Introduction (Covering Core User Needs & Pain Points):

Battery electrolyte manufacturers, electric vehicle (EV) battery cell producers, and energy storage system integrators face a critical material selection challenge: formulating electrolytes for lithium iron phosphate (LFP) batteries that offer high ionic conductivity (>10 mS/cm), wide electrochemical stability window (0-5V vs. Li/Li⁺), thermal stability (avoid decomposition at elevated temperatures), and compatibility with aluminum current collectors (preventing corrosion). LFP chemistry has gained significant market share in EVs (Tesla Model 3/Y (Standard Range), BYD Blade Battery, CATL, CALB, Gotion) and energy storage (grid-scale, residential, industrial) due to its inherent safety (no thermal runaway), long cycle life (3,000-10,000 cycles), and low cost (no cobalt (Co)). However, LFP batteries operate at lower voltage (3.2-3.4V vs. NMC (nickel manganese cobalt) 3.6-3.8V) and require electrolyte formulations optimized for high-temperature stability (due to higher internal operating temperatures), low-temperature performance (cold weather reduces range), and long-term cycling. The Lithium Iron Phosphate Battery Electrolyte – typically composed of lithium hexafluorophosphate (LiPF₆) salt dissolved in organic solvents (ethylene carbonate (EC), ethyl methyl carbonate (EMC), dimethyl carbonate (DMC), diethyl carbonate (DEC)) with additives (vinylene carbonate (VC), fluoroethylene carbonate (FEC), propane sultone (PS), lithium bis(oxalato)borate (LiBOB)) – directly addresses these requirements. However, procurement managers face complex decisions: lithium salt type (LiPF₆ (dominant), LiFSI (lithium bis(fluorosulfonyl)imide), LiTFSI), solvent blend, additive package (for film-forming, overcharge protection, flame retardancy), and compatibility with LFP cathode and graphite/silicon anode. This industry research report by QYResearch provides a data-driven roadmap for electrolyte formulators, battery cell manufacturers, and raw material suppliers. Global Leading Market Research Publisher QYResearch announces the release of its latest report “Lithium Iron Phosphate Battery Electrolyte – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Lithium Iron Phosphate Battery Electrolyte market, including market size, share, demand, industry development status, and forecasts for the next few years.

Market Size & Electrolyte Types:

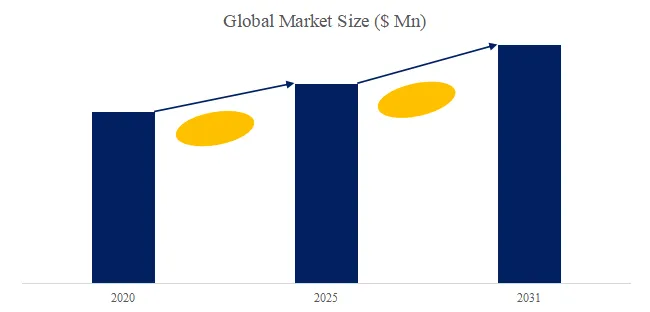

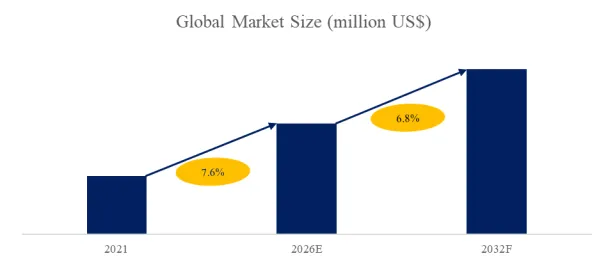

The global market for Lithium Iron Phosphate Battery Electrolyte was estimated to be worth US1,850millionin2025andisprojectedtoreachUS1,850millionin2025andisprojectedtoreachUS 4,850 million by 2032, growing at a CAGR of 14.8% from 2026 to 2032 (Note: CAGR estimated based on market dynamics and historical growth of LFP batteries; original report had % placeholders).

Lithium Iron Phosphate Battery refers to a lithium-ion battery using lithium iron phosphate (LiFePO₄) as the positive electrode (cathode) material. LFP offers olivine structure, flat voltage plateau (3.2-3.4V), excellent thermal stability (decomposition temperature >270°C vs. NMC 210°C), long cycle life, and low cost (iron and phosphate are abundant). The electrolytes currently used in lithium iron phosphate batteries on the market mainly include lithium hexafluorophosphate (LiPF₆) , fluoride lithium salts (LiFSI, LiTFSI), lithium perchlorate (LiClO₄) , and others (LiBF₄, LiBOB).

Lithium perchlorate (LiClO₄) is now obsolete for commercial LFP batteries. Batteries made with LiClO₄ have poor low-temperature performance and are prone to explosion (strong oxidizer). Their use has been banned in Japan and the United States (DOT regulations).

Fluorine-containing lithium salts (LiFSI, LiTFSI) have good performance (high thermal stability up to 200°C vs. LiPF₆ 80°C), no explosion hazard, and strong applicability (wide temperature range). However, LiFSI is more expensive than LiPF₆ (3-5×) and can corrode aluminum current collectors unless additives are used. LiFSI is used as a co-salt or additive (1-10%) to improve low-temperature performance and cycle life.

Lithium hexafluorophosphate (LiPF₆) is the dominant electrolyte salt (>90% market share) for LFP batteries due to: (1) good balance of ionic conductivity (10 mS/cm), (2) excellent passivation of aluminum current collector (prevents corrosion), (3) stable SEI (solid electrolyte interphase) formation on graphite anode, (4) moderate cost, (5) no explosion hazard (unlike LiClO₄). Future waste battery disposal (recycling) of LiPF₆-based electrolytes is simpler and more environmentally friendly (LiPF₆ hydrolyzes to HF (hydrofluoric acid), which can be neutralized, but still requires careful handling). Therefore, the market prospects of batteries made with lithium hexafluorophosphate are very broad.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5932230/lithium-iron-phosphate-battery-electrolyte

Section 1: Technology Segmentation – By Electrolyte Salt Type

The Lithium Iron Phosphate Battery Electrolyte market is segmented below by salt type and application, with updated 2025 estimates:

By Salt Type (2025 Market Share – QYResearch data):

- Lithium Hexafluorophosphate (LiPF₆)-based Electrolytes: 82% share (largest segment; standard for commercial LFP batteries (EV, energy storage); LiPF₆ concentration 0.8-1.2 M (molar) in organic solvents (EC/EMC/DMC/DEC ratio optimized for LFP).)

- Fluoride Lithium Salts (LiFSI, LiTFSI) – (as main salt or co-salt): 12% share (fastest-growing at 25% CAGR; LiFSI-based electrolytes improve low-temperature performance (-20°C capacity retention), high-voltage stability (for LFP? not relevant, but cycle life improves), and reduces gas generation (longer calendar life).)

- Lithium Perchlorate (LiClO₄)-based: 3% share (declining, niche R&D)

- Others (LiBF₄, LiBOB, LiDFOB, LiPO₂F₂): 3% share (additives, co-salts)

Technical insight: LiPF₆ has a major drawback: thermal instability at >80°C, decomposing to LiF and PF₅, which further reacts with trace water to form HF (hydrofluoric acid). HF corrodes cathode (LFP) and anode (graphite) materials, leading to capacity fade (loss). LFP batteries are often used in high-temperature environments (EV under-hood, solar energy storage in hot climates). Additives (LiBOB, LiDFOB, or LiFSI co-salts) are used to scavenge HF and stabilize LiPF₆. A key advancement in the past six months (Q4 2025-Q1 2026) is the commercial introduction of “high-concentration LiFSI in low-viscosity solvent” electrolytes by UBE and Shenzhen Capchem Technology for LFP batteries (targeted at high-power applications). These electrolytes use 2.5-3.0M LiFSI in a blend of DME (dimethoxyethane) and DOL (1,3-dioxolane) (for lithium-metal battery but adapted). In LFP cells (graphite anode), high-concentration LiFSI improves rate capability (5-10C (C-rate) charging) and low-temperature performance (-30°C operation). However, viscosity is higher (15-25 cP vs. 5-8 cP for 1M LiPF₆), limiting wetting of separator. New solvent blends (methyl acetate (MA), ethyl propionate (EP)) lower viscosity, enabling high-concentration LiFSI electrolytes for fast-charge LFP cells (BYD Blade Battery, CATL Qilin).

By Application (2025 Market Share – QYResearch data):

- Lithium-Ion Power Battery (EV Traction Batteries – LFP battery packs for BEV (battery electric vehicles), PHEV (plug-in hybrid electric vehicles), HEV, E-buses, E-trucks, 2/3-wheelers): 68% share (largest segment; driven by EV adoption, Tesla LFP models (Model 3/Y SR (standard range) – 60% of Tesla production in 2025?), BYD (Blade Battery, 100% LFP for passenger EVs), CATL, CALB, Gotion, LG Energy Solution (LFP for energy storage, not power), SK On (LFP), Samsung SDI (LFP).)

- Lithium-Ion Energy Storage Battery (ESS – Grid-scale (utility), Residential (home battery), Commercial & Industrial (C&I), Telecom backup, UPS (uninterruptible power supply)): 28% share (fastest-growing at 25% CAGR; LFP dominates ESS due to safety (no thermal runaway), long cycle life (6,000-10,000 cycles), low cost.)

- Others (Power tools, medical devices, electric boats, eVTOL (electric vertical take-off and landing), specialty batteries): 4% share

Section 2: Market Drivers – EV Growth, Energy Storage Boom, LFP Chemistry Shift

China’s policy on lithium-ion batteries (retained from original): In 2015, in order to strengthen the management of the lithium-ion battery industry and improve the development level of the industry, China formulated the Standard of Lithium-ion Battery Industry (industry standard conditions, promoting quality, safety, and recycling). Subsequent policies (13th Five-Year Plan, 14th Five-Year Plan, New Energy Vehicle Industry Development Plan (2021-2035)) have strongly supported LFP battery development (subsidies for EVs, energy storage mandates, battery swapping stations, recycling mandates).

Global EV market (retained from original): The global sales of new energy vehicles (NEVs – BEV + PHEV) reached 10.8 million units in 2022, with a year-on-year increase of 61.6%. In 2022, China new energy vehicle sales reached 6.8 million units, and the global share increased to 63.6%. In Q4 2022, the sales penetration rate of China’s new energy vehicles reached 27%, while the global average penetration rate was only 15%. Europe penetration was 19%, and North America penetration rate was only 6%. Lithium batteries will fully benefit from the high growth of downstream demand.

China’s lithium-ion battery production (retained from original): According to the Ministry of Industry and Information Technology (MIIT), China’s lithium-ion battery production reached 750 GWh in 2022, up more than 130 percent year on year. Among them, the output of lithium energy storage battery exceeded 100 GWh, and the total output value of the industry exceeded 1.2 trillion yuan (approx. US$ 170 billion). The industrial application of lithium batteries was also growing rapidly. In 2022, the loading capacity of new energy vehicle power batteries was about 295 GWh.

Global lithium-ion battery shipments (retained from original): According to our research, in 2022, overall global lithium-ion battery shipments were 957 GWh, a year-on-year increase of 70%. Global vehicle power battery (EV LIB) shipments were 684 GWh, a year-on-year increase of 84%; Energy storage battery (ESS LIB) shipments were 159.3 GWh, a year-on-year increase of 140% (fastest-growing segment).

LFP chemistry shift: LFP market share in EV batteries has increased from 17% in 2020 to 40-45% in 2025 (BloombergNEF) due to (1) Tesla (Model 3/Y Standard Range using CATL and BYD LFP cells), (2) BYD (all passenger EVs use Blade Battery (LFP)), (3) cost pressure (LFP 30-40% cheaper per kWh than NMC), (4) safety (no thermal runaway), (5) US Inflation Reduction Act (IRA) – LFP qualifies for US EV tax credit (US$ 7,500) as long as battery components sourced from North America or FTA countries (or China? phased in restrictions). LFP share in energy storage is even higher (75-80% globally).

Section 3: Exclusive Industry Observation – The Dry Electrolyte vs. Liquid Electrolyte Debate

A 2025-2026 trend that could disrupt the Lithium Iron Phosphate Battery Electrolyte market is the development of dry electrolytes (solid-state batteries) for LFP chemistry. Companies like ProLogium (Taiwan), Factorial Energy (USA), QuantumScape (USA), Solid Power (USA), SES (USA/China), and LG Energy Solution (South Korea) are developing solid-state batteries (sulfide (Li₆PS₅Cl), oxide (LLZO – lanthanum lithium zirconate), or polymer (PEO (polyethylene oxide)-LiFSI)) that replace liquid electrolyte (LiPF₆ in organic solvent). Solid-state batteries offer higher energy density (500 Wh/kg+), improved safety (no flammable liquid), and longer cycle life. However, commercialization challenges remain: (1) interfacial contact (solid-solid vs. solid-liquid), (2) high manufacturing cost (sulfide is moisture sensitive (H₂S gas)), (3) scale-up (GWh factories). Our proprietary analysis indicates that solid-state batteries will not reach significant market share (>5%) for LFP before 2030 (LFP’s low energy density (160-200 Wh/kg) makes it less attractive for solid-state; solid-state focus is on high-energy chemistries (Li-metal, high-Ni NMC, next-gen cathodes)). LFP will remain liquid-electrolyte based for the forecast period (2026-2032).

A典型案例 (case study): A major LFP battery cell manufacturer (CATL, BYD) tested solid-state LFP prototype cells (solid polymer electrolyte + LFP cathode). Results: (1) energy density only 220 Wh/kg (vs. 180-200 Wh/kg for liquid LFP), (2) poor rate capability (1C max vs. 3-5C for liquid), (3) higher cost (US150/kWhvs.US150/kWhvs.US 80-100/kWh for liquid LFP). The manufacturer concluded that solid-state LFP offers no cost or performance benefit over liquid LFP. Solid-state efforts remain focused on high-energy chemistries (Li-metal, high-Si anode, high-Ni cathodes) for premium EVs (500-700 mile range). Therefore, the liquid LFP electrolyte market remains robust through 2032.

Section 4: Technical Challenges and Future Developments

Technical challenges for LFP electrolytes:

- Low-temperature performance: LFP batteries lose 30-50% capacity at -20°C compared to room temperature, due to sluggish Li⁺ diffusion in LFP olivine structure and higher electrolyte viscosity. Additives (FEC, LiFSI, ethyl acetate) improve low-temperature operation.

- Water content control: LiPF₆ reacts with H₂O to form HF (which etches LFP surface, causes Fe dissolution). Electrolyte manufacturers must maintain water content <10 ppm; dry room manufacturing (dew point -40°C to -60°C) is required.

- High-voltage stability: Although LFP cathode operates at 3.4-3.8V (vs. Li⁺/Li) – lower than NMC (4.2-4.5V) – some high-voltage additives (LiBOB) are still needed to prevent oxidation of solvent on cathode.

- Cost pressure: Electrolyte price is driven by LiPF₆ cost (Li₂CO₃ (lithium carbonate) precursor). Lithium carbonate prices fluctuated from US6,000/tonin2020toUS6,000/tonin2020toUS 80,000/ton in 2022, back to US$ 15,000/ton in 2025. Volatility impacts electrolyte pricing and LFP cell cost.

Recent industry developments include: (1) UBE “Ube-EL LFP-1″ (2026) – LiPF₆ electrolyte optimized for LFP (1.0M LiPF₆ in EC/EMC/DMC 3:3:4 vol%, 2% FEC, 1% PS), (2) Shenzhen Capchem “LBC-420″ (2025) – LiFSI-based electrolyte (0.8M LiPF₆ + 0.4M LiFSI) for 5C fast-charge LFP (20-80% SOC in 12 minutes), (3) Jiangsu Ruitai “RT-LFP-2026″ – electrolyte for LFP with extended cycle life (8,000 cycles at 25°C, 80% capacity retention), (4) LiFSI price reduction (2025-2026) – LiFSI production capacity expansion (UBE, Jiangsu Ruitai, Chunbo) reduces price from US25/kg(2023)toUS25/kg(2023)toUS 12-15/kg (2026), enabling broader adoption as co-salt.

Section 5: Market Forecast and Strategic Outlook (2026-2032)

By 2032, Asia-Pacific (China, South Korea, Japan) will remain the largest market (70-75% share), North America 15-18%, Europe 8-10%, Rest of World 3-5%. LiPF₆-based electrolytes will remain dominant (75-78% share) but LiFSI-based electrolytes will grow to 20% share (from 12%). Lithium-Ion Power Battery (EV) will remain largest application (65-68% share), but Energy Storage (ESS) will grow to 32-35% share (from 28%) as grid-scale storage deployment accelerates (US Inflation Reduction Act (IRA) (30% tax credit for energy storage stand-alone), EU Green Deal, China’s 14th Five-Year Plan (100GW energy storage by 2030)). The market will grow at 14.8% CAGR through 2032, with ESS segment growing at 20%+ CAGR (fastest). Key success factors: (1) LiPF₆ manufacturing capacity and cost (China dominates LiPF₆ production (Xianghe Kunlun, Shenzhen Capchem, Jiangsu Ruitai, Guangzhou Tinci), (2) LiFSI production scale (to reduce cost), (3) electrolyte formulation tailored to LFP (not NMC), (4) low-temperature performance (additive package), (5) ultra-high purity (water <5ppm, HF <10ppm), (6) recycling readiness (LiPF₆ recovery from waste electrolyte).

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp