QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Crossover SUVs- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Crossover SUVs market, including market size, share, demand, industry development status, and forecasts for the next few years.

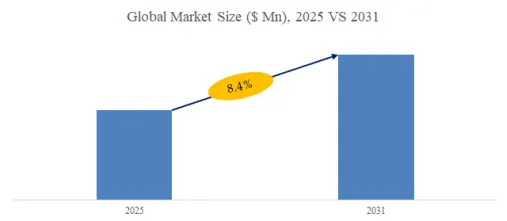

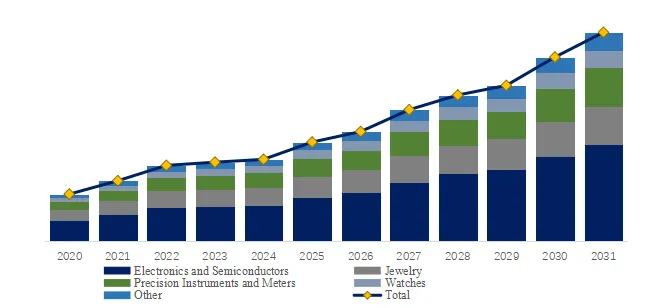

The global market for Crossover SUVs was estimated to be worth US$ 1618 million in 2025 and is projected to reach US$ 2373 million, growing at a CAGR of 5.7% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5543783/crossover-suvs

1. Crossover SUVs Product Introduction

The core demands and business opportunities for All Electric SUVs can be summarized into four key points: First, the anxiety over range and charging drives opportunities for battery technology innovation (such as solid-state batteries) and the deployment of ultra-fast charging networks. Second, the intelligent experience (including advanced driver-assistance systems and smart cockpits) has become a new core purchasing driver and a source of profitability for software services. Third, platform-based vehicle manufacturing enables optimization of R&D costs and opens up space for personalized, modular product definition. Fourth, ecosystem expansion based on the vehicle’s global electronic and electrical architecture, such as V2G (vehicle-to-grid) and data value-added services, fosters innovative business models in the aftermarket.

Figure1: Crossover SUVs Product Picture

Based on or includes research from QYResearch:

2. Leading Manufacturer in the industry

1) Subaru

Subaru, as a globally renowned automobile manufacturer, centers its core business around the research and development, production, and sales of passenger cars and SUVs, while simultaneously dedicating itself to enhancing the overall user mobility experience and vehicle reliability. The company has long adhered to technological innovation, shaping its vehicle lineup through unique core technologies such as the horizontally opposed BOXER engine and Symmetrical All-Wheel Drive (AWD). These technologies not only improve handling performance and safety but also enhance vehicle stability and capability across various road conditions. Subaru sells a diversified range of models in multiple global markets, covering sedans, crossover SUVs, and other light vehicles, and continuously introduces advanced safety systems like EyeSight driver-assist technology to improve driving comfort and peace of mind. Concurrently, Subaru is advancing its product portfolio in hybrid and electrification technologies, making its powertrain combinations more environmentally friendly and efficient, thereby further enriching the brand’s technological capabilities and product lineup.

Subaru has built a product matrix encompassing large SUVs, midsize SUVs, and compact SUVs, meeting different user needs for space, performance, and multi-purpose travel. As the representative of its compact SUVs, the Subaru Crosstrek, based on standard Symmetrical Full-Time AWD, comfortable passenger space, and high ground clearance, achieves an excellent balance between daily urban driving and weekend outdoor adventures, while also offering a hybrid version to improve fuel efficiency and environmental performance. In the midsize SUV segment, the Subaru Forester provides more spacious interior room, advanced driver-assist systems, and outstanding all-terrain capability, making it an ideal choice for family travel and long-distance journeys. As for large SUVs, the Subaru Ascent, as the brand’s largest SUV, offers three rows of seating, more powerful engine output, and ample cargo capacity, making it particularly suitable for large families or users requiring higher passenger and towing capabilities. The entire crossover SUV lineup emphasizes Subaru’s consistent practicality, reliability, and the comprehensive traction advantage of AWD, ensuring competitiveness across different market segments.

The Subaru Crosstrek is a highly practical and multi-faceted compact all-wheel-drive SUV that garners widespread attention for its well-rounded performance, excellent capability, and reliability. As a vehicle equipped standard with the Symmetrical Full-Time All-Wheel Drive system, the Crosstrek performs effortlessly whether for daily urban commuting or weekend outdoor exploration. The latest 2026 model adopts a more powerful standard 2.5-liter horizontally opposed BOXER four-cylinder engine, delivering approximately 180 horsepower and 178 lb-ft of torque, representing a significant improvement over previous versions, and continues to utilize a CVT (Continuously Variable Transmission) to optimize fuel economy and driving smoothness; furthermore, it introduces the all-new Crosstrek Hybrid model, which features a hybrid system combining a 2.5-liter engine with dual electric motors, offering stronger combined power and higher efficiency to meet consumer demands for both performance and environmental friendliness. The overall design of the Crosstrek emphasizes space and functionality, providing generous passenger and cargo room, with a maximum interior volume of approximately 120 cubic feet and a flexible rear seat configuration. Combined with its high ground clearance, this gives it stable performance on mud, gravel, and even light off-road conditions. Standard equipment includes Subaru’s EyeSight driver-assist technology and optional DriverFocus Distraction Mitigation System, along with a comprehensive suite of active safety features such as Blind-Spot Monitoring, Rear Cross-Traffic Alert, and Automatic Reverse Braking, offering drivers all-around peace of mind. Whether for family users seeking daily practicality or for outdoor adventure enthusiasts, the Crosstrek, with its balanced power, reliable AWD capability, practical space, and advanced safety technology, stands as a highly competitive compact SUV choice.

2) Kia

KIA is a globally renowned automobile manufacturing enterprise focused on the design, research and development, production, and sales of passenger vehicles and multi-purpose vehicles. It adheres to a user-value-centric approach to create competitive products and mobility solutions. As a key member of the Hyundai Motor Group, KIA has established a comprehensive production and sales network in numerous countries and regions worldwide. By launching a diversified product portfolio covering sedans, SUVs, MPVs, and new energy vehicles, KIA meets the demands of different markets while continuously enhancing its technological capabilities and brand influence. The company consistently innovates in areas such as powertrain systems, intelligent technology, safety features, and environmentally friendly technologies. Combined with a youthful and sporty design language, it provides users with high-quality, driving-pleasure-oriented, and practical automotive products. KIA also offers financial, after-sales, and smart connectivity services to enhance the overall ownership experience and brand loyalty. KIA vehicles are exported to multiple global markets, and its robust market performance and brand strength position it as one of the world’s leading automotive brands.

Within KIA’s Crossover SUV lineup, the brand has built a product system covering compact, midsize, and large SUVs, catering to various mobility needs ranging from urban commuting to family travel and cross-regional journeys. As a representative of compact SUVs, the KIA Seltos gains market attention with its stylish and avant�garde exterior design, spacious and practical interior, and abundant technological features. It also offers multiple powertrain choices and intelligent safety systems, giving it strong competitiveness in its segment. The compact product line also includes the Sportage, a model that meets daily multi�purpose usage scenarios with its agile handling, comfortable ride, and diverse powertrain combinations. Moving into the midsize SUV segment, the KIA Sorento provides more comprehensive functionality and comfort for family users through its larger body dimensions, more generous passenger space, optional three�row seating arrangement, and efficient powertrain configurations. In the large SUV market, the KIA Telluride (referred to in some markets as a large three�row SUV) offers a premium choice for users requiring greater passenger capacity and long�distance travel capability, with its sense of luxury, powerful performance, excellent capability, and rich array of intelligent technologies. Overall, KIA’s crossover SUV series upholds the brand’s integrated pursuit of design, performance, practicality, and safety, delivering distinctive multi�purpose mobility solutions that meet user expectations across different market segments.

The second�generation KIA Seltos represents the brand’s comprehensively upgraded model in the global compact SUV segment, crafted through in�depth optimization in design, dimensions, powertrain, technological features, and functionality to create a more competitive modern crossover SUV. The all�new Seltos adopts KIA’s latest “Opposites United” design language, giving it a more avant�garde and powerful appearance. Signature elements such as the wide tiger�nose grille, complemented by vertical LED daytime running lights, a full�width rear light bar, hidden door handles, and other details, enhance the overall sense of technology and visual impact. Simultaneously, the body dimensions have increased significantly, with a length of approximately 4,430 mm, width of 1,830 mm, and a wheelbase of 2,690 mm, substantially improving interior space and cargo capacity. The trunk volume has also been increased to approximately 536 L, offering superior practicality compared to vehicles in the same class. Inside, the all�new Seltos is equipped with dual 12.3�inch Trinity panoramic curved displays and an additional 5�inch center touchscreen, along with premium materials and ergonomic layouts. It supports wireless Apple CarPlay and Android Auto, ventilated/heated seats, a panoramic sunroof, and a host of other technological and comfort features, creating a modern and luxurious driving environment. In terms of powertrain, the second�generation Seltos retains multiple engine options, including a 1.6�liter turbocharged and a 2.0�liter naturally aspirated gasoline engine, paired with manual, DCT, 8�speed automatic, or CVT transmissions. Some markets will also introduce a hybrid version to balance performance and fuel economy. An available AWD system and multiple drive modes enhance all�weather and road�condition adaptability. Furthermore, the new vehicle integrates advanced driver�assistance safety systems and parking�assist functions, providing users with comprehensive peace of mind during daily driving and long�distance trips. This makes the second�generation Seltos a flagship choice in the compact crossover SUV segment that combines space, technology, performance, and practicality.

3) Hyundai

Hyundai, as one of the world’s leading automobile manufacturers, is engaged in the design, development, production, and sales of passenger cars, SUVs, multi-purpose vehicles, and future mobility technologies. With a global network of production bases and sales channels, Hyundai exports its products to numerous countries and regions. Driven by technological innovation and consumer demands, the company offers a wide range of powertrains, including traditional gasoline vehicles, hybrid vehicles, electric vehicles, and hydrogen fuel cell cars. Hyundai continuously enhances its competitiveness in areas such as smart connectivity, safety assist systems, in-car technology, and mobility services. Additionally, Hyundai strengthens consumer ownership experiences and brand loyalty through financial services, after-sales support, and localized operational strategies, ensuring continued growth and stable development in the global automotive industry.

Hyundai has created a Crossover SUV lineup that spans compact SUVs, mid-size SUVs, and large SUVs, catering to diverse needs from urban commuting to family trips and long-distance travel. In the compact SUV segment, Hyundai offers models like the Venue, Kona, Tucson, and Mufasa, known for their agile handling, compact size, efficient powertrains, and rich technological features. These models are suitable for urban driving while also capable of handling all-weather conditions. Moving into the mid-size SUV category, models like the Santa Fe provide more spacious interiors, enhanced safety and comfort features, optional AWD, and hybrid systems, offering a reliable and comfortable travel experience for families. In the large SUV market, the Palisade serves as Hyundai’s flagship three-row SUV, offering generous seating space, strong performance, large cargo capacity, and advanced tech features, making it ideal for users needing extra passenger and long-distance capabilities. Moreover, Hyundai is actively advancing its electrification strategy in the SUV sector, with models like the IONIQ series electric crossover SUVs, which not only expand the product line but also reflect the brand’s long-term investment and development in sustainable mobility technologies and electrification.

The Hyundai MUFASA is a compact crossover SUV designed specifically for the Chinese market, targeting urban family users and young consumers with a combination of stylish design, advanced technology features, and practicality. The vehicle is built on Hyundai-Kia’s N3 global platform, with dimensions of approximately 4475 mm × 1850 mm × 1665 mm and a wheelbase of 2680 mm. It offers a sleek and dynamic exterior design, a 5-door, 5-seat layout, and ample space for both passengers and cargo within the compact SUV category, while maintaining a modern and powerful design language. In terms of powertrain, the MUFASA is equipped with a 2.0L naturally aspirated four-cylinder engine, delivering a maximum output of about 160 horsepower (118 kW) and 193 Nm of torque, paired with a 6-speed automatic transmission and front-wheel drive. It offers stable and reliable performance for city commuting and highway cruising, with excellent fuel efficiency. The interior is well-equipped with features such as a large digital cockpit screen, dual 12.3-inch TFT-LCD screens, an intelligent connectivity system, wireless Apple CarPlay/Android Auto, Qi wireless charging, a panoramic sunroof, and multi-zone ambient lighting, providing both technological sophistication and comfort. The MUFASA is available in multiple trim levels and comes with comprehensive active safety features, including Level 2 driver assistance systems and Hyundai SmartSense, enhancing driving convenience and safety. Additionally, the vehicle’s “Multi-Zone” interior design and more than thirty storage compartments further improve practicality, making it a highly cost-effective choice for families looking for an SUV that combines space, smart technology, and efficiency for daily use and weekend trips in the compact SUV market.

4) Toyota

Toyota operates as one of the world’s most influential and diversified automotive manufacturers, with business activities that span the design, development, production, and global distribution of a wide range of mobility products, including passenger cars, trucks, commercial vehicles, and electrified vehicles. Its operations integrate advanced powertrain technologies—such as gasoline, hybrid, plug�in hybrid and battery electric systems—alongside connected vehicle services, safety and driver�assistive technologies, and mobility solutions aimed at enhancing the user experience and improving safety, efficiency and sustainability. Toyota’s business also includes financial services that provide flexible ownership solutions such as financing, leasing and insurance support, helping to broaden customer access to its products and strengthen long�term relationships with end users. Through localized production, collaborative partnerships worldwide, and a sustained focus on innovation across materials, manufacturing processes and software development, Toyota continually works to optimize quality, reduce environmental impact, and reinforce its reputation for durability and reliability in diverse markets globally.

In the realm of Crossover SUVs, Toyota has developed a comprehensive and tiered product lineup that addresses a spectrum of user needs from urban commuting to family travel and outdoor adventure, structured across compact, mid�size and large SUV segments with an emphasis on comfort, capability and efficiency. At the compact level, models such as the Toyota Corolla Cross and Toyota RAV4 deliver practical versatility with agile handling, efficient powertrains—including hybrid and plug�in hybrid options—and a balanced blend of everyday usability, safety technologies and cargo flexibility that suit daily city driving and weekend excursions. Moving into the mid�size category, vehicles like the Toyota Highlander and Grand Highlander offer expanded interior space, available three�row seating, advanced infotainment and connectivity features, and strong hybrid system options, making them well�suited for larger families or those needing extra passenger and cargo capacity. At the large SUV end, models such as the Toyota 4Runner, Land Cruiser and Sequoia provide robust performance, enhanced towing capability, rugged off�road credentials and premium comfort amenities that cater to long�distance travel, adventure�oriented lifestyles and demanding utility applications. Across all segments, Toyota’s SUV lineup integrates its hallmark reliability, a wide array of advanced safety systems and multiple powertrain choices designed to elevate driving confidence and deliver tailored solutions for diverse mobility preferences.

The all-new Lexus RZ is a mid-size luxury Crossover SUV designed for the era of electrification, built on a dedicated electric platform that combines luxury, advanced technology, exceptional handling, and powerful performance to offer a highly competitive pure electric driving experience. The design language of the RZ continues Lexus’s tradition of elegance and dynamic styling, with a well-proportioned body and smooth lines. It also features details such as a one-touch electrochromatic panoramic sunroof and slim, continuous taillights, enhancing its modern, high-tech appearance. Inside, the RZ boasts a large touch screen, luxurious ambient lighting, and electronic shift-by-wire controls, creating a refined and modern cockpit environment.

Built on a dedicated BEV platform with a low center of gravity, the RZ delivers excellent dynamic performance. It offers multiple powertrain options, ranging from an entry-level 221 horsepower version to a high-performance version with over 400 horsepower. The advanced DIRECT4 all-wheel-drive system enhances traction and response speed, providing a driving experience that is both smooth and exhilarating. The vehicle also excels in smart safety features, equipped with Lexus’s latest intelligent safety system and numerous driver-assistance technologies to enhance peace of mind during everyday driving. Additionally, the RZ’s range and charging performance have been optimized, offering long-range capability and convenient charging, making it a pure electric mid-size SUV that seamlessly balances luxury, performance, and practicality.

5) Honda

As a world-leading comprehensive mobility enterprise, Honda operates across multiple domains including automobiles, motorcycles, power products, and related financial services. It globally develops, manufactures, and sells a diverse range of mobility products and services. The automobile business is one of its core divisions, primarily encompassing passenger vehicles and commercial models such as sedans, SUVs, and light trucks. Simultaneously, through its financial services arm, Honda provides customers with loan, leasing, and insurance support to enhance the overall user experience. The motorcycle business covers a wide spectrum from urban commuting to off-road leisure models and maintains a long-standing leading position in numerous markets. The power products business offers a broad range of equipment such as generators, engines, and pumps to meet both personal and industrial needs. Additionally, the company actively promotes R&D innovation and localized manufacturing in multiple regions worldwide, collaborating with partners to expand markets and strengthen brand influence.

Within its Crossover SUV lineup, Honda has built a richly layered family of models that caters to diverse mobility needs, ranging from compact to midsize and large SUVs, addressing varied usage scenarios from daily commuting and family travel to light off-roading. In the compact segment, the CR�V has gained wide recognition for its spacious and practical interior, efficient powertrain options (including hybrid versions), responsive handling, and advanced safety assist systems, striking a balance between fuel economy and comfort. The smaller HR�V offers a more agile body, higher fuel efficiency, and a driving experience suited to urban environments. In the midsize and large SUV segments, Honda provides models such as the Passport and Pilot. These larger vehicles deliver stronger cargo and passenger capacity, higher-output powertrain configurations, and the latest intelligent safety technologies, offering highly competitive choices for families or those requiring greater space, enhanced comfort, and more comprehensive functionality for long-distance travel.

Honda offers a complete Crossover SUV portfolio covering everything from daily commuting to full-family travel, including compact, small, and midsize/large SUVs to meet different user needs for space, performance, efficiency, and utility. The representative compact SUV is the 2026 Honda CR�V, a crossover SUV designed with a blend of modern style and practicality, focusing on agile handling, spacious interiors, and efficient powertrains. It offers a choice between a conventional 1.5L turbocharged engine or an efficient hybrid system. Hybrid variants (such as the CR�V TrailSport Hybrid) come standard with AWD, a 5�seat layout, approximately 35 MPG combined fuel economy, about 36.3 cubic feet of cargo space, and a comprehensive suite of safety assist systems, making it suitable for daily urban driving and weekend getaways. The small SUV segment is defined by the Honda HR�V. With its more compact dimensions, flexible seating, standard 5�seat configuration, and high fuel efficiency, it features a convenient 9�inch infotainment touchscreen, wireless connectivity, HondaLink, and available AWD, designed specifically for city commuting and light outdoor activities. In the midsize to large SUV category, Honda offers the Passport and Pilot. The Passport is a two-row midsize SUV emphasizing performance and off-road capability, typically equipped with a more powerful engine, available AWD, and increased cargo space. The Pilot is a larger three-row SUV accommodating up to 7–8 passengers. It provides more generous interior space, robust power, and comfort for family trips, catering to families with long-distance travel and towing needs.

3. Key Market Trends, Opportunity, Drivers and Restraints

1) Market Trends

The Crossover SUV industry is experiencing three core development trends: the deepening integration of technologies, a pragmatic shift in powertrain strategies, and the innovation of product forms. With the deep integration of artificial intelligence (AI) and consumer electronics, Crossover SUVs are not only showcasing a new level of intelligence but are gradually becoming a driving force in the automotive industry’s technological revolution. For instance, the introduction of next-generation central computing platforms like NVIDIA’s DRIVE Thor is driving the convergence of intelligent driving and smart cabins, allowing every part of the vehicle to integrate closely with AI, thus enhancing user driving experiences and safety. In addition, cross-industry collaborations are becoming more frequent, with automakers partnering with tech companies like Sony, NVIDIA, and Qualcomm. These partnerships are accelerating the development of next-generation smart cars and driving the advancement of automotive intelligence. In terms of powertrain strategies, Crossover SUVs are shifting from a single focus on electric technology to a more pragmatic, diversified powertrain strategy. Given the varying infrastructure and consumer acceptance of electrification in different global markets, hybrid technologies are being reassessed and gaining strategic importance. Many global automakers are introducing hybrid versions of their fuel-powered vehicles or expanding their hybrid product lines to meet diverse market demands. This shift allows Crossover SUVs to flexibly adapt their powertrain systems across different markets, ensuring competitiveness in a diverse range of environments. As for product forms, Crossover SUVs are continuously extending into new travel scenarios. The emergence of MPSUV (Multi-Purpose Sport Utility Vehicle) as a new category, aimed at combining the off-road performance of SUVs with the spacious comfort of MPVs, is fulfilling the diverse needs of family travel. Meanwhile, cars are evolving from mere transportation tools to “smart lifestyle terminals” and “third living spaces,” with integration into smart home and travel service ecosystems becoming a frontier of exploration. This trend is pushing Crossover SUVs to break traditional boundaries and move toward a more diversified and scenario-based future.

6) Opportunities

The structural transformation of the Crossover SUV industry has created differentiated opportunity windows for both new and existing players. In the differentiated competition within the smart ecosystem, technology companies or those with ecosystem advantages have unique opportunities to position vehicles as key nodes within their smart ecosystems. For instance, Xiaomi’s “full ecosystem of car, home, and personal devices” integrates vehicle systems with smart home devices, while Geely’s “big mobility ecosystem” links aviation and ground transportation, aiming to innovate through scenario integration and bypass traditional mechanical performance competition by focusing on software and ecosystem services. This approach offers Crossover SUV manufacturers new paths to establish stronger user engagement through ecosystem services. Additionally, as demand for segmented markets continues to grow, there are significant opportunities for Crossover SUVs in category innovation and deep market exploration. In mature markets, many unmet personalized needs remain. Companies can stand out in competition by introducing new niche categories, such as crossover wagons or MPSUVs, or by deeply optimizing products for specific scenarios (e.g., focusing on “parking scenario value”). Moreover, the professional division of labor in the industry chain offers collaboration opportunities for Crossover SUV manufacturers, especially under the trend of “manufacturing outsourcing.” Open car manufacturing platforms like Foxconn’s MIH provide opportunities for light-asset companies to enter the market, enabling collaboration with other manufacturers to participate in the automotive value chain restructuring without heavy capital investment. This collaborative model allows companies with expertise in user operations, sales channels, and specific technologies to more flexibly engage in the production and promotion of Crossover SUVs. Finally, the differentiated global market layout provides additional opportunities for Crossover SUV manufacturers. Given the different stages of electrification and consumer preferences across regions, companies can tailor their product offerings and market expansion strategies based on their technological capabilities. For example, China is a leader in electrification and smart applications, while other markets may have higher demand for hybrid models or specific SUV sizes, enabling Crossover SUV manufacturers to implement flexible product and market strategies.

7) Challenges

As the Crossover SUV industry evolves rapidly, it faces a range of severe challenges. With the intensifying market competition, leading companies like Tesla and BYD have already captured significant market share, creating triple barriers of technology, production capacity, and brand. For new entrants, they must not only overcome substantial initial research, development, and production investments but also continue to make billions of dollars in ongoing R&D and marketing investments to maintain competitiveness in an increasingly “overheated” market, which creates significant financial pressure. Furthermore, long-term pressure regarding core technology independence and supply chain security is also a major challenge for the industry. The development of advanced battery technologies, high-level intelligent driving algorithms, and critical automotive-grade chips involves high technical barriers and rapid iteration. Crossover SUV manufacturers are under constant scrutiny for their ability to integrate rather than innovate, and whether they can establish a strong competitive edge in underlying technologies such as chassis tuning and the three-electric system (battery, motor, and electronic control) is crucial for their long-term survival. Moreover, the uncertainty in global supply chains, especially with the shifting international landscape, has increased risks related to raw material procurement and manufacturing. For cross-industry players, brand and channel restructuring pose another significant challenge. Many companies that cross over from the home appliance or technology sectors, despite having strong brand recognition in those industries, still face challenges in gaining consumer trust in their automotive products, especially in terms of safety, reliability, and performance. Additionally, existing sales channels, such as home appliance stores, are not easily convertible to the automotive sector, and establishing a specialized sales service system aligned with automotive consumer habits is costly and time-consuming. Meanwhile, the uncertain macroeconomic environment and policy risks also place considerable pressure on Crossover SUV companies. Changes in trade policies from major global economies (e.g., tariff adjustments) may significantly affect supply chain layouts and product costs. Additionally, countries’ evolving policies on data security and autonomous driving regulations present compliance uncertainties, further complicating the development of the Crossover SUV industry.

8) Industry Entry Barriers

The Crossover SUV industry, especially in the field of smart electric vehicles, faces extremely high entry barriers, which are multidimensional and systemic. First and foremost, the technical and talent barriers are the most critical. The development of Crossover SUVs involves complete vehicle platforms, the three-electric system (battery, motor, electronic control), intelligent driving, and smart cabins, all of which require deep technical accumulation and a large, multidisciplinary team of high-end talent. These technical accumulations and talent reserves cannot be quickly obtained through capital alone, and breakthroughs must come after years of research and development as well as talent cultivation. Second, capital and scale barriers are particularly prominent in the automotive industry. As a capital and scale-intensive industry, the development, design, supply chain construction, factory construction (or outsourcing fees), sales service network establishment, and brand marketing for Crossover SUVs require billions of yuan in funding. At the same time, companies must achieve a certain level of production and sales scale to amortize high fixed costs and supply chain expenses; otherwise, achieving profitability is difficult. Brand and channel barriers also present significant challenges. In an increasingly competitive market, establishing a new, trustworthy automotive brand is both difficult and time-consuming. Consumers’ trust and recognition of a brand must be built over time through market accumulation and word-of-mouth, while constructing an efficient, user-friendly, and widespread sales, delivery, and after-sales service system requires massive investments in capital, manpower, and long-term operational accumulation. Supply chain and qualification barriers are reflected in the reliance on a stable supply of critical components such as chips and batteries, which have become strategic capabilities for enterprises. Additionally, obtaining production qualifications for automobiles in many countries is a stringent administrative and market entry hurdle. Lastly, the emerging barriers of ecosystem and data are becoming increasingly important. In the field of smart electric Crossover SUVs, creating a vehicle-based smart software ecosystem and the ability to obtain vast amounts of driving data to continuously optimize algorithms and improve user experience is becoming a competitive advantage for leading companies. These leading companies are continuously optimizing their technology and services through a large stock of vehicles, making it nearly impossible for new entrants to catch up with this technological accumulation and ecosystem advantage in the short term. Thus, the entry barriers for the Crossover SUV industry are not only challenges related to capital and technology but also to brand, channels, supply chains, and data ecosystems.

4. Supply Chain Analysis

1) Upstream Market

a) Basic Structural Materials — Steel and Aluminum Alloys

In the industry chain of Crossover SUVs, basic structural materials play a crucial role, primarily including steel and aluminum alloys. These materials directly influence vehicle lightweighting, strength, and safety, thereby impacting overall performance and driving experience. Steel, particularly high-strength steel and hot-formed steel, serves as the core material for the body and chassis of Crossover SUVs. The advantage of high-strength steel lies in its ability to provide high compressive strength while reducing vehicle weight under the premise of ensuring overall safety, contributing to improved fuel economy and power performance. The fifth-generation ultra-high-strength steel widely used in modern vehicles is provided by domestic major automotive sheet supplier Baosteel Group. It is extensively applied in key structural components such as body frames and door beams, providing collision safety assurance for vehicles. As lightweighting becomes a global trend in automotive manufacturing, the application proportion of aluminum alloys in Crossover SUVs continues to increase. Aluminum alloys not only offer good corrosion resistance and a high strength-to-weight ratio but also effectively reduce body weight, improving fuel efficiency and the range performance of electrified models. Global aluminum industry giants such as Novelis have increasingly close collaborations with automakers, promoting the widespread application of aluminum alloys. For example, the LeS6 Ultra aluminum alloy co-developed by Li Auto and Novelis has a yield strength three times higher than traditional aluminum alloys. It is successfully applied in critical safety components such as battery underbody protection plates, ensuring battery pack safety and optimizing the performance of electric Crossover SUVs. The application of these foundational materials enables Crossover SUVs to better meet market demands for lightweighting and high performance while adhering to safety standards.

b) Powertrain System Materials

In the powertrain materials sector for Crossover SUVs, especially for new energy Crossover SUVs, battery materials are the highest cost and technical barrier component, accounting for approximately 30%-40% of the total vehicle cost. Battery raw materials primarily include lithium, cobalt, nickel, manganese, graphite, and others. Chinese companies dominate the global lithium battery material supply chain. For example, fluctuations in the price of key materials such as lithium carbonate (which dropped from a peak of 56,000 RMB per ton in 2022 to 8,000 RMB per ton in 2024) directly impact the total vehicle cost and pricing strategy. Battery components and vehicle manufacturers include cathodes, anodes, separators, electrolytes, cells, and battery packs (PACK). The market is highly concentrated, with leading companies such as CATL, BYD, and Contemporary Amperex Technology Co. Ltd. accounting for more than 75% of the market share. Some companies are attempting vertical integration, such as Hubei Chutian New Energy, which extends from battery manufacturing to vehicle production through its parent company’s channels, promoting the collaborative development of batteries and vehicles. The high technical barriers and cost associated with these powertrain materials form the core competitive edge in the new energy Crossover SUV industry, pushing companies to continuously seek breakthroughs in supply chain management, technological innovation, and market adaptability.

c) Intelligent Materials and Components — Automotive-grade Chips (MCU, SoC), Sensors (Cameras, Millimeter-wave Radar, Lidar), Computing Platforms, Domain Controllers, etc.

In the industry chain of Crossover SUVs, intelligent materials and components represent the core upstream segment that determines a vehicle’s “intelligence quotient,” possessing high added value and involving the integration of multiple key technologies and parts. Automotive-grade chips (MCU, SoC) are the “brain” of intelligent systems, playing a vital role in processing various vehicle intelligent functions such as autonomous driving, in-vehicle infotainment systems, and vehicle connectivity. Automotive-grade chips require high performance, low power consumption, and high stability to meet the automotive industry’s demands for long-term use under harsh environmental conditions. Sensors are the perceptual organs of intelligent systems, including cameras, millimeter-wave radar, lidar, etc. They provide vehicles with precise environmental perception capabilities, forming the foundation for realizing functions like autonomous driving and Advanced Driver-Assistance Systems (ADAS). Cameras identify pedestrians, lane markings, etc., through image recognition; millimeter-wave radar detects preceding vehicles and obstacles; while lidar provides high-precision three-dimensional perception capabilities, widely used in autonomous driving systems. With advancements in computing platform and domain controller technologies, intelligent systems are gradually evolving towards centralization and modularization. Computing platforms are responsible for processing and managing various types of in-vehicle data, ensuring efficient information flow to meet the demands of autonomous driving and intelligent control. Domain controllers integrate and coordinate management of various intelligent modules (such as powertrain, body control, infotainment, etc.), simplifying traditional decentralized control systems and enhancing the reliability and response speed of intelligent systems. These intelligent materials and components work closely together in Crossover SUVs, collectively elevating the vehicle’s level of intelligence, driving the development of technologies like autonomous driving, intelligent safety, and vehicle connectivity, and providing users with a safer, more convenient, and efficient driving experience.

9) Midstream

a) Full-Size SUVs

Full‑Size SUVs are the largest category of Crossover SUVs and are defined by their greater overall size, interior volume and capacity compared to smaller SUV classes. Full‑Size SUVs typically offer expansive passenger space and cargo capacity, often accommodating three rows of seating and more generous room for occupants and their belongings, and are well‑suited for applications that demand higher passenger capacity, extended travel comfort and versatile utility. These vehicles generally feature robust powertrain options and chassis designs that emphasize towing capability and stable performance across a range of driving conditions, making them appealing to users who require substantial interior space, strong load‑carrying capability or enhanced adaptability in diverse environments. In many markets, Full‑Size SUVs are positioned with higher levels of comfort, advanced safety technology and premium equipment, elevating the overall driving and riding experience for families or commercial users who need multifunctional transport solutions. The practical advantages of larger interiors and stronger utility underpin their enduring appeal, and as consumer demand for spacious and versatile vehicles continues, Full‑Size SUVs retain strong positioning in segments where maximum space, capability and comfort are priorities.

b) Med-Size SUVs

Med‑Size SUVs sit between Compact‑Size and Full‑Size SUVs in terms of dimensions and capacity, and they represent one of the most mainstream and widely adopted categories in the SUV market. Med‑Size SUVs balance interior space, driving comfort and fuel economy more effectively than their smaller counterparts while offering more room and capability than Compact‑Size SUVs. Many Med‑Size SUVs provide flexible seating layouts that can include two or three rows of seats, enabling them to serve families and users who need both passenger accommodation and cargo capacity without the bulk of Full‑Size models. The design of these vehicles typically supports a range of driving scenarios, from urban commuting and school runs to longer highway journeys, and their powertrain and safety systems are engineered to deliver a blend of performance, efficiency and comprehensive safety support. Because Med‑Size SUVs aim to deliver a comfortable ride and versatile functionality without excessive size, they have become a preferred choice for consumers seeking all‑around usability and value within the SUV lineup.

c) Compact-Size SUVs

Compact�Size SUVs represent the most ubiquitous and broadly accepted class of Crossover SUVs in global automotive markets. Built on smaller vehicle platforms relative to Med�Size and Full�Size models, Compact�Size SUVs provide a practical combination of elevated driving position, flexible cargo space and maneuverability that suits daily urban driving and routine use. Compact�Size SUVs typically feature five�seat configurations with interior and cargo space optimized for everyday needs, and their more moderate dimensions make them easier to navigate and park in crowded urban environments. Compared with traditional sedans, these vehicles offer enhanced visibility and a more versatile interior layout, enabling drivers to carry larger loads when needed while still benefiting from efficient operation and lower ownership costs. Their balance of convenience, comfort and utility has made Compact�Size SUVs a dominant segment in overall SUV sales, and this trend persists as more consumers seek vehicles that blend everyday practicality with the elevated presence and adaptability that the SUV body style provides.

10) Downstream

a) Personal Use

In the personal use market, Crossover SUVs play a pivotal role in driving the development of the entire industry chain, as they serve as an important segment of passenger vehicles. Crossover SUVs combine the comfort of passenger cars with the higher ride height, greater luggage capacity and improved all‑around usability of SUVs, making them particularly advantageous in family daily commuting and travel scenarios; mid‑size and full‑size SUVs are often preferred by multi‑person families due to their generous interior space, elevated seating position and enhanced sense of safety. Beyond urban commuting, Crossover SUVs also support weekend short trips and light recreational excursions by enabling drivers to carry more equipment for outdoor activities, thereby enhancing the vehicle’s versatility. In addition, consumers increasingly regard Crossover SUVs as a means to express personal identity and lifestyle; vehicles from luxury brands or models with distinctive design features are frequently perceived as symbols of individual taste and social image. With the advancement of digitalization and intelligent technologies, modern Crossover SUVs have evolved into “third living spaces,” where intelligent cockpits and connected entertainment systems transform vehicles into mobile entertainment lounges or temporary workspaces, enriching everyday usage experiences. Aspects such as driving range, levels of intelligence, spatial comfort, safety, brand reputation and after‑sales service have become core considerations in consumer decision‑making beyond price and basic performance, reflecting an integrated consumption trend that further stimulates demand for Crossover SUVs in the personal use market. Official statistics show that passenger vehicles, including SUVs, continue to grow in domestic markets and that the penetration rate of new energy vehicles in the passenger vehicle segment has been increasing, indicating stronger acceptance among personal users for new energy and intelligent Crossover SUVs.

b) Commercial Use

In the commercial use domain, Crossover SUVs, though smaller in scale compared with the personal consumption market, also demonstrate stable and specific demand within certain commercial scenarios. Some enterprises choose mid�size or luxury Crossover SUVs as official business vehicles and executive transport, leveraging these models’ combination of comfortable ride quality, strong brand reputation and higher safety configurations to support official activities, business receptions and cross�regional travel, thereby meeting practical needs related to daily operations and corporate image presentation. Crossover SUVs are also included in vehicle procurement plans for rental companies and mobility service platforms, where they are used for short�term and long�term rentals as well as premium ride�hailing services; in such applications, the vehicles’ spatial performance, ride comfort and operational economics help enhance user experience and improve operational efficiency. Furthermore, in specialized industry scenarios such as engineering inspections and medical support where a certain degree of load capacity and spatial adaptability are required, Crossover SUVs serve as functional utility vehicles. It is worth noting that as the penetration rate of new energy vehicles in the passenger car market continues to rise — with new energy passenger vehicles accounting for a significant proportion of overall sales — the applicability of new energy vehicles in both commercial and personal segments has increased, indirectly promoting broader use of new energy Crossover SUVs in commercial settings to meet enterprises’ demands for greener mobility and cost control.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Crossover SUVs market is segmented as below:

By Company

BMW

Audi

Subaru

Mitsubishi

Kia

General Motors

Polestar

Honda

Chevrolet

Ford

Mazda

Infiniti

Toyota

Nissan

Hyundai

Nio

SAIC Volkswagen

Segment by Type

Full-Size SUVs

Med-Size SUVs

Compact-Size SUVs

Segment by Application

Personal Use

Commercial Use

Each chapter of the report provides detailed information for readers to further understand the Crossover SUVs market:

Chapter 1: Introduces the report scope of the Crossover SUVs report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Crossover SUVs manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Crossover SUVs market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

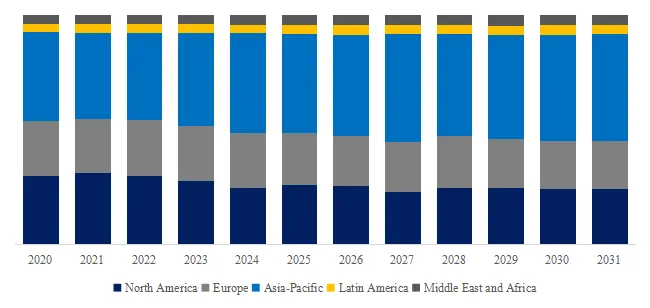

Chapter 5: Sales, revenue of Crossover SUVs in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Crossover SUVs in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Crossover SUVs competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Crossover SUVs comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Crossover SUVs market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Crossover SUVs Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Crossover SUVs Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Crossover SUVs Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp