QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Product Label Review Service- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Product Label Review Service market, including market size, share, demand, industry development status, and forecasts for the next few years.

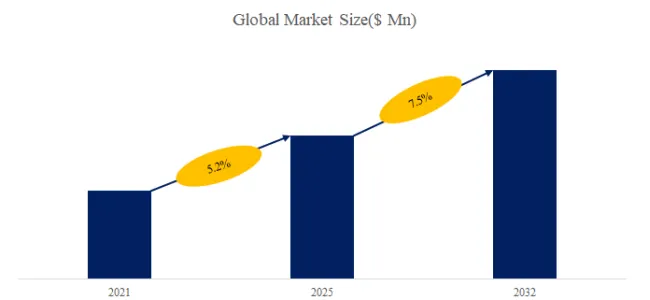

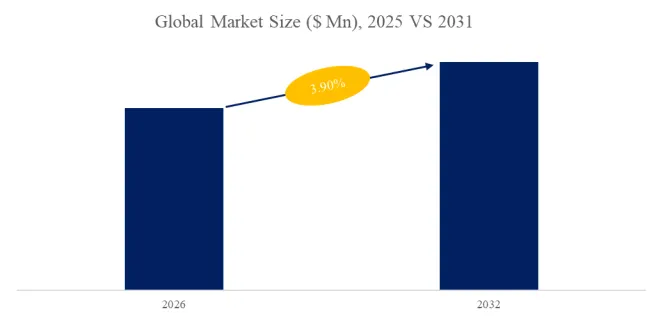

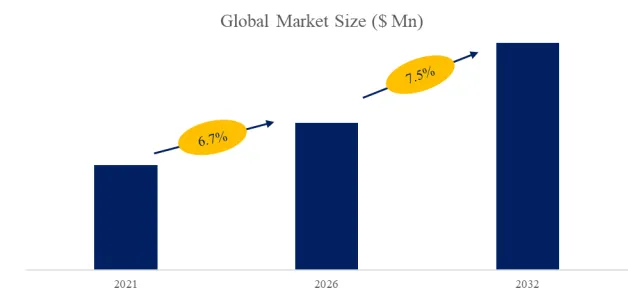

The global market for Product Label Review Service was estimated to be worth US$ 3410 million in 2025 and is projected to reach US$ 5679 million, growing at a CAGR of 7.5% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6705283/product-label-review-service

Product Label Review Service Market Summary

According to the new market research report “Global Product Label Review Service Market Report 2026-2032”, published by QYResearch, the global Product Label Review Service market size is projected to reach USD 5.68 billion by 2032, at a CAGR of 7.5% during the forecast period.

Product label review service is a technical service provided by specialized agencies or compliance consultants to systematically verify and evaluate the labeling information displayed on product packaging, hangtags, electronic labels, or instruction manuals. This service is widely utilized across various industries—including food, cosmetics, daily chemical products, textiles, electronics, toys, luggage, and medical devices—and is particularly critical in the context of cross-border trade, where compliance with the diverse regulatory frameworks of different countries and regions is essential.

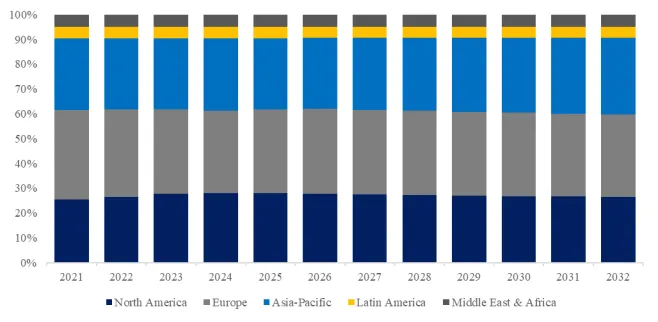

Figure00001. Global Product Label Review Service Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Product Label Review Service Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Market Drivers:

1. Major global economies are continuously strengthening legislation and enforcement regarding consumer product labeling. Across a wide spectrum of goods—ranging from food and cosmetics to electronics and textiles—regulatory bodies are imposing increasingly detailed and legally binding requirements concerning ingredient disclosure, allergen identification, net content accuracy, safety warnings, expiration dates, and claims regarding special functions. Should companies fail to meet these standards—whether due to missing information, errors, or misleading content on their labels—they risk facing substantial fines, product recalls, or even market bans. Consequently, professional labeling review services have become an indispensable support mechanism for businesses seeking to mitigate compliance risks.

2. As labeling regulations for food, cosmetics, health supplements, medical devices, chemicals, and consumer goods are constantly updated across various nations, businesses face increasingly complex compliance requirements. Markets such as the EU, the U.S., China, Japan, and the Middle East continue to raise their standards regarding ingredient disclosure, allergen labeling, nutritional information, origin statements, environmental claims, and language specifications; this trend is driving brands and export enterprises to rely increasingly on professional labeling review services to mitigate the risks of product recalls, fines, and customs clearance issues.

3. The rapid expansion of global supply chains and cross-border e-commerce has created a need for numerous enterprises to simultaneously comply with labeling regulations across multiple countries and regions. Given the significant disparities among nations regarding ingredient nomenclature, units of measurement, nutritional claims, warning statements, and certification marks—and the difficulty for companies to fully address these complexities using internal teams alone—third-party labeling review services have emerged as a critical compliance support mechanism for export-oriented enterprises seeking to enter international markets.

Restraint:

1. Regulatory frameworks, language requirements, and industry standards vary significantly across different countries and regions—and are subject to frequent updates—making it challenging to establish unified standards for label review services. Service providers must continuously invest in regulatory databases, expert teams, and localization capabilities, thereby increasing both operational costs and service complexity.

2. A large number of small and medium-sized manufacturers and export enterprises have relatively limited budgets for label audits; some prefer to handle label content internally, seeking professional services only in the event of export spot checks, specific client requests, or the occurrence of issues. This cost sensitivity limits the industry’s penetration within the low-to-mid-range market segments.

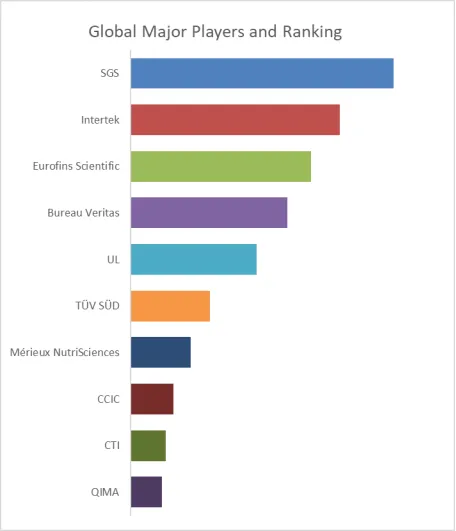

Figure00002. Global Product Label Review Service Top Ten Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Product Label Review Service Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

This report profiles key players of Product Label Review Service such as SGS, Intertek, Eurofins Scientific, Bureau Veritas and UL.

In 2025, the global top ten Product Label Review Service players account for 60% of market share in terms of revenue. Above figure shows the key players ranked by revenue in Product Label Review Service.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Product Label Review Service market is segmented as below:

By Company

SGS

AIB International

Marie Gale

Intertek

Eurofins Scientific

Prime Label

Food Consulting Company

CIRS Group

TÜV SÜD

UL

Bureau Veritas

ITA Corporation

CCIC

NutriData

Mérieux NutriSciences

EAS Consulting Group

Qualitas Executive Group

V-Label

Label Bank

CAS Testing

CTI

Segment by Type

Regulatory Compliance Review

Ingredients and Formulation Review

Others

Segment by Application

Food & Beverages

Cosmetics

Chemicals

Others

Each chapter of the report provides detailed information for readers to further understand the Product Label Review Service market:

Chapter 1: Introduces the report scope of the Product Label Review Service report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Product Label Review Service manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Product Label Review Service market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Product Label Review Service in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Product Label Review Service in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Product Label Review Service competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Product Label Review Service comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Product Label Review Service market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Product Label Review Service Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Product Label Review Service Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Product Label Review Service Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp