QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Medical Guidewires- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Medical Guidewires market, including market size, share, demand, industry development status, and forecasts for the next few years.

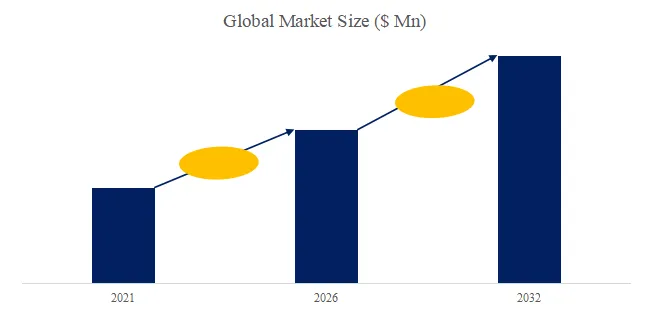

The global market for Medical Guidewires was estimated to be worth US$ 1436 million in 2024 and is forecast to a readjusted size of US$ 2090 million by 2031 with a CAGR of 5.6% during the forecast period 2025-2031.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/4282622/medical-guidewires

Medical Guidewires Market Summary

A medical guidewire is a thin, flexible, semi-rigid wire used by physicians to navigate through blood vessels, anatomical pathways, or other hollow structures within the body. It acts as a “rail” or track over which other devices (like catheters, stents, balloons, or delivery sheaths) can be advanced to a precise target location.

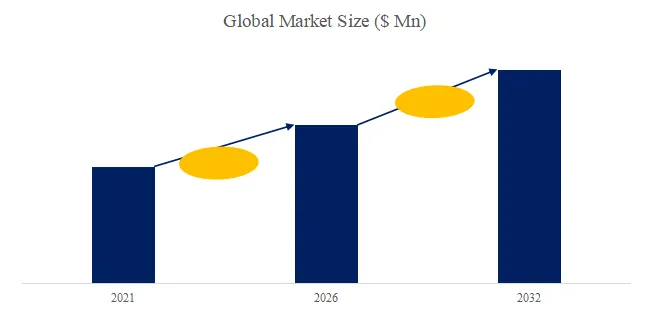

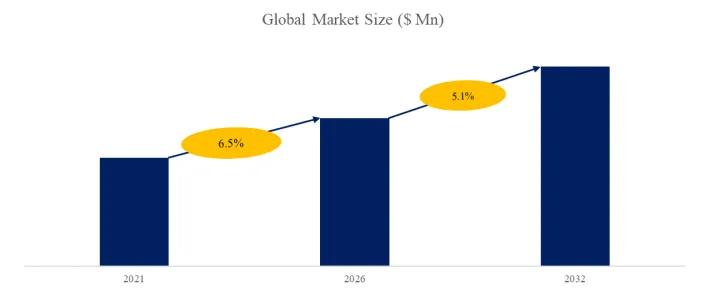

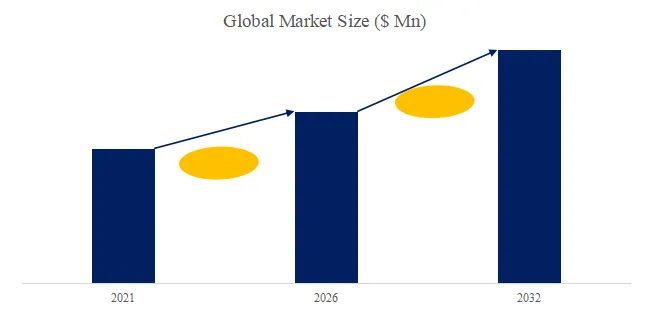

According to the new market research report “Global Medical Guidewires Market Report 2026-2032”, published by QYResearch, the global Medical Guidewires market size is projected to reach USD 2.84 billion by 2032, at a CAGR of 5.2% during the forecast period.

Figure00001. Global Medical Guidewires Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Medical Guidewires Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

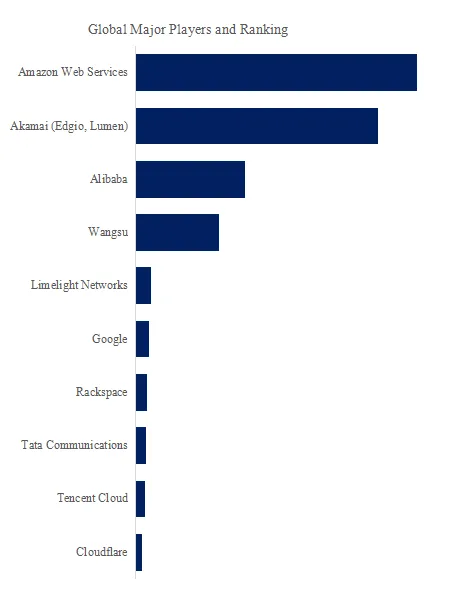

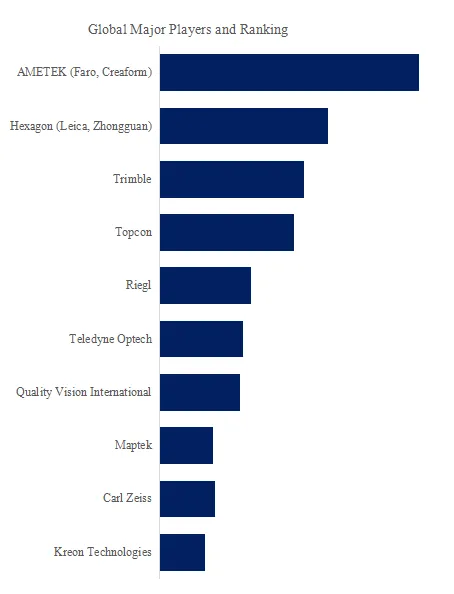

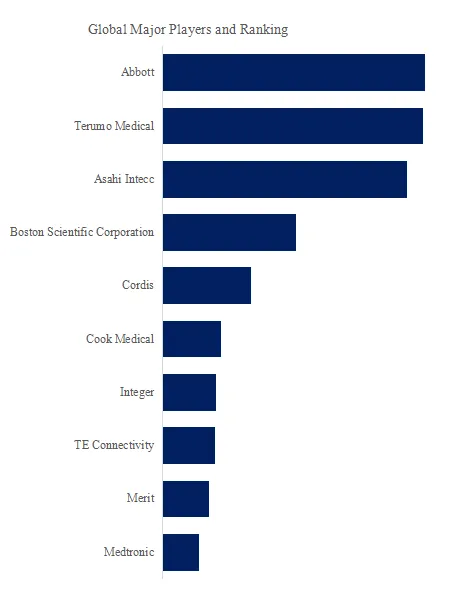

Figure00002. Global Medical Guidewires Top 10 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Medical Guidewires Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Medical Guidewires include Abbott, Terumo Medical, Asahi Intecc, Boston Scientific Corporation, Cordis, Cook Medical, Integer, TE Connectivity, Merit, Medtronic, etc. In 2025, the global top five players had a share approximately 64.0% in terms of revenue.

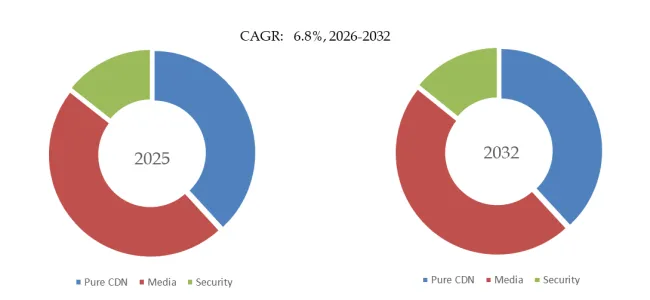

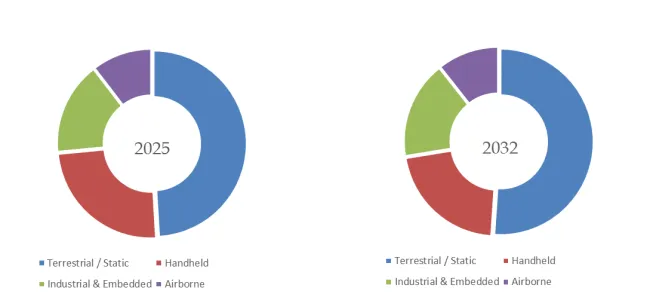

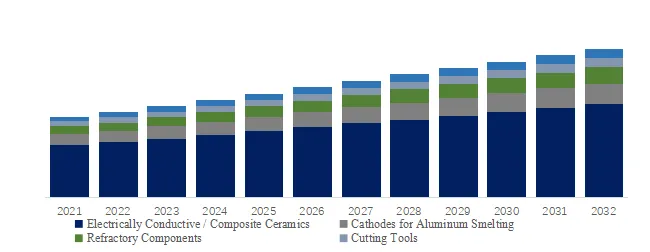

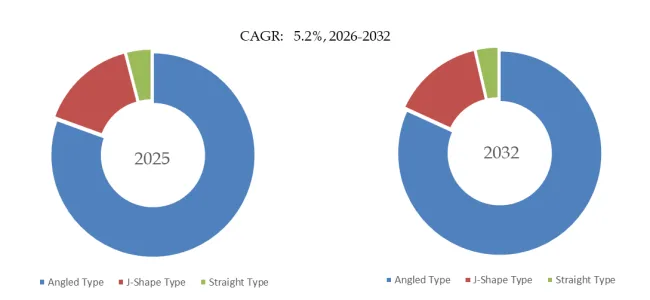

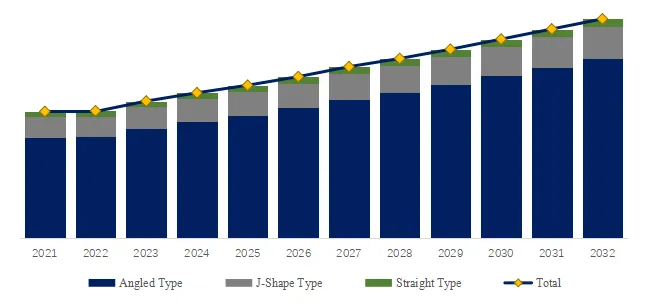

Figure00003. Medical Guidewires, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Medical Guidewires Market Report 2026-2032.

In terms of product type, currently Angled Type is the largest segment, hold a share of 80.5%.

Key Drivers:

1. Rising Prevalence of Chronic Diseases: The increasing global incidence of cardiovascular diseases (CAD, PAD), urological disorders (kidney stones, BPH), and gastrointestinal cancers drives the volume of minimally invasive diagnostic and interventional procedures (angiography, angioplasty, stent placement, biopsies).

2. Aging Population: Older demographics are more prone to conditions requiring vascular and non-vascular interventions, directly increasing the demand for guidewires and associated devices.

2. Shift Towards Minimally Invasive Surgery (MIS): MIS techniques (laparoscopic, endoscopic, percutaneous) offer benefits like shorter hospital stays, less pain, and faster recovery. Guidewires are fundamental tools in virtually all these procedures.

Key Challenges:

1. Technical and Design Complexity:

The “One-Size-Fits-All” Dilemma: No single guidewire can suit all anatomies and procedures. Creating wires that balance flexibility, stiffness, torque control, and pushability for specific applications is a constant engineering challenge.

Navigating Complex Anatomy: Tortuous, calcified, or highly stenotic vessels require exceptional wire performance, and failure to cross a lesion can lead to procedural failure.

2. Stringent Regulatory Landscape: Guidewires are Class II or Class III medical devices (varying by region and risk). Obtaining regulatory approvals (FDA, CE, PMDA) is time-consuming and costly, especially for novel materials or designs. Post-market surveillance requirements are also rigorous.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Medical Guidewires market is segmented as below:

By Company

Invatec S.p.A.

Abbott Vascular

St.Jude Medical

OptiMed Medizinische Instrumente

Medtronic Inc

Segment by Type

Straight Guidewires

J shaped Guidewires

Segment by Application

Percutaneous Transluminal Coronary Angioplasty (PTCA)

Percutaneous Transluminal Angioplasty (PTA)

Other

Each chapter of the report provides detailed information for readers to further understand the Medical Guidewires market:

Chapter 1: Introduces the report scope of the Medical Guidewires report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Medical Guidewires manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Medical Guidewires market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Medical Guidewires in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Medical Guidewires in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Medical Guidewires competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Medical Guidewires comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Medical Guidewires market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Medical Guidewires Market Outlook, In‑Depth Analysis & Forecast to 2031

Global Medical Guidewires Sales Market Report, Competitive Analysis and Regional Opportunities 2025-2031

Global Medical Guidewires Market Research Report 2025

Global Therapeutic Medical Guidewire Market Outlook, In‑Depth Analysis & Forecast to 2031

Global Therapeutic Medical Guidewire Sales Market Report, Competitive Analysis and Regional Opportunities 2025-2031

Therapeutic Medical Guidewire- Global Market Share and Ranking, Overall Sales and Demand Forecast 2025-2031

Global Therapeutic Medical Guidewire Market Research Report 2025

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp