Introduction: Addressing Industry Pain Points

Fleet operators, marine engineers, and industrial facility managers face a persistent operational challenge: diesel engines (marine propulsion, mining haul trucks, construction equipment, backup generators) degrade gradually – fuel consumption increases 8-15% over 2-3 years, exhaust emissions rise, and unplanned breakdowns cause costly downtime (marine vessel: 10,000−50,000/day;mininghaultruck:10,000−50,000/day;mininghaultruck:5,000-15,000/hour). Traditional manual monitoring (periodic oil analysis, visual inspections, operator logs) cannot detect developing faults (injector coking, turbocharger fouling, cylinder imbalance) until performance has already deteriorated significantly. The solution lies in advanced diesel engine monitoring systems – integrated sensor networks with real-time data analytics, predictive algorithms, and automated alerting for key parameters: exhaust gas temperature (EGT), cylinder pressure, fuel injection timing, turbo speed, and NOx/particulate emissions. Global Leading Market Research Publisher QYResearch announces the release of its latest report “Diesel Engine Monitoring System – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Diesel Engine Monitoring System market, including market size, share, demand, industry development status, and forecasts for the next few years.

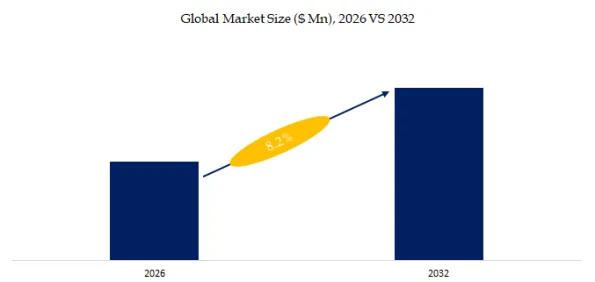

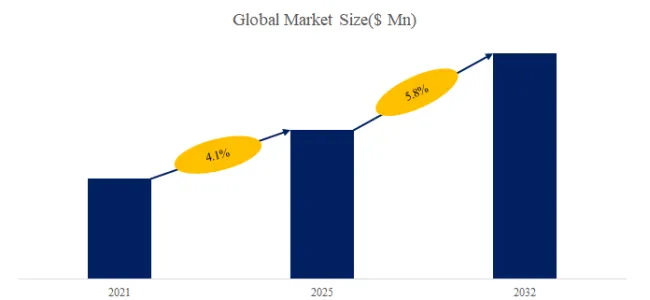

The global market for Diesel Engine Monitoring System was estimated to be worth US475millionin2025andisprojectedtoreachUS475millionin2025andisprojectedtoreachUS 789 million by 2032, growing at a CAGR of 7.5% from 2026 to 2032.

A Diesel Engine Monitoring System is an advanced technology used to monitor and analyze the performance of diesel engines in various applications such as vehicles, industrial machinery, and power generators. This system uses sensors and intelligent software to collect real-time data about different engine parameters and conditions.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/5932420/diesel-engine-monitoring-system

Market Segmentation by Component Type & Application

By Component Type – System Architecture Share Analysis

- Integrated System (Hardware + Software): Largest segment with 52% market share, fastest-growing at 8.1% CAGR. Turnkey solutions including sensors (pressure, temperature, knock, vibration), data acquisition modules (CAN bus, Ethernet), and cloud analytics dashboard. Preferred by commercial marine and mining fleet operators for “plug-and-play” deployment.

- Software System (Standalone Analytics): 28% market share, cloud-based or on-premises platforms that integrate with existing engine ECUs (Electronic Control Units) and plant SCADA systems. Lower upfront cost but requires compatible hardware.

- Hardware System (Sensors + DAQ only): 20% market share, component-level monitoring for retrofits and specialized applications (e.g., cylinder pressure sensors for research engines).

By Application – End-User Demand Drivers

- Marine (Commercial Vessels, Ferries, Offshore Support, Naval): Largest segment with 48% market share, fastest-growing at 8.5% CAGR. IMO Tier III (NOx limits) and EU Stage V (particulate) regulations require continuous emissions monitoring. Key parameters: EGT (per cylinder), turbo speed, scavenge air pressure, fuel rack position.

- Mining (Haul Trucks, Loaders, Excavators): 22% market share, remote mine sites (Australia, Chile, Canada, South Africa) requiring predictive maintenance to minimize haul cycle disruption. Typical fleet: 50-200 diesel engines per mine.

- Construction (Excavators, Bulldozers, Cranes, Generators): 18% market share, non-road mobile machinery (NRMM) emission standards tightening (EU Stage V, US EPA Tier 4 final).

- Others (Rail, Power Generation, Agriculture, Stationary Engines): 12% market share.

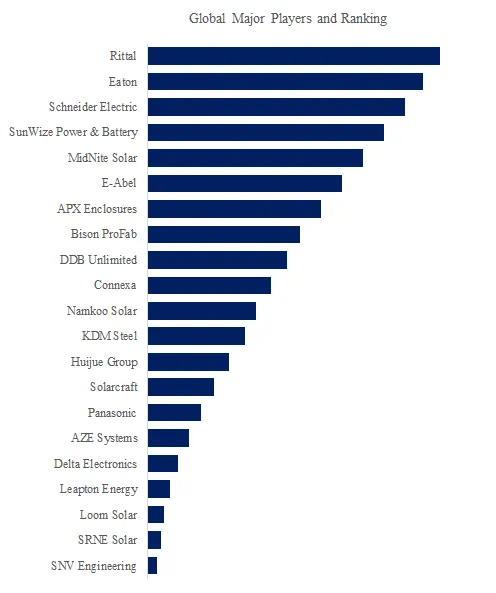

Competitive Landscape: 18+ Global Players

The market includes marine automation specialists, engine OEMs, and industrial analytics providers. Leading players identified in QYResearch’s analysis include:

Wärtsilä (Finland) – Global leader with 20% revenue share. Integrated monitoring for marine engines (2-stroke and 4-stroke), UNIC software platform.

ABB (Switzerland) – 16% share, marine and industrial monitoring (Ability™ Condition Monitoring).

MAN Energy Solutions (Germany) – 14% share, engine OEM with proprietary monitoring (MAN CEON).

Kongsberg Maritime (Norway) – 10% share, marine integrated systems (K-Chief, K-Engine).

Heinzmann (Germany) – 8% share, engine control and monitoring for gensets.

Chris Marine (Sweden) – 6% share, specialized in cylinder pressure monitoring.

Technoton (Belarus) – 5% share, fuel consumption monitoring.

Böning Automationstechnologie (Germany) – 4% share.

Poseidon Systems (US) – 3% share, oil debris and particle monitoring.

Other notable players: Icon Research, Phormula, Veethree Group, Advanced Marine Solutions, MRS Electronic, Techno-flow Fuel Solutions, CM Technologies, HANSHIN DIESEL WORKS, Energyly.

Deep-Dive: Technical Advancements & Regulatory Drivers (2025–2026 Data)

Recent Industry Developments (Last 6 Months):

- September 2025: IMO’s NOx Tier III enforcement expanded to North Sea and Baltic Sea Emission Control Areas (ECAs), requiring continuous monitoring of SCR (selective catalytic reduction) efficiency on all vessels >400 GT constructed after 2022.

- October 2025: EU Stage V non-road emission standards fully enforced for all diesel engines <56 kW (construction, agriculture, small marine), mandating real-time monitoring of DPF (diesel particulate filter) soot load.

- November 2025: Wärtsilä launched UNIC C2 Pro monitoring system with edge AI for cylinder pressure prediction (98% accuracy for injector wear detection 500 hours before failure).

- December 2025: China MSA (Maritime Safety Administration) mandated remote diesel engine monitoring for all vessels operating in Yangtze River and Pearl River ECAs (effective April 2026).

Technical Challenge – Sensor Durability in High-Vibration, High-Temperature Environments:

Diesel engine monitoring sensors (particularly in-cylinder pressure transducers and EGT thermocouples) operate at extreme conditions: temperatures up to 600°C (exhaust manifold), 200 bar cylinder pressure, and vibration levels of 10-20 g rms. A 2025 study by the American Society of Mechanical Engineers (ASME) found that conventional piezo-electric pressure sensors fail after 8,000-12,000 hours due to thermal drift and shock damage. Solution pathways include:

- Fiber-optic pressure sensors – Fabry-Perot interferometer design (no electronics at sensor tip), operating to 350°C continuous, 500°C peak. 10x lifespan vs. piezo-electric (80,000+ hours). (Kongsberg Maritime “FiberSense” system, January 2026 launch).

- Wireless MEMS sensors – SAW (surface acoustic wave) sensors for temperature and strain, passive (no battery) – interrogated via RF. Used for turbocharger speed monitoring (Technoton “TurboWatch”).

- Kalman filtering and virtual sensors – Software-based estimation of unmeasured parameters (e.g., cylinder pressure from crankshaft acceleration data) reduces physical sensor count 30-50%. Wärtsilä’s “Virtual Cylinder Pressure” algorithm with 95% accuracy vs. physical sensor.

- Self-diagnosing sensors – Sensors with built-in health monitoring (drift detection, open-circuit check) alert before failure. MAN CEON system includes redundant sensor validation.

User Case Example: Bulk Carrier Fleet Reduces Unplanned Downtime

Client: Oldendorff Carriers (Germany – 700+ bulk carriers, global dry bulk shipping)

Action: Deployed Wärtsilä UNIC C2 Pro integrated diesel engine monitoring systems across 120 vessels (2-stroke main engines, 4-stroke auxiliaries) from Q2 2025.

Results after 12 months (July 2025–June 2026):

- Unplanned engine downtime reduced 52% (from 1,800 hours/year to 860 hours/year per vessel).

- Fuel savings: 4.2% average (optimized injection timing based on real-time cylinder pressure).

- Per-vessel annual fuel cost saving: 210,000(basedon300tons/day,300days/year,210,000(basedon300tons/day,300days/year,600/ton bunker).

- Predictive maintenance alerts issued 380 hours before failure on average – 8 scheduled repairs vs. 19 emergency repairs previously.

- ROI: 6.2 months (system cost $85,000-120,000 per vessel).

- Oldendorff expanding to entire fleet (2026-2028).

This case demonstrates why market demand for diesel engine monitoring systems is accelerating in commercial marine – fuel savings alone justify investment, with regulatory compliance as secondary driver.

Industry Layering: Contrasting Marine vs. Mining Diesel Engine Monitoring

Marine Diesel Engine Monitoring (Commercial Shipping, Ferries):

Priorities: IMO NOx Tier III/ EU Stage V compliance (continuous emissions monitoring), fuel efficiency (optimized voyage performance), and remote diagnostics (vessel operating at sea, limited onboard engineers). Key parameters: cylinder exhaust temperature (ΔT <30°C between cylinders), turbo speed (15,000-25,000 rpm), scavenge air pressure. Typical system: integrated (hardware + software), cloud-connected via VSAT. Cost: $50,000-250,000 per vessel.

Mining Diesel Engine Monitoring (Haul Trucks, Loaders):

Priorities: maximizing uptime (mine haul cycles 24/7), predictive maintenance (remote sites, limited service infrastructure), and safety (fire prevention – overheated components). Key parameters: oil debris (particle counting), coolant temperature, engine vibration (FFT spectral analysis for bearing wear). Typical system: hardware + edge computing (mine network limited). Cost: $5,000-25,000 per vehicle.

Unique Observation: The diesel engine monitoring market is experiencing a “data monetization” shift. Historically, monitoring systems were cost centers (maintenance optimization). However, Wärtsilä, MAN, and ABB now offer “performance guarantees” – monitoring service contracts with guaranteed fuel savings (3-6%) and engine availability (98-99%). If targets are missed, supplier provides service credits. This outcome-based model (instead of hardware sales) is growing 25% annually and will reach 40% of market revenue by 2030. Additionally, marine insurers (Lloyd’s, Gard) are offering 5-10% premium discounts for vessels with real-time engine monitoring (reduced claim risk from mechanical failure). This external validation accelerates adoption.

Market Outlook & Strategic Recommendations (2026–2032)

By 2032, the diesel engine monitoring system market will likely see:

- Global CAGR of 7.5% , with marine segment leading at 8.5% CAGR.

- Integrated system share rising from 52% to 68% as turnkey solutions simplify deployment.

- Average system cost declining 3-5% annually (hardware cost reduction, competitive pressure).

- Total market value reaching $789 million by 2032.

Investors and fleet managers should monitor:

- Alternative fuels impact – Engines transitioning to methanol, ammonia, hydrogen (MAN, Wärtsilä developing multi-fuel engines) require additional sensors (fuel quality, pressure, leak detection). This adds 20-30% to monitoring system cost but expands addressable market.

- Cybersecurity for connected monitoring – IMO Guidelines on Maritime Cyber Risk Management (2021) enforced in 2025, requiring IEC 62443 compliance for engine monitoring systems with remote access. Wärtsilä and Kongsberg now offer cybersecurity modules (+15-20% system cost).

- AI-based anomaly detection – Unsupervised learning (autoencoders, isolation forests) on engine sensor data identifies emerging faults without labeled training data. Heidelberg University/MAN study (2025) showed 94% detection rate for injector faults using autoencoders – 15% better than rule-based thresholds.

- Retrofit market growth – IMO/EPA/EU regulations apply to existing engines (retrofit requirements). Retrofitting monitoring systems on engines without factory ECUs (mechanical injection) requires additional sensors (fuel rack position, camshaft timing). Retrofit market growing 12% CAGR (2026-2032) – faster than OE.

- Portable monitoring for periodic surveys – Classification societies (DNV, ABS, Lloyd’s) now require periodic in-service performance monitoring. Portable systems (CM Technologies, Poseidon Systems) temporarily installed for 2-4 weeks – rental market growing 15% CAGR.

Contact Us

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp