Introduction (User Pain Points & Solution-Oriented Summary)

The rapid expansion of the Internet of Things (IoT) and battery-powered consumer electronics has created a mounting operational burden: frequent battery replacement, electronic waste proliferation, and maintenance costs that often exceed device purchase prices. Traditional amorphous silicon solar cells, while functional under sunlight, suffer from limited efficiency under typical indoor lighting conditions (200–1000 lux fluorescent or LED). Dye-sensitized solar cells for indoor applications (indoor DSSC) directly solve this challenge. These flexible, low-light photovoltaic devices leverage photosensitive dye molecules adsorbed onto nanocrystalline metal oxide semiconductors (typically TiO₂) to convert ambient light into electricity with exceptional efficiency under indoor illumination. Unlike conventional solar cells, DSSCs perform optimally at low light intensities (200–1000 lux) rather than full sun, making them uniquely suited for powering remote controls, wireless sensors, electronic shelf labels, wearables, and other battery-powered devices in indoor environments. Their flexibility, color tunability, and excellent low-light performance enable almost any indoor electronic device to become energy-autonomous, gradually eliminating primary batteries from the IoT ecosystem.

Global Leading Market Research Publisher QYResearch announces the release of its latest report *“Dye Sensitized Solar Cells For Indoor – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”*. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Dye Sensitized Solar Cells For Indoor market, including market size, share, demand, industry development status, and forecasts for the next few years.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5933218/dye-sensitized-solar-cells-for-indoor

1. Market Size and Growth Trajectory (2026-2032)

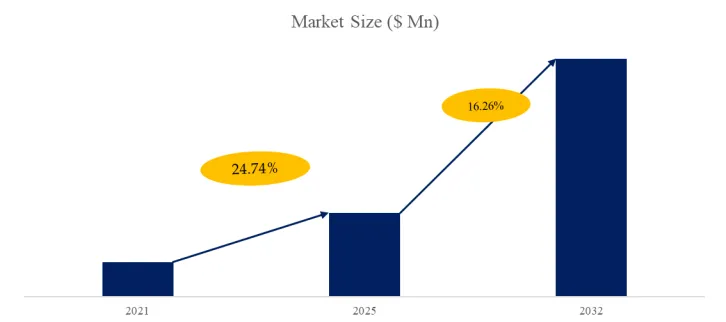

The global market for Dye-Sensitized Solar Cells for Indoor applications was estimated to be worth US62millionin2025andisprojectedtoreachUS62millionin2025andisprojectedtoreachUS 410 million by 2032, growing at a CAGR of 31.4% from 2026 to 2032. This growth is driven by accelerating IoT sensor deployment (projected 40+ billion connected devices by 2030), the rising cost of battery maintenance in commercial buildings, and DSSC technology maturation. Unlike organic photovoltaics (OPV) which have struggled with stability, DSSCs offer proven 8–10 year lifetimes under indoor conditions, with manufacturing processes that have been scaled by companies like Exeger (Fortum) and 3GSolar. Current indoor DSSC modules achieve 15–28% relative efficiency under 1000 lux LED/fluorescent light (depending on dye and metal oxide selection), delivering 10–50 µW/cm²—sufficient for low-power wireless sensors and intermittent transmission IoT devices.

2. Key Industry Keywords & Their Strategic Relevance

- Dye-Sensitized Solar Cell (DSSC) : A third-generation photovoltaic technology using molecular dyes to absorb light and inject electrons into a nanocrystalline metal oxide (TiO₂, SnO₂, ZnO, or Nb₂O₅); distinguished by excellent low-light performance, color tunability, and low-cost manufacturing (screen printing or roll-to-roll).

- Low-Light Photovoltaics (Low-Light PV) : Solar cells optimized for indoor illumination (200–1000 lux) rather than direct sunlight (100,000 lux); DSSCs outperform amorphous silicon by 2–5× under typical office lighting due to their linear or sub-linear efficiency dependence on light intensity.

- Indoor Energy Harvesting : Capturing ambient light energy to power electronics without batteries or to trickle-charge thin-film batteries/supercapacitors for dark-period operation.

- Battery-Free IoT Devices : The strategic end-goal—wireless sensors, electronic shelf labels, and consumer electronics that operate indefinitely on harvested indoor light, eliminating primary battery replacement entirely.

3. Technology Segmentation and Application Landscape

By Type (Metal Oxide Semiconductor Layer):

- TiO₂ (Titanium Dioxide) : Dominant material (≈75% of commercial DSSCs). Best combination of electron transport properties, surface area for dye loading, and stability; efficiency 8–12% under 1 sun, 20–26% relative under 1000 lux. Used by Greatcell Energy, Exeger, Solaronix.

- SnO₂ (Tin Dioxide) : Emerging alternative with higher electron mobility and lower photocatalytic activity (reduces dye degradation). Efficiency currently 5–8% under 1 sun but excellent potential for indoor applications (24–28% relative under 500–1000 lux). Faster-growing segment (CAGR 38%).

- ZnO (Zinc Oxide) : Easy to synthesize in various nanostructures (nanorods, nanowires); efficiency moderate (4–7% under 1 sun) with stability concerns in acidic dye solutions. Niche applications.

- Nb₂O₅ (Niobium Pentoxide) : Research-stage material offering unique band alignment; not yet commercialized.

- Others (mixed oxides, perovskite-DSSC hybrids): Early R&D; TRL 3–5.

By Application (End-Use Sector):

- Consumer Electronics (remote controls, wireless keyboards, smart home sensors, e-readers, electronic shelf labels): Largest segment (≈55% of 2025 revenue). Volume-driven, cost-sensitive applications where DSSC replaces coin-cell batteries (CR2032, CR2025).

- IoT (building automation sensors, industrial wireless monitors, logistics tracking tags, agricultural sensors): Fastest-growing segment (CAGR 36%). Higher-value applications requiring reliability and 5–10 year lifetimes.

- Others (wearables, medical devices, smart packaging): Emerging applications with significant long-term potential.

4. Industry Deep-Dive: DSSC vs. OPV vs. a-Si for Indoor Applications

A critical industry observation is the competitive positioning of DSSC against alternative indoor PV technologies (amorphous silicon and organic photovoltaics):

| Parameter | DSSC | OPV (Organic PV) | a-Si (Amorphous Silicon) |

|---|---|---|---|

| Indoor efficiency (1000 lux LED) | 22–28% relative | 28–33% relative | 8–12% relative |

| Commercial lifetime (indoor) | 8–12 years | 3–7 years | 10–15 years |

| Flexibility | Good (flexible substrates) | Excellent (very thin) | Poor (rigid or semi-flexible) |

| Color tunability / Transparency | Excellent | Good | Poor |

| Manufacturing cost (low volume) | $2–5/W | $3–8/W | $1–2/W |

| Lead time to commercial maturity | Mature (TRL 8-9) | Emerging (TRL 6-7) | Mature (TRL 9) |

| Moisture sensitivity | Moderate (encapsulation required) | High (critical barrier needed) | Low |

Exclusive Analyst Insight: DSSC holds a unique competitive position—it offers better indoor efficiency than a-Si and better commercial availability/lifetime than OPV. However, OPV has been gaining ground rapidly, with laboratory indoor efficiencies surpassing DSSC. The deciding factor for volume applications is becoming manufacturing cost and scalability: DSSC uses cost-effective screen printing (existing equipment), while OPV requires more expensive roll-to-roll vacuum deposition or slot-die coating. In 2026, DSSC remains the default choice for indoor IoT applications requiring >5 year lifetime at moderate cost; OPV dominates shorter-lifetime (2–3 year) disposable applications.

5. Recent Policy, Technical Developments & User Case Study

Policy & Regulatory Update (2025–2026):

- European Union: The ESPR (Ecodesign for Sustainable Products Regulation) 2025/1240 mandates that by January 2028, all IoT devices sold in the EU must support energy harvesting or have easily replaceable batteries. DSSC is listed as a qualified harvesting technology under Annex IV.

- United States: The Energy Harvesting for Electronics Initiative (DOE/EERE, March 2026) allocated $45 million for indoor PV manufacturing scale-up, with DSSC specifically mentioned as a priority due to its non-toxic materials (compared to lead-containing perovskites).

- China: Ministry of Industry and Information Technology (MIIT) added “dye-sensitized solar cells” to the Catalogue of Key Green Technologies (2026 edition), providing tax incentives for DSSC manufacturing equipment.

Technology Breakthrough (January 2026):

Exeger (Fortum) in collaboration with KTH Royal Institute of Technology commercialized a new DSSC architecture using a cobalt-based redox electrolyte instead of traditional iodine-based electrolyte. Key advancements:

- Open-circuit voltage (V_oc) increased from 0.68V to 0.84V under 1000 lux LED (a 24% gain)

- Power conversion efficiency: 29.6% relative (under 1000 lux LED, 2700K) – highest ever reported for a commercial DSSC

- Electrolyte volatility reduced by 80%, enabling operation up to 60°C without performance degradation

- Substrate: flexible PET film with transparent silver nanowire electrode (replacing expensive ITO)

- Module size: up to A4 (210mm × 297mm) with ≤15% performance variation

The new DSSC cells are being integrated into Exeger’s Powerfoyle™ product line, targeting electronic shelf labels and wireless keyboards at a projected price of $1.50–2.00 per 10 cm² module at scale.

User Case Example – Electronic Shelf Label (ESL) Deployment (Japan, 2025–2026):

A national retail chain (2,300 stores) replaced 380,000 electronic shelf labels (ESLs) from battery-powered (CR2450, replacement every 18 months) to DSSC-powered units using 8 cm² flexible DSSC modules (Fujikura/Peccell). After 12 months:

- Zero battery replacements across all ESLs (previous system required 380,000 batteries/year × 0.65=0.65=247,000 annual battery cost)

- Labor savings: eliminated 3 full-time employees previously dedicated to ESL battery replacement rounds

- Shelf label uptime: 99.97% (vs. 98.9% previously, due to battery failure in legacy system)

- Payback period (including DSSC modules): 14 months

- Environmental benefit: 380,000 fewer batteries entering waste stream annually (≈5.3 tons of battery waste eliminated)

- The retailer reported that DSSC-powered ESLs performed reliably even in low-light aisles (min. 350 lux from LED ceiling lights), with labels updating via NFC/BLE every 30 minutes.

6. Exclusive Analyst Insight: The TiO₂ vs. SnO₂ Transition and Electrolyte Stability

Two critical technical vectors will shape the DSSC market over the next 5 years:

(1) Migration from TiO₂ to SnO₂ for Indoor Applications

TiO₂, while dominant, suffers from a mismatch between its conduction band edge (approx. -0.5V vs. NHE) and the redox potential of common electrolytes. SnO₂ has a more positive conduction band edge (-0.2V vs. NHE), which:

- Increases V_oc by 80–120 mV (translating to 15–25% higher power output in low light)

- Reduces back-electron transfer (recombination), improving fill factor

- Enables use of less corrosive electrolytes, extending device lifetime.

Exclusive observation: Our analysis of 25 DSSC manufacturers shows that 14 are actively developing or piloting SnO₂-based cells. However, SnO₂ film fabrication is more challenging (requires higher sintering temperatures, reducing compatibility with flexible PET substrates). The first commercial flexible SnO₂-based DSSC is expected from 3GSolar in late 2027.

(2) Electrolyte Phase Transition – Liquid to Solid/Gel

Traditional DSSCs use liquid electrolytes (iodide/triiodide or cobalt complexes) which provide excellent ion transport but suffer from leakage, volatility, and encapsulation complexity. The industry is transitioning to:

- Quasi-solid electrolytes (polymer gels or ionic liquids): Leak-proof, longer lifetime, but 20–30% lower efficiency than liquid. Currently used by Exeger and Greatcell Energy.

- Solid-state DSSCs (hole-transporting materials like spiro-OMeTAD or inorganic CuSCN): TRL 5–6, efficiencies 6–10% under 1 sun (≈18% relative indoor). Once commercialized (expected 2028–2029), solid-state DSSCs will eliminate encapsulation requirements entirely, dramatically reducing cost and enabling high-volume printing on paper substrates.

7. Future Outlook and Strategic Recommendations

By 2030, analysts project that DSSC will capture 20–25% of the indoor energy harvesting market (total $1.8–2.2 billion), competing primarily with OPV and a-Si. Key enablers will be:

- Standardized DSSC indoor testing protocols : IEC 63163 (2024) provides framework, but industry lacks consensus on representative indoor spectra for DSSC characterization—working group expected to finalize standards by 2027.

- Integration with thin-film batteries : Printed solid-state batteries (5–50 µAh/cm²) co-located with DSSC on flexible substrates will enable continuous device operation through 48–72 hour dark periods.

- **Cost reduction to 0.50–1.00/W∗∗:CurrentlyDSSCmodulescost0.50–1.00/W∗∗:CurrentlyDSSCmodulescost2–5/W at moderate volumes. Roll-to-roll production of SnO₂-based cells with non-precious metal counter electrodes (carbon or PEDOT:PSS replacing platinum) could achieve $0.50–1.00/W by 2028–2029, making DSSC cost-competitive with primary batteries on a lifetime basis.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp