QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Single-acting Spring Return Actuator- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Single-acting Spring Return Actuator market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for Single-acting Spring Return Actuator was estimated to be worth US$ 22.90 million in 2025 and is projected to reach US$ 33.75 million, growing at a CAGR of 5.7% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6114612/single-acting-spring-return-actuator

Single-acting Spring Return Actuator Market Summary

According to the latest report “Global Single-acting Spring Return Actuator Market Report 2025-2031″ by the QYResearch research team, the global Single-acting Spring Return Actuator market size is expected to reach US$0.0242 billion in 2031, with a compound annual growth rate (CAGR) of 5.7% in the next few years.

A single-acting spring-return actuator is a mechanical drive device utilized in industrial automation control systems, typically paired with valves, dampers, or other regulating mechanisms. Its core structure comprises a pneumatic or hydraulic cylinder, a piston, a spring, and a connecting shaft. When external fluid pressure (gas or liquid) is applied to the piston, the actuator generates force to drive the valve’s opening or actuate the mechanism; conversely, when the fluid pressure is released, the internal spring automatically returns to its original state, restoring the valve or mechanism to its initial position. Characterized by its simple structure, rapid response, high reliability, and ease of maintenance, this actuator is widely deployed across industries such as petrochemicals, energy, electric power, environmental protection, and water treatment to facilitate remote automatic valve control, emergency shutdown protection, and automated process regulation. Single-acting spring-return actuators can be designed in various specifications—tailored to specific thrust requirements, stroke lengths, and interface standards—to accommodate a diverse range of valve types, including ball valves, butterfly valves, and gate valves. By ensuring both system safety and operational precision, they serve as critical actuating components in modern industrial process control systems.

The overall market for single-acting spring-return actuators is exhibiting a trend of steady growth. As production equipment demands increasingly higher levels of reliability, rapid response capabilities, and safety protection, single-acting spring-return actuators—distinguished by their simple structure, low cost, ease of maintenance, and reliable return mechanisms—have emerged as critical actuating components in automated machinery, valve control systems, and fluid transport networks.

Concurrently, downstream industries—including mechanical manufacturing, petrochemicals, energy, and water treatment—are demonstrating a significant surge in demand for actuators capable of withstanding high pressures and temperatures, while ensuring long-term operational stability. Technological development trends are becoming increasingly diversified, encompassing advancements in high-performance spring materials, corrosion-resistant surface treatments, modular design, and integrated intelligent monitoring systems, all aimed at extending service life and enhancing system reliability. In terms of regional markets, North America and Europe tend to prioritize high-precision and high-reliability products, whereas the Asian market is primarily driven by the demand for cost-effective solutions.

Overall, driven by the continuous advancement of industrial automation and increasingly stringent requirements for energy efficiency and environmental protection, the market for single-acting spring-return actuators retains substantial room for steady growth and offers new business opportunities stemming from technological upgrades.

The development of single-acting spring-return actuators is primarily driven by the imperatives of industrial automation, energy transition, and safety and environmental protection requirements.

As industries such as petrochemicals, power generation, metallurgy, and water treatment raise their standards for automation and remote control capabilities, the application of actuators in valve regulation, emergency shut-off systems, and process control is becoming increasingly widespread, thereby fueling a growing demand for products characterized by high reliability and rapid response speeds.

Simultaneously, the rapid construction of new energy facilities, smart grids, and clean energy projects has positioned actuators as critical control components within these modern energy infrastructures, imposing higher demands regarding resistance to high temperatures, high pressures, and corrosion.

Furthermore, the tightening of industrial safety standards and environmental protection regulations has compelled enterprises to adopt automated valves equipped with spring-return functions—facilitating automatic emergency fail-safe returns and leak-prevention control—thereby driving both technological product upgrades and market expansion.

Finally, the integration of intelligent control systems, modular design principles, and remote monitoring capabilities continues to provide sustained momentum for expanding the scope of application and optimizing the performance of single-acting spring-return actuators.

This report profiles key players of Single-acting Spring Return Actuator such as Valen Tech、Cowan Dynamics、Covnavalves、Festo、Zhejiang Zhongzhi Valve、Kinetrol、SMC、Bray、Quifer Actuators、SHANGHAI CHUANHU VALVE、DEZURIK、SHANGHAI QUGONG VALVE、Aira、Juhang Automation、Master Flo、Emerson、Aox-actuator、MT Valves & Fittings.

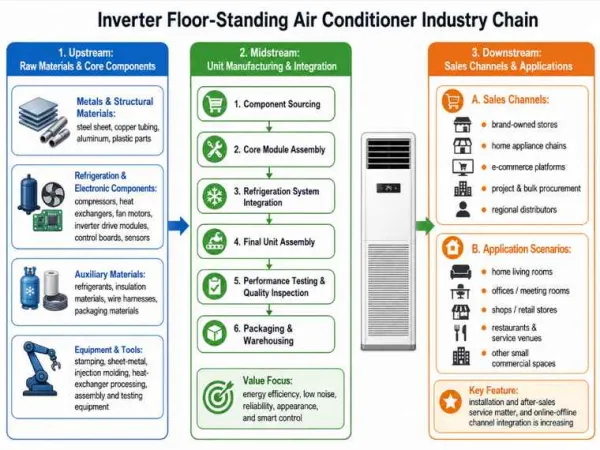

The industrial chain for single-acting spring-return actuators primarily consists of the following components:

I. Upstream of the Industrial Chain: Supply of Core Raw Materials and Components.

The upstream segment of the single-acting spring-return actuator industrial chain is primarily composed of metal material suppliers and precision component manufacturers, providing the fundamental material support necessary for the production and manufacturing of the actuators.

Regarding raw materials, carbon steel, stainless steel, and aluminum alloys serve as the foundational materials for core structural components such as the actuator cylinder body, piston, and end caps. The quality and performance of these materials directly determine the actuator’s mechanical strength and corrosion resistance. Among these, aluminum alloys are widely utilized for standard actuator cylinder bodies due to their lightweight nature and excellent machinability, whereas stainless steel is predominantly employed in corrosion-resistant models or products specifically designed for marine environments.

In terms of core components, alloy spring steel is the critical element enabling the actuator’s “spring-return” function. The material grade, heat treatment process, and dimensional precision of the spring directly impact the actuator’s return torque characteristics and operational lifespan. High-end actuator products typically incorporate customized spring assemblies that have undergone rigorous fatigue testing, ensuring that stable elastic performance is maintained even after millions of operational cycles.

Sealing assemblies and piston assemblies also reside within the upstream segment of the industrial chain. Rubber seals (such as those made from nitrile rubber or fluororubber) feature characteristics such as high-temperature resistance, corrosion resistance, and low friction, thereby ensuring that the actuator maintains excellent sealing integrity across a wide temperature range—typically from -40°C to +150°C.

Furthermore, the upstream segment encompasses the supply of standard parts, including bearings, fasteners, and positioner interfaces. The quality consistency of these components exerts a significant influence on the actuator’s assembly precision and long-term operational reliability.

II. Midstream of the Industrial Chain: Manufacturing Integration and Brand Manufacturers.

The midstream segment of the industrial chain constitutes the core stage of single-acting spring-return actuator manufacturing, encompassing a complete value chain ranging from precision machining, assembly, and testing to brand-based sales.

At the manufacturing level, the production of actuators involves a multi-step process that includes the extrusion molding of aluminum alloy cylinder bodies; hard anodizing of internal bores (creating an anodic oxide layer thickness exceeding 30μm); precision machining of gears and racks; heat treatment and pre-compression of springs; and the selection and assembly of sealing components. Mainstream manufacturers typically adopt a modular design philosophy, allowing spring assemblies to be added or removed on-site without the need for tools (commonly in configurations of 2 to 6 springs), thereby offering the flexibility to match the specific torque requirements of various valves.

Branded manufacturers constitute the core entities within the midstream segment of the industry chain. Key players in the global market include international giants—many boasting a century of industrial heritage—and rapidly emerging domestic Chinese enterprises. Companies at the international level hold dominant positions in the high-end market and in large-scale engineering projects. Leveraging their deep technical expertise, comprehensive global service networks, and regulatory barriers such as ATEX/IECEx explosion-proof certifications and SIL functional safety certifications, these firms maintain a competitive edge in high-end application sectors such as petrochemicals and nuclear power.

Chinese enterprises are experiencing rapid growth. Beyond catering to the immense domestic demand for industrial automation upgrades, several leading firms have begun to penetrate international markets, competing for market share by capitalizing on their cost-effectiveness and rapid-response capabilities.

In terms of midstream sales models, actuator manufacturers typically employ a hybrid approach combining direct sales with distribution channels. For large-scale engineering projects and OEM clients, customized solutions are often delivered through direct sales channels; conversely, the fragmented maintenance and repair market is typically served through a network of regional distributors.

III. Downstream of the Industry Chain: Integrated Applications and End-User Industries

The downstream segment of the industry chain is primarily composed of system integrators and end-users, representing the final stage where the value of actuator products is realized.

The core downstream clientele consists of control valve manufacturers and automation system integrators. These entities mechanically assemble and electrically commission single-acting, spring-return actuators in conjunction with valve bodies—such as ball valves, butterfly valves, and plug valves—to create complete pneumatic valve assemblies, which are then sold to end-users across various industries.

The scope of end-user applications is extremely broad, encompassing sectors such as petrochemicals, energy and power, metallurgy, water treatment, pharmaceuticals, and food and beverages. Among these, the petrochemical sector currently represents the largest downstream market; actuators are extensively deployed in applications such as feedstock shut-off valves within refinery catalytic cracking units, tail gas discharge valves in sulfuric acid production lines, and emergency shut-off valves on unloading arms at LNG receiving terminals. Single-acting actuators—distinguished by their inherent “fail-safe” characteristic (automatically reverting to a safe position upon loss of air supply, whether “fail-open” or “fail-close”)—are the preferred choice in scenarios requiring safety interlocks or emergency shut-down capabilities.

The energy and power sector constitutes another significant area of application. In nuclear power plants, this type of actuator is employed to control main steam isolation valves, requiring high seismic resistance ratings and radiation-resistant properties. In thermal power plants, they are utilized for high-pressure bypass pressure-reducing valves on steam turbines, thereby ensuring the safe and stable operation of the generating units.

In the field of water treatment, actuators are applied to brine discharge valves in seawater desalination facilities and knife gate valves in municipal wastewater treatment plants; their corrosion-resistant design and reliable spring-return functionality ensure stable performance in environments involving highly corrosive media or fluids containing solid particulates. Furthermore, actuators play a pivotal role in the metallurgy, pharmaceutical, and rail transit sectors.

IV. Horizontal Support Systems: Standards, Certifications, and Services

A horizontal support system spanning the entire industrial chain serves as the bedrock for the healthy functioning of the industry. International standards—such as ISO 5211 (mounting interface standard) and NAMUR (solenoid valve/positioner interface standard)—ensure the interchangeability and interoperability of actuators and valves from different brands. Regarding safety certifications, ATEX/IECEx explosion-proof certification and SIL functional safety certification constitute high barriers to market entry, representing mandatory requirements—particularly in sectors such as petrochemicals and natural gas.

With the advancement of Industry 4.0 and the rise of smart factories, downstream customers are placing increasingly high demands on the digital capabilities of actuators. There is a growing demand for “smart actuators” that support industrial fieldbus communication protocols—such as PROFIBUS and Modbus—and feature remote diagnostics and self-tuning parameter capabilities. This trend is compelling mid-stream manufacturers to increase their R&D investment in embedded systems and IoT technologies, thereby driving the industrial chain toward an upgrade into higher value-added segments.

The competitive landscape for single-acting spring-return actuators is characterized by a pattern of “fragmentation at the lower end, concentration at the higher end.”

From a market segmentation perspective, domestic low-to-mid-range products compete primarily on the basis of price advantages and localized services. These products mainly cater to the automated valve requirements of small-to-medium-sized factories and regional engineering projects; this segment features relatively low technical barriers and intense competition. Conversely, the mid-to-high-end market is dominated by internationally renowned brands and large-scale domestic enterprises. These manufacturers possess mature pneumatic and hydraulic design technologies, utilize highly reliable materials, and demonstrate precision manufacturing capabilities; moreover, they provide comprehensive system integration and after-sales services, primarily serving demanding sectors such as petrochemicals, electric power, metallurgy, and new energy. Overall, the market landscape is characterized by technology-leading enterprises dominating high-end application segments—where branding and service constitute core competencies—while price-sensitive markets are subject to fragmented competition among numerous small and medium-sized manufacturers. Looking ahead, driven by advancements in intelligent control, corrosion-resistant materials, and remote monitoring capabilities, high-performance products will increasingly establish technological barriers, thereby fostering a gradual rise in market concentration.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Single-acting Spring Return Actuator market is segmented as below:

By Company

Valen Tech

Cowan Dynamics

Covnavalves

Festo

Zhongzhi

Kinetrol

SMC

Bray

Quifer Actuators

CHUANHU

DEZURIK

SHANGHAI QUGONG VALVE

Aira

Juhang Automation

Master Flo

Emerson

Aox-actuator

MT Valves & Fittings

Segment by Type

Single Spring Configuration

Multiple Spring Configuration

Segment by Application

Petrochemicals

Energy

Metallurgy

Others

Each chapter of the report provides detailed information for readers to further understand the Single-acting Spring Return Actuator market:

Chapter 1: Introduces the report scope of the Single-acting Spring Return Actuator report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Single-acting Spring Return Actuator manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Single-acting Spring Return Actuator market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Single-acting Spring Return Actuator in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Single-acting Spring Return Actuator in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Single-acting Spring Return Actuator competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Single-acting Spring Return Actuator comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Single-acting Spring Return Actuator market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Single-acting Spring Return Actuator Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Single-acting Spring Return Actuator Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Single-acting Spring Return Actuator Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp