QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Vendor Management System (VMS) Software- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Vendor Management System (VMS) Software market, including market size, share, demand, industry development status, and forecasts for the next few years.

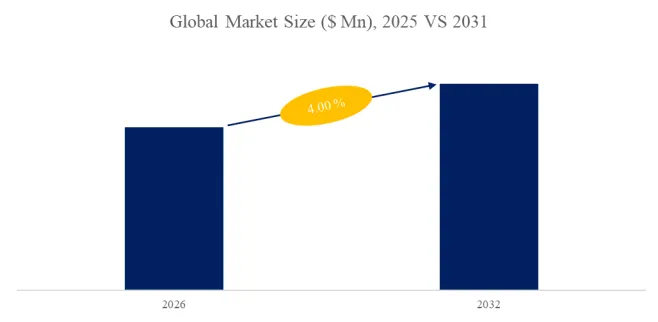

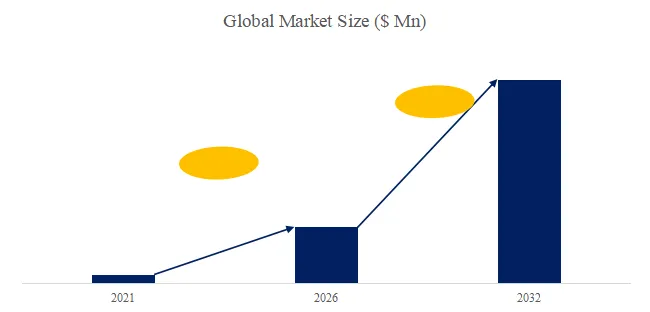

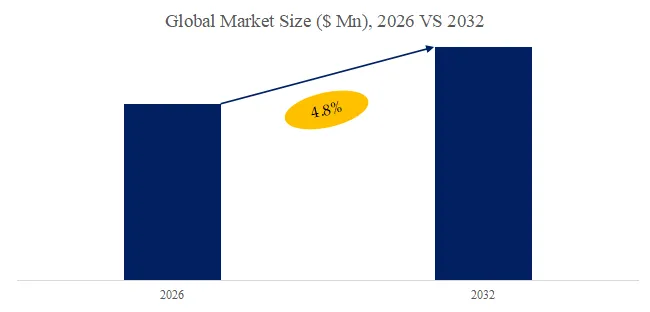

The global market for Vendor Management System (VMS) Software was estimated to be worth US$ 3005 million in 2025 and is projected to reach US$ 4806 million, growing at a CAGR of 6.7% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5649306/vendor-management-system–vms–software

Vendor Management System (VMS) Software Market Summary

Vendor Management System software is an enterprise software platform used to centrally manage external suppliers, service providers, contractors, contingent workers, professional consultants, and outsourced teams. It covers key processes such as vendor onboarding, qualification review, job or service requisitions, quotation and contracts, time and delivery confirmation, invoicing and payment, performance evaluation, compliance documentation, risk classification, renewal, and offboarding. Its core value is not simply “managing a supplier list,” but integrating third-party data scattered across procurement, finance, legal, information security, human resources, business units, and compliance teams into a trackable, auditable, and analysable management system. The mainstream product scope has expanded from traditional contingent workforce management to external workforce management, services procurement, and supplier risk and performance management. SAP Fieldglass positions itself as a cloud platform for managing external workforce and services procurement, while Workday VNDLY emphasises the full lifecycle of contingent workers from sourcing, engagement, management, invoicing, reporting, and offboarding.

Industry Background: External Suppliers Have Become a Core Variable in Enterprise Resilience

Global enterprises are entering a stage where external resources are deeply embedded in daily operations. Banking, insurance, consulting, healthcare, pharmaceuticals, software, semiconductors, manufacturing, energy, retail, logistics, construction, and engineering companies increasingly rely on third parties for technology development, professional services, equipment maintenance, contingent staffing, logistics delivery, project execution, cybersecurity, compliance consulting, and outsourced operations. In the past, procurement management mainly focused on price, delivery, and contracts. Today, supplier management is directly linked to business continuity, data security, regulatory compliance, labour compliance, environmental responsibility, delivery quality, and brand reputation. As supplier networks expand, service models become more complex, and cross-regional collaboration increases, spreadsheets, emails, and manual approvals can no longer support real-time visibility and end-to-end tracking. Vendor Management System software is therefore evolving from a procurement department tool into essential infrastructure for managing the enterprise’s external ecosystem.

Policy, Technology, and Demand Changes: Compliance, Artificial Intelligence, and Third-Party Risk Are Raising System Value

At the policy level, corporate responsibility for third-party management continues to expand. The European Union Corporate Sustainability Due Diligence Directive entered into force on 25 July 2024, requiring in-scope companies to identify and address adverse human rights and environmental impacts in their own operations and global value chains. The European Union network and information security framework also covers multiple critical sectors and emphasises cross-border coordination and supply chain security. The European Union Digital Operational Resilience Act has applied since 17 January 2025 and requires financial entities to strengthen information and communication technology third-party risk management.

At the technology level, cloud deployment, system interfaces, electronic contracts, automated approvals, identity and access management, supplier scoring, risk alerts, invoice matching, data analytics, and artificial intelligence are becoming core directions for product upgrades. Coupa has incorporated supplier risk detection, performance monitoring, and supplier diversity into its supplier management capabilities, while SAP Fieldglass Services Procurement highlights holistic management of external services such as consulting, marketing, maintenance, repair, and security, with artificial intelligence-generated statements of work, chatbots, and decision wizards.

At the demand level, enterprise customers are no longer satisfied with simply recording supplier information. They expect the system to answer more critical questions: which suppliers support mission-critical operations, which external workers access sensitive data, which service contracts have compliance gaps, which suppliers show declining delivery quality, and which regions face supply interruption risks. As a result, the value of Vendor Management System software is shifting from workflow automation to procurement transparency, proactive risk control, and strategic external resource management.

Market Opportunities: From Contingent Workforce Management to Enterprise-Wide Third-Party Ecosystem Governance

The market opportunity for Vendor Management System software mainly comes from three directions. First, external workforce and professional services procurement continue to grow. Enterprises need to manage contingent workers, freelancers, consultants, outsourced teams, project-based service providers, and services procurement contracts at the same time, while traditional human resources or procurement systems often cannot fully cover these “non-employee but operationally embedded” external resources. Second, third-party risk management is expanding from highly regulated sectors such as finance, healthcare, and energy into manufacturing, retail, technology, and engineering. Supplier onboarding, certificate validity, cybersecurity, labour compliance, environmental responsibility, and business continuity all require digital records and continuous monitoring. Third, artificial intelligence is increasing the decision-making value of this software category. Through supplier profiles, delivery scores, price benchmarks, risk labels, contract anomaly detection, and alternative supplier recommendations, the system can help enterprises move from passive supplier administration to proactive optimisation of external resource portfolios. The United States Securities and Exchange Commission’s cybersecurity disclosure rules have also raised requirements for cybersecurity risk management, governance, and material incident disclosure among public companies, bringing third-party service provider security risk further into the attention of boards and investors.

Risks: Data Quality, System Integration, and Organisational Coordination Determine Implementation Success

The Vendor Management System software market has a clear growth logic, but implementation is not simple. First, supplier data is usually scattered across procurement, finance, legal, information security, human resources, quality, and business departments. If master data is not unified, system deployment can easily result in duplicate suppliers, missing contract information, confused approval paths, and distorted risk scores. Second, the system often needs to integrate with enterprise resource planning systems, human capital management systems, procurement systems, finance systems, identity and access management systems, contract systems, and risk management platforms, making the project more complex than a single-point tool. Third, supplier management involves a redesign of authority and responsibility. Enterprises need to redefine onboarding standards, approval rights, service levels, performance indicators, risk categories, external worker access, and offboarding mechanisms. For software vendors, a lack of industry templates, compliance expertise, localisation services, and ecosystem integration capability can create delivery challenges in highly regulated or highly complex sectors such as finance, healthcare, energy, construction, and engineering.

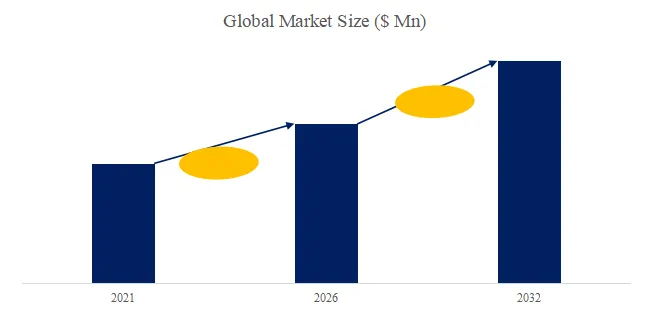

According to the new market research report “Global Vendor Management System (VMS) Software Market Report 2026-2032”, published by QYResearch, the global Vendor Management System (VMS) Software market size is projected to reach USD 4.73 billion by 2032, at a CAGR of 6.4% during the forecast period.

Figure00001. Global Vendor Management System (VMS) Software Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Vendor Management System (VMS) Software Market Report 2026-2032 (published in 2024). If you need the latest data, plaese contact QYResearch.

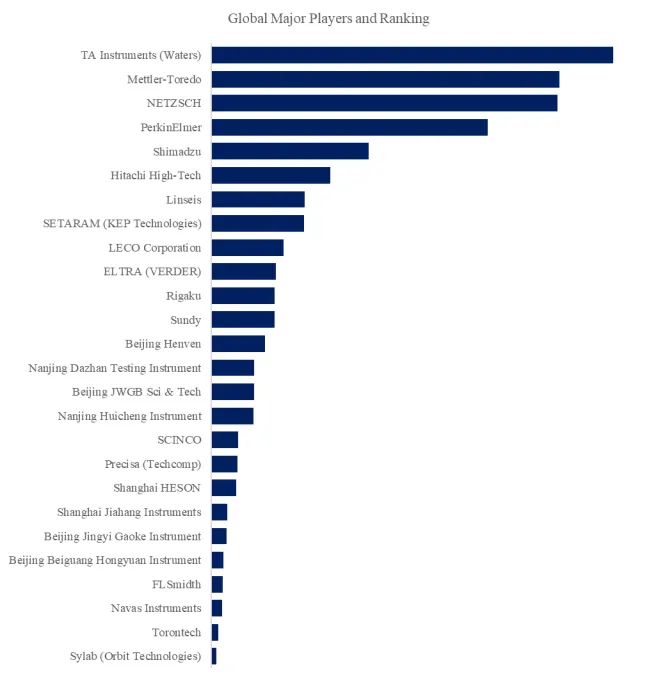

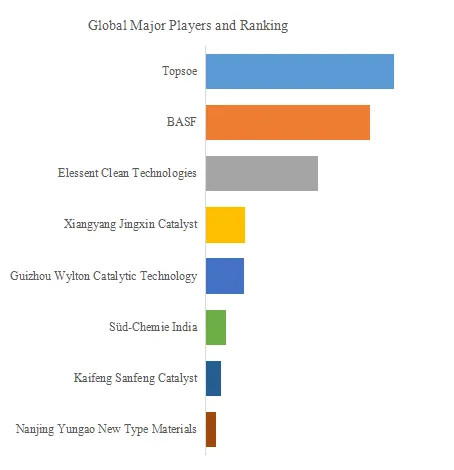

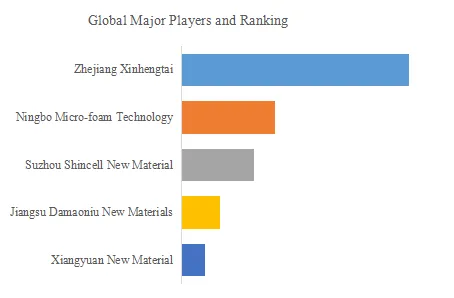

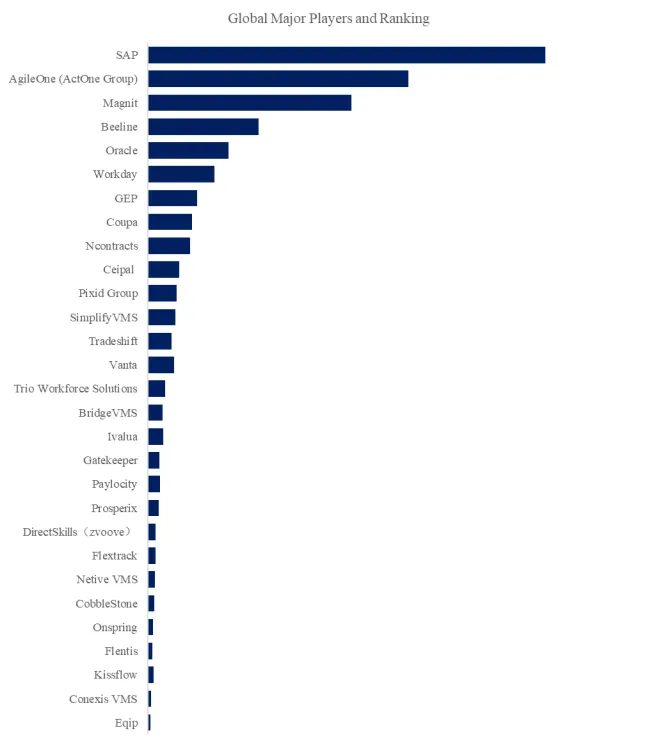

Figure00002. Global Vendor Management System (VMS) Software Top 29 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Vendor Management System (VMS) Software Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Vendor Management System (VMS) Software include SAP, AgileOne (ActOne Group), Magnit, Beeline, Oracle, Workday, GEP, Coupa, Ncontracts, Ceipal, etc. In 2025, the global top 10 players had a share approximately 63.0% in terms of revenue.

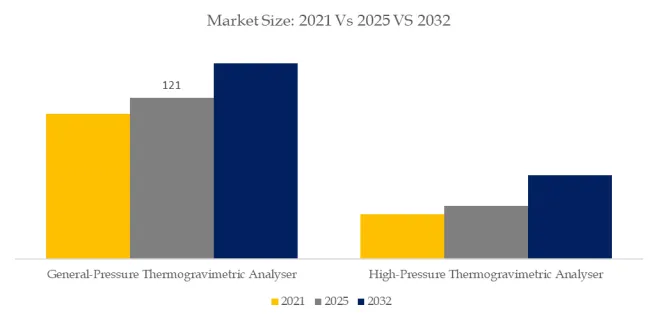

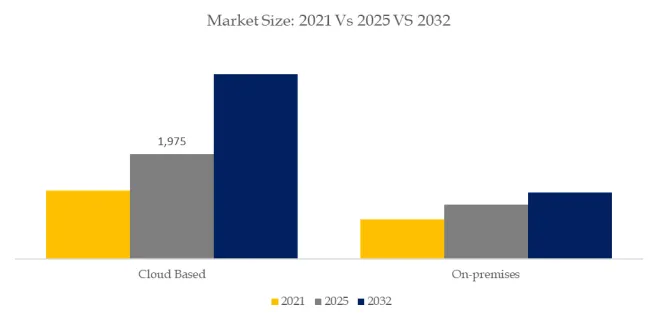

Figure00003. Vendor Management System (VMS) Software, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Vendor Management System (VMS) Software Market Report 2026-2032.

In terms of product type, currently Cloud Based is the largest segment, hold a share of 65.7%.

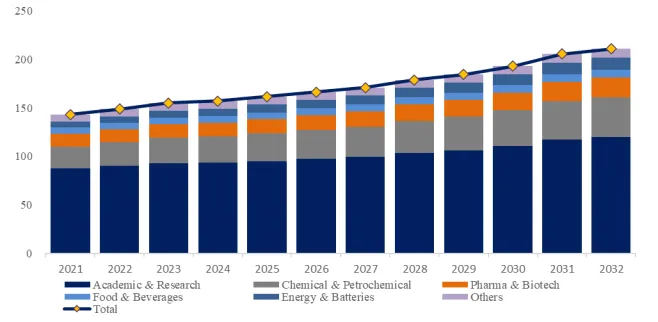

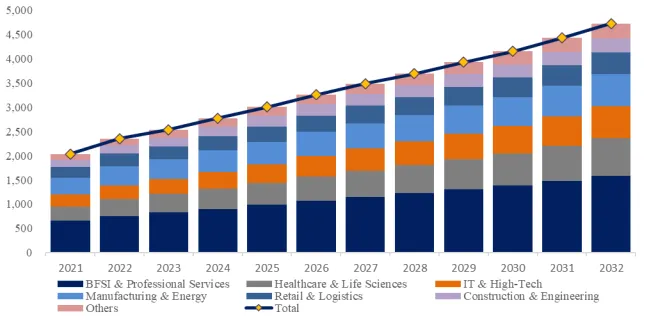

Figure00004. Vendor Management System (VMS) Software, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global Vendor Management System (VMS) Software Market Report 2026-2032.

In terms of product application, currently BFSI & Professional Services is the largest segment, hold a share of 32.9%.

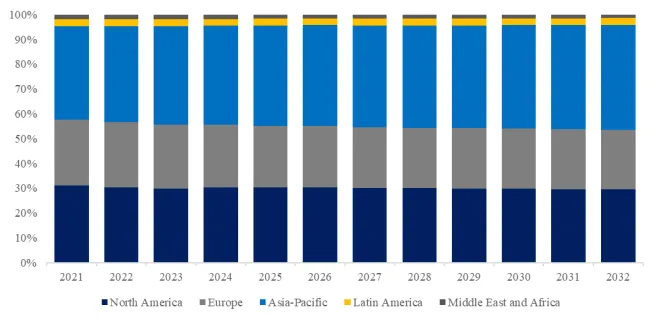

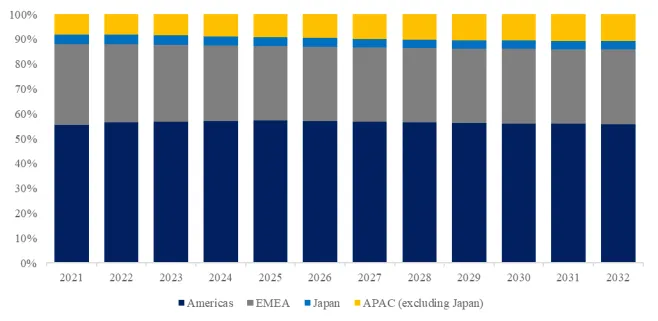

Figure00005. Vendor Management System (VMS) Software, Global Market Size, Split by Region

Based on or includes research from QYResearch: Global Vendor Management System (VMS) Software Market Report 2026-2032

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Vendor Management System (VMS) Software market is segmented as below:

By Company

SAP

AgileOne (ActOne Group)

Magnit

Beeline

Oracle

Workday

GEP

Coupa

Ncontracts

Ceipal

Pixid Group

SimplifyVMS

Tradeshift

Vanta

Trio Workforce Solutions

Eqip

Ivalua

Gatekeeper

Paylocity

Prosperix

DirectSkills(zvoove)

Flextrack

Netive VMS

CobbleStone

Onspring

Flentis

Kissflow

Conexis VMS

BridgeVMS

Segment by Type

Cloud Based

On-premises

Segment by Application

BFSI & Professional Services

Healthcare & Life Sciences

IT & High-Tech

Manufacturing & Energy

Retail & Logistics

Construction & Engineering

Others

Each chapter of the report provides detailed information for readers to further understand the Vendor Management System (VMS) Software market:

Chapter 1: Introduces the report scope of the Vendor Management System (VMS) Software report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Vendor Management System (VMS) Software manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Vendor Management System (VMS) Software market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Vendor Management System (VMS) Software in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Vendor Management System (VMS) Software in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Vendor Management System (VMS) Software competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Vendor Management System (VMS) Software comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Vendor Management System (VMS) Software market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Vendor Management System (VMS) Software Market Research Report 2026

Global Vendor Management System (VMS) Software Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Vendor Management System (VMS) Software Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global and Japan Vendor Management System (VMS) Software Market Report & Forecast 2025-2031

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp