity Aluminum- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Electronic Grade Ultra-High-Purity Aluminum Market Research Report 2026

Global Ultra-high Purity Aluminum Sputtering Target Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Ultra-high Purity Aluminum Sputtering Target Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Ultra-high Purity Aluminum Sputtering Target Market Research Report 2026

Ultra-high Purity Aluminum Sputtering Target- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

5N Ultra-high Purity Aluminum Sputtering Targets- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global 5N Ultra-high Purity Aluminum Sputtering Targets Market Outlook, In‑Depth Analysis & Forecast to 2032

Global 5N Ultra-high Purity Aluminum Sputtering Targets Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global 5N Ultra-high Purity Aluminum Sputtering Targets Market Research Report 2026

Ultra-high Purity Aluminum Sputtering Target for FPD- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Ultra-high Purity Aluminum Sputtering Target for FPD Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Ultra-high Purity Aluminum Sputtering Target for FPD Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Ultra-high Purity Aluminum Sputtering Target for FPD Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp