QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “PVA Film for Polarizer- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global PVA Film for Polarizer market, including market size, share, demand, industry development status, and forecasts for the next few years.

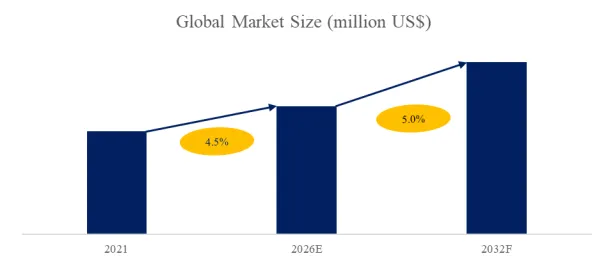

The global market for PVA Film for Polarizer was estimated to be worth US$ 2152 million in 2024 and is forecast to a readjusted size of US$ 3155 million by 2031 with a CAGR of 5.7% during the forecast period 2025-2031.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/3854923/pva-film-for-polarizer

PVA Film for Polarizers Market Summary

PVA film for polarizers is one of the core raw materials used in polarizers. It is made from polyvinyl alcohol, or PVA, through processes such as stretching, dyeing, and lamination. The film selectively absorbs light waves traveling in a specific direction, enabling optical polarization. In products such as liquid crystal displays, touch panels, optical instruments, and sunglasses, PVA polarizing film serves as the key functional layer of the polarizer.

The production process of PVA film generally includes extrusion or casting of PVA film, directional stretching, dyeing treatment, and lamination with protective films. Stretching aligns the PVA molecular chains in a specific direction and gives the film its polarizing function. Dyeing is typically carried out with iodine or other colorants so that the film can absorb light polarized in a specific direction. Lamination with protective films enhances mechanical strength, moisture resistance, and durability.

The performance indicators of PVA film for polarizers are critical and include transmittance, polarization efficiency, thickness uniformity, moisture resistance, and thermal stability. High-quality polarizing film can significantly improve display brightness, contrast, and viewing angle, while also ensuring long-term stability during use. With the development of liquid crystal displays, OLED screens, wearable devices, and automotive displays, demand for high-performance PVA film continues to grow, making it an indispensable material in the display panel value chain.

Industry Overview

PVA optical film is the core membrane material of polarizers, which are key materials in liquid crystal displays. Polarizers are composed of multiple film layers, and raw materials account for 80% of total production cost. The main raw materials include TAC film, optical-grade PVA film, pressure-sensitive adhesive, protective film, and release film. Among them, TAC film accounts for around 50% of cost, optical-grade PVA film accounts for 12%, adhesive accounts for 5% to 10%, protective film and release film account for 15%, chemical materials account for 5%, and other costs account for 10%. Due to the high technical barriers of PVA optical film, the global market has long been dominated by Japanese companies. Kuraray accounts for more than 64% of global capacity and Mitsubishi Chemical Corporation accounts for 28%, with the two companies together holding the vast majority of the global market. At the same time, Kuraray also holds a leading position in the PVA raw material segment used for film production. In China, only Wanwei High-Tech, Chang Chun Group in Taiwan, China, and Sinopec Chongqing SVW Chemical Co., Ltd. currently have some supply capability, mainly providing small volumes of narrow-width film for the mid- to low-end market, with a combined market share of less than 9%. Overall, the number of companies worldwide capable of stable supply remains very limited.

As global liquid crystal display capacity continues to shift to China, competition in the domestic polarizer market has become increasingly intense. Downstream manufacturers are placing stricter requirements on cost control, and demand for localization of upstream raw materials is becoming more urgent. In this context, the importance of localized supply capability for PVA optical film, as a key raw material, continues to rise. Based on interviews and industry information, consumption of PVA optical film for polarizers in China reached about 200 million square meters in 2025. Given that Kuraray and Mitsubishi Chemical Corporation together held more than 93% of the China market, and based on interview-based estimates covering five companies, the average market price in China in 2025 was about RMB 21 per square meter, corresponding to a China market size of about RMB 4.2 billion.

Table 1. China PVA Film for Polarizers Top 5 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

| Company | Market Share |

| Kuraray | 66.18% |

| Mitsubishi Chemical Corporation | 26.92% |

| Chang Chun Group | 3.51% |

| Anhui Wanwei Updated High—Tech Material Industry Co.,Ltd | 1.81% |

| Sinopec Chongqing SVW Chemical Co., Ltd. | 1.58% |

Above data is based on report from QYResearch: China PVA Film for Polarizers Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

According to QYResearch, the main producers of PVA film for polarizers in the China market include Kuraray, Mitsubishi Chemical Corporation, Chang Chun Group, Sinopec Chongqing SVW Chemical Co., Ltd., and Anhui Wanwei Updated High—Tech Material Industry Co.,Ltd At present, only these five companies have stable commercial supply capability, and the overall global market structure is broadly similar. Among them, Kuraray and Mitsubishi Chemical Corporation together account for 93.10% of market share, indicating a highly concentrated market.

1. Kuraray

Product link: https://www.kuraray.com/global-en/products/poval-film/

Since commercializing PVA film in 1961, Kuraray has continued to deepen its presence in this product field. In addition to applications in optical films such as polarizers for liquid crystal displays, its products are also widely used in transparent garment packaging films and water-soluble films. Kuraray’s PVA film for polarizers is produced in Japan. The company currently has capacity of 296 million square meters and plans to add another 38 million square meters, which is expected to come on stream in 2027. Total capacity will then increase to 334 million square meters. More than 55% of the company’s revenue from this product comes from the China market, and the average selling price is above RMB 20 per square meter.

2. Mitsubishi Chemical Corporation

Product link: https://www.m-chemical.co.jp/en/products/departments/mcc/acetyl/product/1205877_9064.html

Mitsubishi Chemical Corporation’s PVA film for polarizers is marketed under the trade name OPLFILM and is a PVOH film used in polarizers for liquid crystal displays. The company’s production base is located in Japan, with existing capacity of 127 million square meters. It also plans to add 27 million square meters of new capacity, which is expected to come on stream in 2027, bringing total capacity to 154 million square meters. About 52% of the company’s business for this product comes from the China market, and the average selling price is above RMB 20 per square meter.

3. Chang Chun Group

Product link: https://ccpgp.com/cn/News_Prt_Content/2538/79262/

Chang Chun Group produces PVA film for polarizers in Taiwan, China, with existing capacity of 18 million square meters. More than 65% of the company’s sales of this product are generated in mainland China, which is one of its core downstream markets. The average selling price is above RMB 15 per square meter, and the company has certain competitiveness in the mid- to high-end segment of the PVA film for polarizers market.

4. Anhui Wanwei Updated High—Tech Material Industry Co.,Ltd

Product link: https://www.wwgf.com.cn/hxcp3166/info.aspx?itemid=12239

Anhui Wanwei Updated High—Tech Material Industry Co.,Ltd is one of China’s local suppliers of PVA film for polarizers. The company currently has capacity of 12 million square meters, with an additional 20 million square meters under construction. In 2025, the average selling price of its products was above RMB 11 per square meter. In addition to the domestic market, the company also exports to Taiwan, China, with major customers including BenQ Materials and CMMT. In 2025, export revenue from PVA film for polarizers was approximately RMB 15 million to RMB 20 million.

5. Chongqing SVW Chemical Co., Ltd.

Chongqing SVW Chemical Co., Ltd., a subsidiary of Sinopec Group, is an important new entrant in China’s PVA film for polarizers market. The company currently has capacity of 8 million square meters. It began small-batch supply in 2023 and entered the large-scale supply stage in 2025, with shipments of about 6 million square meters that year. Major customers include Sanlipu, and the average selling price is above RMB 14 per square meter. The company is currently building a second production line, and total capacity is expected to reach 16 million square meters after completion.

6. Chongqing Spectrum New Materials

Chongqing Spectrum New Materials is a new project entrant in China’s PVA film for polarizers market. The company has planned capacity of 7 million square meters and is currently under construction. As the project moves toward completion and production, the company is expected to become an emerging supplier in the domestic market.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The PVA Film for Polarizer market is segmented as below:

By Company

Kuraray

Samsung SDI

Mitsubishi Chemical

YS America

Nitto

Anhui Wanwei Group

Sinopec Chongqing SVW Chemical

Sichuan Longhua Film

Changchun Group

Segment by Type

Anti-glare Treatment (AG)

Anti-glare + Low-reflective Treatment (AG + LR)

CHC + LR Treatment

CHC Treatment

Anti-glare Treatment

Other

Segment by Application

Display Panel

Sunglasses

Photography Equipment

Watch

Other

Each chapter of the report provides detailed information for readers to further understand the PVA Film for Polarizer market:

Chapter 1: Introduces the report scope of the PVA Film for Polarizer report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of PVA Film for Polarizer manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various PVA Film for Polarizer market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of PVA Film for Polarizer in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of PVA Film for Polarizer in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth PVA Film for Polarizer competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides PVA Film for Polarizer comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides PVA Film for Polarizer market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global PVA Film for Polarizer Market Outlook, In‑Depth Analysis & Forecast to 2031

Global PVA Film for Polarizer Sales Market Report, Competitive Analysis and Regional Opportunities 2025-2031

Global PVA Film for Polarizer Market Research Report 2025

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp