QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Interlayer Films for Automotive Laminated Glass- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Interlayer Films for Automotive Laminated Glass market, including market size, share, demand, industry development status, and forecasts for the next few years.

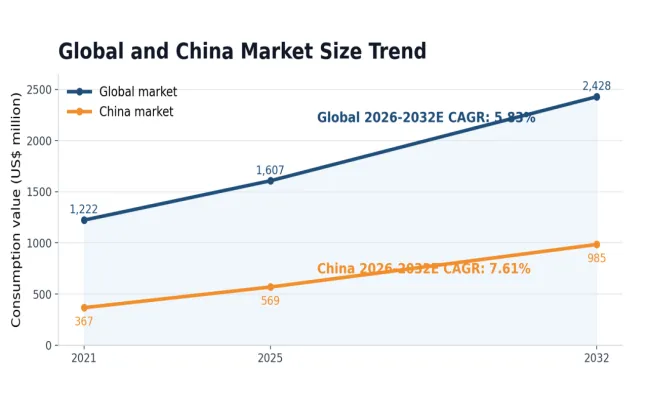

The global market for Interlayer Films for Automotive Laminated Glass was estimated to be worth US$ 1606 million in 2025 and is projected to reach US$ 2428 million, growing at a CAGR of 5.8% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6262787/interlayer-films-for-automotive-laminated-glass

Automotive laminated glass interlayers are core materials in automotive safety glass. They are placed between two or more glass sheets and laminated through pre-pressing, de-airing, and high-temperature/high-pressure autoclaving to form a stable composite structure. Their baseline value lies in fragment retention, penetration resistance, and optical transparency control. As smart cabins, HUD, NVH comfort, and thermal management requirements become more important, interlayers are moving from conventional safety materials toward higher-value functional materials.

According to the latest research, the global market for interlayer films for automotive laminated glass was approximately US$1.607 billion in 2025 and is expected to reach approximately US$2.428 billion by 2032, representing a 2026-2032 CAGR of about 5.83%. The China market is expected to grow from approximately US$569 million in 2025 to approximately US$985 million in 2032, outpacing the global average. Market growth is being driven by steady windshield demand, rising penetration of HUD wedge films, acoustic and heat-insulating film upgrades, panoramic roof glass, and laminated side-window adoption.

Source: QYResearch Nanning Research Center

1.1 Market overview: stable growth driven by safety demand and functional upgrading

Demand for automotive laminated glass interlayers is first determined by regulation, safety requirements, and vehicle glazing configurations. The front windshield remains a resilient base application with high penetration, but future value growth increasingly depends on higher-spec vehicle platforms, smart-cabin features, and functional film adoption. In commercial terms, growth reflects not only vehicle-market recovery, but also larger laminated-glass area per vehicle, higher unit value of functional films, and regional supply-chain reconfiguration.

From a business perspective, this is an automotive-material qualification market. Customers are not simply buying film thickness or volume; they are buying stable optical performance, batch consistency, reliable adhesion, low haze, weatherability, processing compatibility, and the ability to validate jointly with glass processors and OEM platforms. New nominal capacity that fails to pass glass-plant lamination validation, OEM program nomination, and vehicle SOP ramp-up cannot be directly converted into automotive-grade revenue.

On the cost side, the industry is exposed to volatility in PVB resin, PVA, butyraldehyde, plasticizers, functional additives, energy, and logistics. Standard films have weaker cost pass-through than functional films, so margin upside is more likely to concentrate in HUD wedge films, acoustic films, heat-insulating films, and multifunctional composite interlayers.

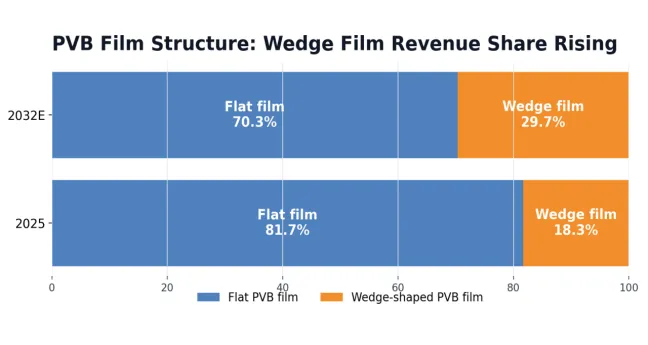

1.2 Product structure: PVB remains the mainstream, while wedge-shaped and functional films raise value density

By material system, PVB film remains the mainstream automotive laminated glass interlayer. SGP/ionoplast interlayers offer higher stiffness and strength and are relevant for selected high-strength, large-area roof, security, or specialty glazing projects. However, before 2032, cost, optical requirements, processing compatibility, and automotive qualification barriers mean SGP should be viewed as a premium or project-specific material rather than a large-scale substitute for PVB.

Within PVB, the market is becoming more segmented. By structure, flat film still carries the largest demand base, while wedge-shaped PVB film is growing faster, mainly serving HUD and AR-HUD windshields. The report estimates that wedge-shaped PVB film’s share of PVB-film revenue will increase from about 18.3% in 2025 to about 29.7% in 2032, reflecting HUD’s higher requirements for ghost-image control, wedge-angle consistency, and optical-distortion management.

Source: QYResearch Nanning Research Center

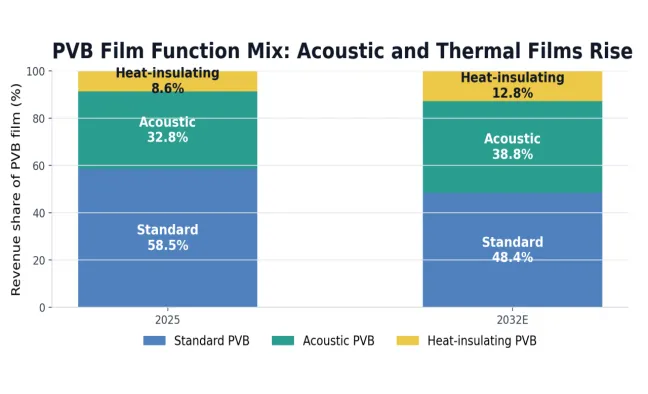

By function, standard PVB film remains the largest category, but acoustic and heat-insulating films are growing faster. Acoustic films benefit from NEV and premium-vehicle requirements for cabin quietness, while heat-insulating films are supported by panoramic roofs, fixed glass roofs, solar-radiation control, and cabin thermal comfort. By 2032, standard PVB film’s revenue share is expected to decline to about 48.4%, while acoustic film rises to about 38.8% and heat-insulating film to about 12.8%.

Source: QYResearch Nanning Research Center

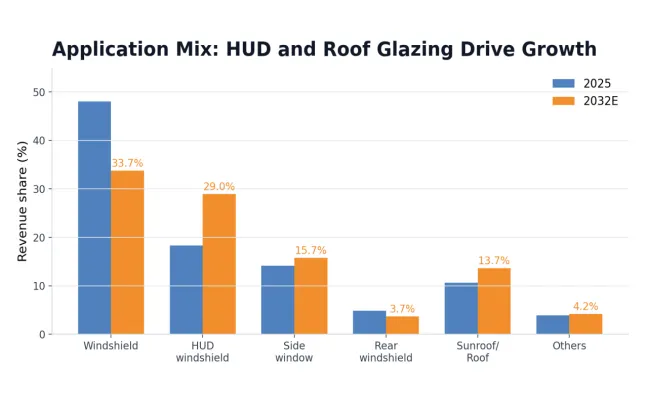

1.3 Applications: windshields remain the scale base; HUD, side windows and roof glazing provide growth

The windshield remains the core application scenario for interlayer films in automotive laminated glass, with regulatory requirements and safety attributes ensuring resilient demand. However, in terms of incremental growth, the market is expanding from traditional windshields to HUD windshields, acoustic side windows, panoramic sunroofs/roofs, and high-specification replacement glass.

The value of HUDs comes from the optical correction capabilities of the wedge-shaped interlayer film, especially in controlling ghosting, field of view, and projection clarity. With the increasing penetration of W-HUDs and AR-HUDs in new energy vehicles and mid-to-high-end models, the HUD interlayer film has become a crucial factor driving up average prices.

The lamination process for side windows, rear windshields, and sunroofs/roofs is more differentiated. Side windows are primarily driven by acoustics, frameless doors, security and anti-theft features, and high-end configurations; sunroofs/roofs are influenced by the need for large-area glass, heat insulation, and structural safety. However, these scenarios still need to consider competition from tempered glass, coated glass, Low-E, sunshades, and dimming glass solutions alongside laminated solutions.

Source: QYResearch Nanning Research Center

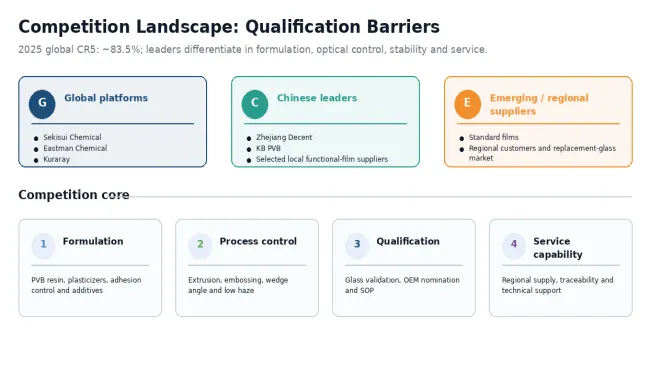

1.4 Competitive landscape: high concentration persists; functional films and automotive qualification define tiers

The global automotive laminated glass interlayer market remains highly concentrated. The report indicates that the global CR5 reached approximately 83.5% in 2025, with leading suppliers including Sekisui Chemical, Eastman Chemical, Kuraray, Zhejiang Decent New Material, and KB PVB. Global leaders retain advantages in PVB formulation systems, optical control, batch stability, automotive customer qualification, cross-regional supply, and functional-film portfolios.

Chinese suppliers are extending from standard PVB films into acoustic, heat-insulating, and selected wedge-shaped films. Their growth is supported by domestic automotive glass processing capacity, China’s NEV output, OEM localization of procurement, and local material suppliers’ investment in functional-film capacity. However, standard-film volume growth should not be directly interpreted as a breakthrough in premium OEM programs; wedge-shaped, acoustic, and heat-insulating films still require lengthy customer validation, program nomination, and SOP ramp-up.

Future competition is therefore likely to become more tiered. Standard films and parts of the replacement-glass market will remain more price-competitive, while premium HUD, acoustic, heat-insulating, and multifunctional composite films will compete on formulation, process control, optical performance, batch consistency, and global customer service.

Source: QYResearch Nanning Research Center

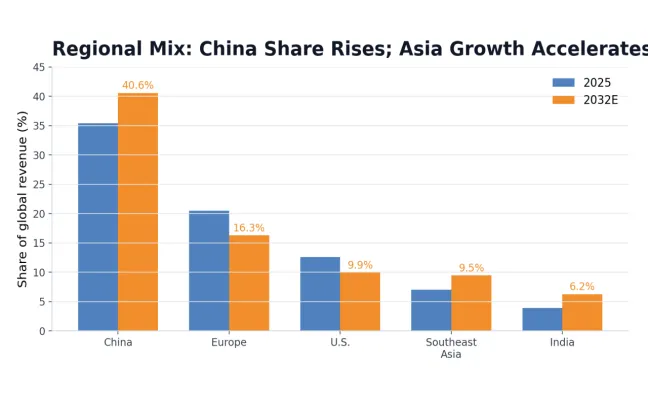

1.5 Regional landscape: China is the largest incremental market, while Asia’s supply-chain weight rises

By consumption value, China is the most important incremental market. The report estimates that China’s share of global revenue will rise from about 35.4% in 2025 to about 40.6% in 2032. This reflects not only China’s vehicle output and NEV scale, but also domestic automotive glass processing capability, HUD windshields, panoramic roofs, acoustic side windows, and the improvement of local functional-film supply.

Europe, North America, and Japan remain important markets for high-specification automotive glass and functional-film validation, with demand placing greater emphasis on quality consistency, regulatory compliance, long-term supply, and premium-vehicle applications. Southeast Asia and India offer growth elasticity from automotive manufacturing relocation, regionalized capacity deployment, and local glass-processing upgrades, although premium functional-film adoption will still depend on vehicle platforms, supplier qualification, and consumer-upgrade pace.

Source: QYResearch Nanning Research Center

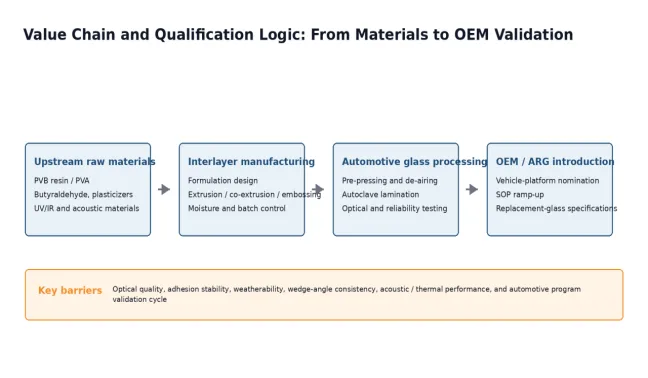

1.6 Value chain and manufacturing: the core barrier is the integration of materials, process control and customer introduction

The upstream chain for automotive laminated glass interlayers includes PVB resin, PVA, butyraldehyde, plasticizers, adhesion-control additives, UV/IR absorbers, acoustic functional-layer materials, pigments/masterbatch, and SGP-related ionoplast resins. Midstream suppliers must use formulation design, extrusion, embossing, multilayer co-extrusion, wedge-thickness control, moisture control, and stable packaging/logistics to meet automotive glass lamination requirements.

Direct downstream customers are mainly automotive glass suppliers such as Fuyao, AGC, Saint-Gobain Sekurit, NSG/Pilkington, Vitro, Xinyi, KCC Glass, and AGP. End demand comes from vehicle OEMs, the replacement-glass market, commercial vehicles, and specialty safety-glass projects. Because interlayer performance is ultimately realized after glass lamination, suppliers must work closely with glass processors, OEMs, and program platforms.

Key manufacturing control points include transparency, haze, adhesion strength, moisture content, thermal shrinkage, surface roughness, acoustic-layer stability, infrared blocking, wedge-angle consistency, and optical distortion. Bubbles, yellowing, shrinkage, adhesion failure, or HUD ghosting may lead to returns, claims, or supplier replacement.

Source: QYResearch Nanning Research Center

1.7 Opportunities and challenges: value growth is clear, but commercialization timing requires disciplined judgment

Growth opportunities are concentrated in HUD/AR-HUD, acoustic laminated glass, heat-insulating roof glass, panoramic roofs, low-carbon PVB, and high-specification replacement glass. For material suppliers, increasing the share of functional films, entering leading automotive glass supply chains, and securing OEM platform programs are critical to improving product mix and earnings quality.

Constraints fall into three categories. First, vehicle production and configuration timing: if HUD, laminated side-window, or glass-roof penetration is slower than expected, functional-film revenue growth may decelerate. Second, technology and validation cycles: wedge-shaped, acoustic, and heat-insulating films require long program validation, so new capacity cannot be equated directly with effective automotive-grade supply. Third, alternative-route competition: tempered glass, coated glass, Low-E glass, switchable glazing, and sunshade systems still have cost and process maturity advantages in some non-windshield applications.

Overall, the automotive laminated glass interlayer market is expected to maintain steady expansion. The industry focus is shifting from standard-film scale competition to competition around functional films, project qualification, regional service, and supply-chain security. For supply-chain customers, supplier selection should not rely only on price and capacity; automotive qualification records, batch consistency, functional-film capability, and integration with glass-processing steps are increasingly important.

By 2032, PVB will remain the mainstream material for automotive laminated glass interlayers, but its product content will be meaningfully upgraded. Front windshields will provide a stable demand base, while HUD wedge films, acoustic films, heat-insulating films, and laminated roof/side-window applications contribute incremental value. China and broader Asia will continue to gain weight. The key industry differentiator will shift from who can supply film to who can reliably supply functional, automotive-grade, and verifiable materials that meet vehicle-program requirements.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Interlayer Films for Automotive Laminated Glass market is segmented as below:

By Company

Sekisui Chemical

Eastman Chemical

Kuraray

Zhejiang Decent New Material

KB PVB

Huakai Plastic (Chongqing) Co., Ltd

Chang Chun Group

Anhui Wanwei

Zhejiang Duoli

Jiangsu Aotianli New Material

Jiangsu Jingdun New Material

Taizhou Infini

Suzhou Tolyy Optoelectronics Co., Ltd

Sichuan EM Technology

Suzhou Dongfu Electronic Technology

Jiangxi Huatesheng New Material

Segment by Type

Standard Interlayer Film

Sound Insulation Interlayer Film

Heat Insulation Interlayer Film

Segment by Application

Front Windshield

HUD

Side Window

Rear Windshield

Sunroof

Others

Each chapter of the report provides detailed information for readers to further understand the Interlayer Films for Automotive Laminated Glass market:

Chapter 1: Introduces the report scope of the Interlayer Films for Automotive Laminated Glass report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Interlayer Films for Automotive Laminated Glass manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Interlayer Films for Automotive Laminated Glass market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Interlayer Films for Automotive Laminated Glass in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Interlayer Films for Automotive Laminated Glass in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Interlayer Films for Automotive Laminated Glass competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Interlayer Films for Automotive Laminated Glass comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Interlayer Films for Automotive Laminated Glass market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Interlayer Films for Automotive Laminated Glass Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Interlayer Films for Automotive Laminated Glass Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Interlayer Films for Automotive Laminated Glass Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp