Introduction: Solving Seasonal Storage and Multi-Day Grid Backup Limitations of Battery Energy Storage

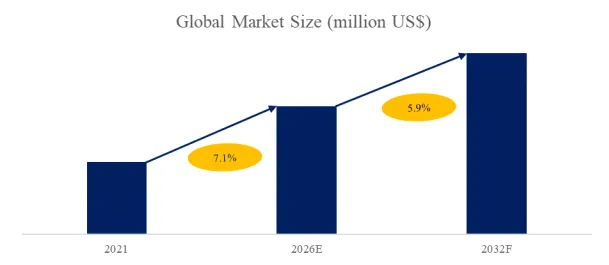

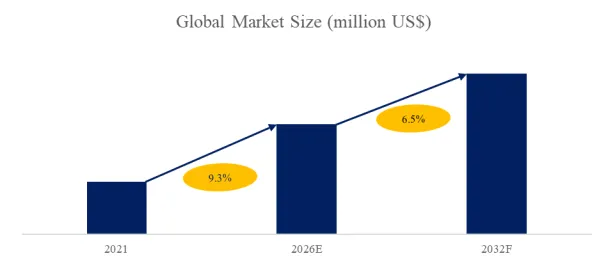

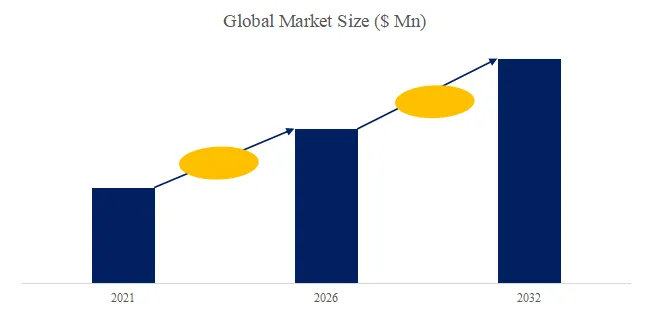

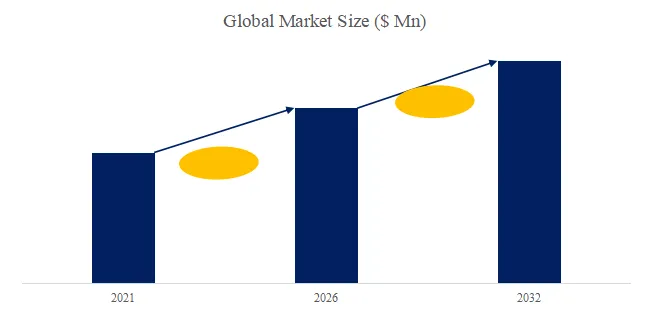

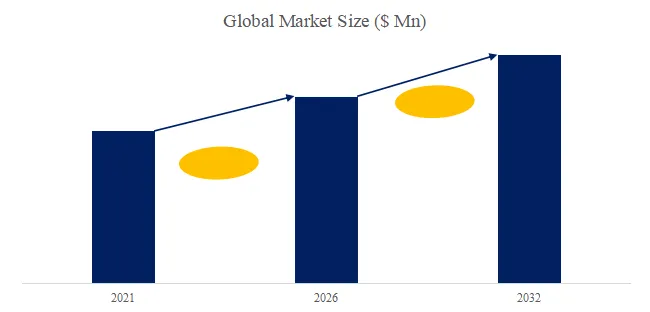

For utility grid operators, renewable energy developers, and industrial energy managers, lithium-ion batteries have become the default solution for short-duration energy storage (4–8 hours). However, batteries face fundamental economic and technical limitations for long-duration storage (24–100+ hours), seasonal storage (weeks to months), and multi-day grid backup following extended periods of low wind and solar irradiation (dunkelflaute—”dark doldrums” in German, periods with little wind and solar). Energy Storage With Hydrogen Conversion addresses these gaps through a power-to-gas-to-power (P2G2P) process: (1) electrolysis of water (using surplus renewable electricity, typically from solar or wind) to produce hydrogen (green hydrogen), (2) storage of hydrogen in gaseous (compressed), liquid (cryogenic), or solid-state (metal hydrides) form, and (3) conversion of stored hydrogen back into electrical energy via fuel cells (PEM, solid oxide, phosphoric acid) or hydrogen combustion turbines (gas turbines or reciprocating engines). This technology is a new type of energy storage and conversion method specifically designed to solve the high volatility and intermittency of renewable energy (solar, wind, tidal, run-of-river hydro), enabling deep decarbonization of electricity grids (50–100% renewable penetration) and providing backup power for critical infrastructure (hospitals, data centers, telecom, military bases) with durations measured in days, not hours. Global Leading Market Research Publisher QYResearch announces the release of its latest report *“Energy Storage With Hydrogen Conversion – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”*. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Energy Storage With Hydrogen Conversion market, including market size, share, demand, industry development status, and forecasts for the next few years. The global market for Energy Storage With Hydrogen Conversion was estimated to be worth US850millionin2025andisprojectedtoreachUS850millionin2025andisprojectedtoreachUS 12.5 billion by 2032, growing at a compound annual growth rate (CAGR) of 47.5% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5932280/energy-storage-with-hydrogen-conversion

Market Segmentation by Storage Phase: Gaseous, Liquid, and Solid-State

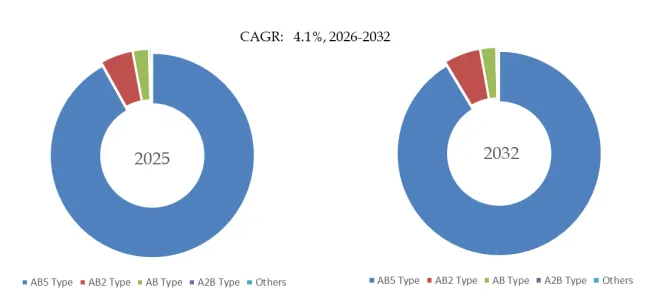

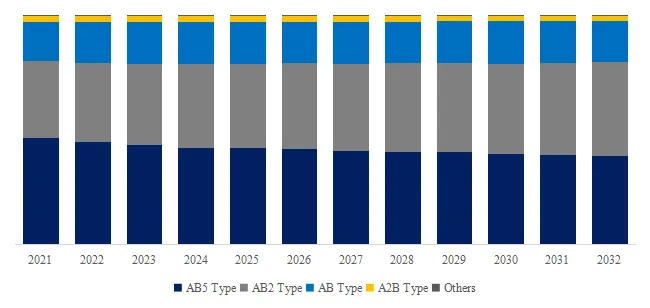

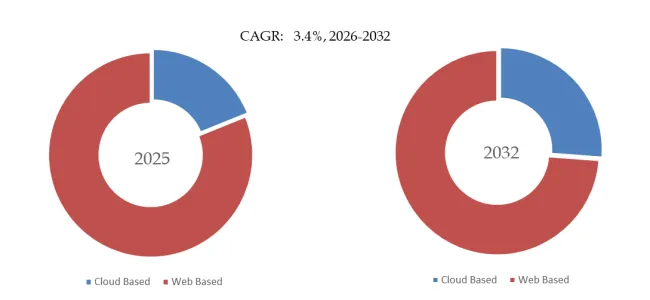

The Energy Storage With Hydrogen Conversion market is segmented by hydrogen storage method. Gaseous hydrogen storage (compressed H₂ at 350–700 bar in Type I-IV pressure vessels) currently dominates market share, accounting for approximately 68% of global revenue in 2025. Gaseous storage is the most mature and lowest-cost method for large-scale, long-duration energy storage (10 MWh to GWh scale). Storage tanks are installed above ground (steel pressure vessels) or underground (salt caverns, depleted natural gas reservoirs, aquifers). Above-ground cost: US300–600perkgH2(for350–700barTypeIVcompositetanks).Undergroundsaltcaverncost:US300–600perkgH2(for350–700barTypeIVcompositetanks).Undergroundsaltcaverncost:US 25–50 per kg H₂ (very low, but limited to locations with suitable geology). Gaseous storage used in utility-scale projects (e.g., Hybrit (Sweden), NREL (US), ENTSO-E (European hydrogen backbone).

Liquid hydrogen storage (cryogenic, -253°C at 1 bar) holds 20% market share, used for large-scale, long-duration storage with high volumetric density (70 kg/m³ vs. 40 kg/m³ for 700 bar gaseous). Liquefaction requires 30–35% of stored energy (energy penalty) and has boil-off losses (0.1–1% per day, lower for large tanks >50,000 m³ (0.05–0.1% per day)). Liquid storage is used for hydrogen export/import (shipping, trucks) and large-scale grid storage in Europe (Germany, Netherlands, UK). Cost: US$ 1,000–2,000 per kg H₂ storage (including liquefaction equipment). Liquid hydrogen segment growing at 50% CAGR.

Solid-state hydrogen storage (metal hydrides: MgH₂, TiFe, LaNi₅; chemical hydrides; carbon-based materials) holds 12% market share, used in small-scale stationary storage (<1 MWh, 1–100 kg H₂) and microgrid applications. Solid-state storage operates at low pressure (10–50 bar), has high volumetric density (100–150 kg/m³), but high cost (US$ 2,000–10,000 per kg H₂) and slow refueling (requires heat to release hydrogen (endothermic desorption). Emerging for residential and commercial energy storage (LAVO System (Australia, metal hydride for home storage), H2GO Power (UK, metal hydride for remote sensing)).

Market Segmentation by Application: Industrial, Commercial, Utilities, and Others

The Energy Storage With Hydrogen Conversion market serves four primary application segments:

- Utilities (45% of demand): Largest and fastest-growing segment (55% CAGR). Utility-scale hydrogen storage (100 MWh–1 GWh+) used for grid services: (i) long-duration storage (24–100+ hours) for renewable firming (solar, wind), (ii) seasonal storage (summer solar to winter heating, spring wind to summer peak), (iii) transmission and distribution (T&D) deferral, (iv) black start capability, (v) grid inertia and synthetic inertia (frequency response). Projects: Hybrit (Sweden, 800 MWh hydrogen storage with cavern for steel plant), NREL Wind2H2 (US), ENTSO-E Hydrogen Backbone (European transmission system operators plan 6,800 km hydrogen pipeline by 2030). Utilities install electrolyzers (20–200 MW), hydrogen storage (salt cavern or tanks), and fuel cells/ gas turbines (combined cycle or open cycle).

- Commercial (28%): Commercial and industrial (C&I) microgrids, data centers (backup power with multi-day runtime, replacing diesel generators), hospitals (emergency power, uninterruptible power supply (UPS)), telecom towers (off-grid and backup power), and remote commercial facilities (mines, resorts, camps). Commercial applications prioritize reliability (no grid, no diesel), emissions reduction (zero onsite), and long storage duration (3–7 days). Systems: 100 kW–10 MW electrolyzer, 1–10 MWh storage, 100 kW–10 MW fuel cell. Examples: Microsoft data center (Ireland, hydrogen fuel cell backup for 48-hour runtime), LAVO residential storage (Australia, 2–3 days backup).

- Industrial (18%): Industrial energy storage for captive power (island mode), peak shaving (avoid demand charges), and emergency backup (critical manufacturing). Industrial segment also includes power-to-gas (P2G) for hydrogen injection into natural gas networks (up to 5–20% blend by volume without infrastructure changes). Industrial users include steel (hydrogen for direct reduction of iron (DRI)), ammonia (hydrogen for fertilizer), refining (hydrocracking, desulfurization), chemicals (methanol, polymers). Energy storage integration allows co-location of electrolysis (use surplus renewable electricity) and hydrogen storage (buffer for process variations). Segment growing at 40% CAGR.

- Others (9%): Including residential (home energy storage (LAVO System), backup power, solar self-consumption), transportation (hydrogen refueling stations with on-site electrolysis and storage), military (forward operating bases (FOBs) with hydrogen storage for silent watch and extended missions), and remote sensing (meteorological stations, ocean buoys, seismic monitoring, space applications). Residential segment growing at 65% CAGR (from small base) as hydrogen storage becomes cost-competitive with batteries (LiFePO₄, lead-acid) for multi-day backup (3+ days autonomy).

Technical Deep Dive: Power-to-Gas-to-Power Process, Round-Trip Efficiency, and Economics

Electrolysis Technologies :

- Alkaline electrolysis (AEL) : Mature (50+ years), low cost (US$ 600–1,000/kW), efficiency 50–70% (50–60 kWh/kg H₂, lower heating value (LHV) of hydrogen is 33.3 kWh/kg). Suitable for utility-scale (MW to GW). Response time minutes (slower than PEM). Stack lifetime 60,000–100,000 hours.

- Proton exchange membrane (PEM) electrolysis : Fast response (seconds), efficiency 60–75% (45–55 kWh/kg H₂), cost US$ 1,000–1,500/kW, stack lifetime 40,000–80,000 hours. Ideal for direct coupling with variable renewables (solar, wind). Market share 30% (growing).

- Solid oxide electrolysis (SOEC) : High efficiency 85–100% (35–40 kWh/kg H₂) using high-temperature steam (800–1,000°C) from waste heat or nuclear. Cost US$ 2,000–3,000/kW (pre-commercial). Long-term potential for industrial co-location (steel, cement, chemical plants).

Hydrogen Storage (Gaseous, 350–700 bar) :

- Energy density: 1.3 kWh/L (350 bar), 1.8 kWh/L (700 bar) — compare to LiFePO₄ battery 0.4–0.7 kWh/L (cell only). Hydrogen lower volumetric density but much higher specific energy (33 kWh/kg vs. 0.25 kWh/kg for battery). For stationary storage, volume less critical; weight irrelevant.

- Storage cost per kWh: US10–20/kWh(gaseous,700bar,TypeIVtanks),US10–20/kWh(gaseous,700bar,TypeIVtanks),US 1–5/kWh (salt cavern). Battery: US100–300/kWh.Hydrogenstorageis5–50×cheaperthanbatteriesforlong−duration(>24hours)becausetankcostperkWhfallsasdurationincreases(energycapacitydecoupledfrompowerrating).For100−hourstorage:batterywouldrequire100×morecells(samepower,but100×energy)→costlinearwithduration.Hydrogenstorage:sametankvolumefor100−hourvs.20−hour(ifsamepowerrating),onlyincrementalcostofadditionalhydrogen(electrolysisenergy,100–300/kWh.Hydrogenstorageis5–50×cheaperthanbatteriesforlong−duration(>24hours)becausetankcostperkWhfallsasdurationincreases(energycapacitydecoupledfrompowerrating).For100−hourstorage:batterywouldrequire100×morecells(samepower,but100×energy)→costlinearwithduration.Hydrogenstorage:sametankvolumefor100−hourvs.20−hour(ifsamepowerrating),onlyincrementalcostofadditionalhydrogen(electrolysisenergy,5–10/kg H₂ (US$ 0.15–0.30/kWh)).

Fuel Cell Technologies :

- PEM fuel cell : Efficiency 50–60% (electrical), 85-90% with heat recovery (CHP). Fast start-up (minutes), modular (kW to MW). Cost US400–1,000/kW(2025),targetUS400–1,000/kW(2025),targetUS 80/kW (2030). Lifetime 20,000–40,000 hours.

- Solid oxide fuel cell (SOFC) : High efficiency (60–70% electrical, 85-90% CHP), operates at high temperature (600–1,000°C), slow start-up (hours), cost US$ 2,000–3,000/kW, lifetime 40,000–80,000 hours (degradation low). Suitable for continuous (baseload) operation.

- Hydrogen combustion turbine : Modified gas turbine (GE, Siemens, Mitsubishi Power) burning 100% hydrogen (or H₂ + natural gas blend). Efficiency 35–45% (simple cycle), 55–60% (combined cycle). Lower efficiency than fuel cell, but higher power density (MW to 100s MW) and lower cost (US$ 400–800/kW). Hydrogen turbines are commercial for power generation (planned projects 2025–2030).

Round-trip efficiency (electricity → H₂ → electricity) :

- Alkaline electrolysis (60%) + compression (90%) + PEM fuel cell (55%) = 30% round-trip (storage only)

- PEM electrolysis (70%) + compression (90%) + PEM fuel cell (55%) = 35% round-trip

- SOEC (85%) + no compression (if used at high pressure steam? SOEC operates at 1–30 bar, may require compression for storage) + SOFC (65%) = 55% round-trip (best case, lab-scale).

- Battery: 85–95% round-trip. Low efficiency of P2G2P is acceptable for long-duration storage (weeks/months) where surplus renewable energy is otherwise curtailed (zero marginal cost). Short-duration cycling (daily) not economical—use battery.

Levelized cost of storage (LCOS) for hydrogen storage (gaseous, 350 bar, 100-hour duration): US0.05–0.10/kWh(2040projection,DOE),US0.05–0.10/kWh(2040projection,DOE),US 0.15–0.25/kWh (2025). Battery LCOS for 4-hour: US0.10–0.15/kWh,for100−hour:>US0.10–0.15/kWh,for100−hour:>US 1.00/kWh (not economic). Hydrogen wins for duration > 24 hours.

User Case Study: Wind-Hydrogen Energy Storage Project (Germany)

A 100 MW onshore wind farm in Schleswig-Holstein, Germany (high wind resource, average capacity factor 35%, but intermittent, with periods of high wind (storm) when grid congested and wind power curtailed) integrated an Energy Storage With Hydrogen Conversion system (PEM electrolysis (10 MW), gaseous hydrogen storage (6,000 kg H₂ at 350 bar, 200 MWh electrical equivalent), and a 5 MW PEM fuel cell). Project commissioned Q2 2025 by regional utility (Stadtwerke Flensburg) and hydrogen specialist (H-TEC SYSTEMS (now PEM electrolysis, part of MAN Energy Solutions)). Key outcomes:

- Electrolysis capacity: 10 MW (PEM, 4 stacks × 2.5 MW, 70% efficiency, 52 kWh/kg H₂)

- Hydrogen production: 45 kg H₂/hour (full load), 390 metric tons/year (assuming 8,760 hours/year but limited by surplus wind availability). Stored 6,000 kg H₂ (200 MWh) after 140 hours of electrolysis (spread over 3–4 weeks).

- Fuel cell output: 5 MW electrical (PEM, 55% efficiency), continuous discharge for 38 hours (from full storage), or 2 MW for 95 hours, etc.

- Round-trip efficiency: 35% (grid to grid, measured over 9 months). Higher than utility target (30%), lower than battery (88%). Acceptable because only hydrogen used when wind curtailed (zero marginal cost electricity).

- Cost: electrolyzer US12million(US12million(US 1,200/kW), storage (6,000 kg, 350 bar Type IV tanks, 2.5 m³ each, 10 tanks) US2.5million(US2.5million(US 400/kg H₂), fuel cell US3.5million(US3.5million(US 700/kW), balance of plant (compressor, chiller, controls, grid connection) US4million,totalUS4million,totalUS 22 million. Battery with same energy (200 MWh) would cost US$ 30–40 million + replacement every 10–15 years.

- CO₂ reduction: 15,000 tons CO₂/year (displacing natural gas and reducing curtailment). Hydrogen is green (certified via guarantee of origin).

- Revenue: grid services (frequency regulation (primary, secondary, tertiary), voltage support, black start preparation). Wind farm owner avoids curtailment (lost revenue) by converting curtailed wind to hydrogen. Hydrogen also sold (for mobility, industry, grid injection) at €6–8/kg (US$ 6.50–8.70/kg) covering operating cost, but not capital.

Project qualifies for German government funding (National Hydrogen Strategy, IPCEI (Important Project of Common European Interest) funding). Phase 2 (2026–2027): add 20 MW electrolysis, 20,000 kg H₂ storage (600 MWh, salt cavern nearby), and 10 MW fuel cell (or hydrogen gas turbine (Siemens SGT-800, 62 MW, 100% H₂ ready). Commercial operation by 2028.

Competitive Landscape and Regional Dynamics

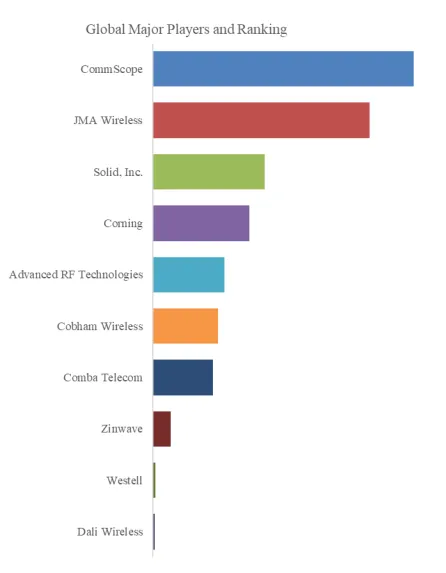

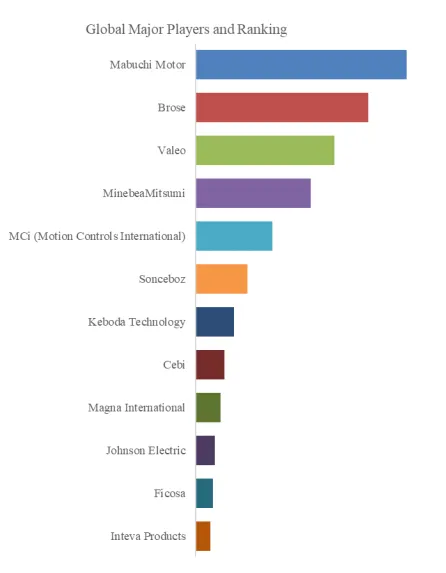

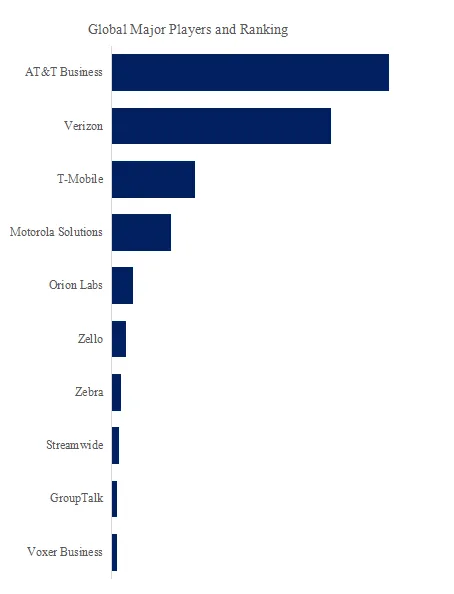

Electrolysis manufacturers: ITM Power (UK, PEM), Hydrogenics (Canada, now Cummins), Nel Hydrogen (Norway, alkaline, PEM), Longi (China, alkaline), Mingyang (China, alkaline), Toshiba (Japan, alkaline, SOEC), Cummins (US, alkaline, PEM), Plug Power (US, PEM, integrated electrolysis + fuel cell + storage). Hydrogen storage equipment: Air Liquide (France), Linde (Germany, UK), Air Products (US), Chart Industries (US, cryogenic tanks), Hexagon Composites (Norway, Type IV composite cylinders), Worthington Industries (US, Type I-III cylinders), Faurecia (France, hydrogen storage systems), ILJIN Hysolus (Korea, Type IV), GKN (UK, metal hydride). Fuel cell manufacturers: FuelCell Energy (US, stationary fuel cells (PAFC, SOFC)), Plug Power (PEM, CHP), Hydrogenics (PEM), Bloom Energy (not listed, SOFC). Integrated hydrogen storage solutions (turnkey): LAVO System (Australia, metal hydride for residential/commercial), H2GO Power (UK, metal hydride for remote sensing), Home Power Solutions (Germany, home storage), HyTech Power (US, military). Industrial gas majors (Air Liquide, Linde, Air Products) offer full P2G2P systems (electrolysis, storage, fuel cells) for utility and industrial customers.

Geographic Distribution: Europe largest market (45% share), driven by EU Hydrogen Strategy (40 GW electrolyzers by 2030, 500 GW by 2050), national hydrogen strategies (Germany, France, Netherlands, Spain, Portugal, UK), and funding (IPCEI, Horizon Europe). Asia-Pacific (30% share) led by Japan (Basic Hydrogen Strategy, 3 million tons hydrogen by 2030), South Korea (Hydrogen Economy Roadmap, 15 GW fuel cells by 2040), China (hydrogen for industry, pilot energy storage projects, 2025 targets (50,000 fuel cell vehicles, 100 hydrogen refueling stations, but not aggressive on energy storage—focus on hydrogen production from renewables for industrial use (refineries, ammonia, methanol, steel). North America (20% share), US DOE Hydrogen Shot (target 1/kgH2by2031),IRA(InflationReductionAct,PTCforhydrogenproductionupto1/kgH2by2031),IRA(InflationReductionAct,PTCforhydrogenproductionupto3/kg), Long Duration Storage Shot (target 90% cost reduction by 2030). Rest of World (5%): Australia (Hydrogen Energy Supply Chain pilot (HESC) exporting hydrogen to Japan, Eavor-Loop geothermal + hydrogen storage), Middle East (green hydrogen production for export (Saudi Arabia NEOM), domestic energy storage.

Cost trends: Electrolysis capital cost expected to fall 60–70% by 2030 (US200–400/kW),fuelcellcosttofall70–80200–400/kW),fuelcellcosttofall70–80 80–150/kW), hydrogen storage (Type IV tanks) to fall 30–40% (US200–300/kgH2,US200–300/kgH2,US 6–10/kWh). LCOE for green hydrogen: US2–3/kg(2025),US2–3/kg(2025),US 1–2/kg (2030), US$ 0.5–1.5/kg (2050).

Outlook and Strategic Recommendations

The QYResearch report projects that by 2030, hydrogen storage for energy storage will exceed 50 GWh deployed (from <1 GWh in 2025), driven by utility-scale projects in Europe (Germany, UK, Netherlands, France, Nordics), US (California, Texas, New York, Midwest), and Asia-Pacific (Japan, South Korea, China). Power-to-gas-to-power (P2G2P) will primarily compete with long-duration batteries (10–100 hours) and pumped hydro (constrained by geography). Hydrogen storage will dominate seasonal storage (weeks to months) due to low storage cost per kWh.

For utility planners, renewable developers, and energy storage investors, three strategic priorities emerge:

- For long-duration storage (24–100 hours, multi-day backup) : Evaluate hydrogen storage (P2G2P) vs. other LDES (long-duration energy storage) technologies (compressed air (CAES), flow batteries (vanadium redox, zinc-bromine), pumped hydro). Hydrogen has lower storage cost than flow batteries for durations >20 hours (NREL analysis). Salt cavern storage for hydrogen is cheapest (US1–5/kWh),butlimitedtosuitablegeology.Above−groundgaseousstorage(US1–5/kWh),butlimitedtosuitablegeology.Above−groundgaseousstorage(US 10–20/kWh) still competitive vs. flow batteries (US100–300/kWh).For24–100hour,hydrogenLCOSUS100–300/kWh).For24–100hour,hydrogenLCOSUS 0.10–0.20/kWh, flow battery LCOS US$ 0.15–0.30/kWh (depending on duration). Recommend: use hydrogen for 50+ hour storage, flow batteries for 10–20 hours, lithium batteries for 2–8 hours.

- For seasonal storage (weeks to months) : Hydrogen is the only viable storage technology (besides synthetic fuels (methane, methanol, ammonia), thermal storage (molten salt in CSP), geological storage (hydrogen, compressed air, natural gas). Use salt cavern hydrogen storage (if available) or lined rock cavern (LRC) for high pressure. Project payback: hydrogen seasonal storage enables 100% renewable grid, avoiding natural gas peaker plants, curtailment, and CO₂ penalties. Seasonal storage cost US0.05–0.15/kWh(hydrogen)vs.US0.05–0.15/kWh(hydrogen)vs.US 1–5/kWh (batteries) — only hydrogen economic.

- For microgrids, remote communities, and critical infrastructure (multi-day backup, 3–7 days) : Install hydrogen storage (gaseous, 350 bar) with electrolyzer (solar/wind powered) and fuel cell (or hydrogen genset). Advantage: no diesel deliveries, zero emissions, quiet, and longer autonomy (3–7 days) than batteries (1–2 days). For island communities (Pacific, Caribbean, Mediterranean, Arctic) and mountain villages, hydrogen storage may be cheaper than submarine power cable or diesel shipping. Payback 5–10 years (depending on diesel cost, renewable resource). Example: island of Orkney (Scotland) hydrogen storage for ferry and backup (BIG HIT project).

The complete *Energy Storage With Hydrogen Conversion – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032* provides segment-level revenue breakdowns by storage phase (gaseous, liquid, solid-state), application (industrial, commercial, utilities, others), and 14 key countries, along with competitive benchmarking, LCOS comparisons, and five-year deployment forecasts.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp