Cameras for School Photography Market Summary

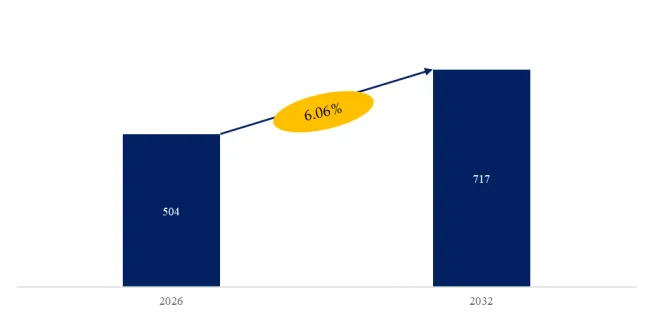

The global Cameras for School Photography market is entering a dynamic phase of transformation, driven by shifting technology preferences, evolving professional photography workflows, and robust demand from educational institutions worldwide. According to recent industry forecasts, the market size reached US$ 479.85 million in 2025 and is projected to expand to US$ 717.20 million by 2032, representing a steady compound annual growth rate (CAGR) of 6.06% during 2026–2032.

This notable growth reflects the continued importance of high-quality imaging equipment within the school photography segment. While smartphones and consumer devices capture informal snapshots, dedicated cameras remain indispensable for professional yearbooks, student portraits, class group photos, and institutional record-keeping. The ongoing recovery of student activity programs and supplementary services lost during the pandemic has also helped reinvigorate demand for professional photography solutions.

Figure00001. Global Cameras for School Photography Market Size (US$ million), 2026-2033

Above data is based on report from QYResearch: Global Cameras for School Photography Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Market Structure: Concentration Among Leading Brands

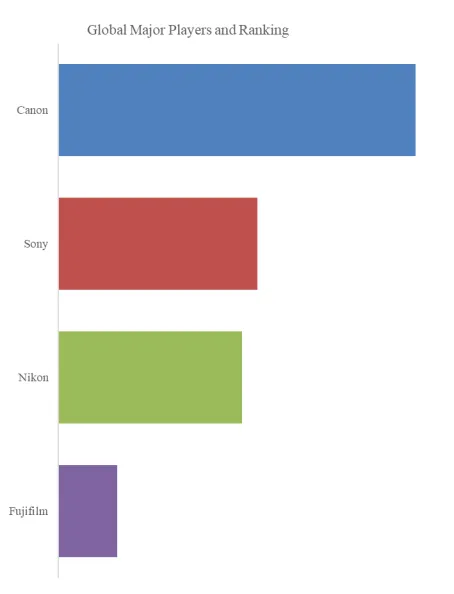

The global landscape for school photography cameras is highly concentrated. In 2025, the top four manufacturers — Canon, Sony, Nikon, and Fujifilm — accounted for approximately 83.78% of total industry revenue. These legacy imaging companies combine broad portfolios, deep dealer networks, and strong brand equity, making them the dominant players in institutional camera procurement.

Figure00002. Global Cameras for School Photography Top 4 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Cameras for School Photography Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Canon remains a leading force, leveraging its extensive expertise in both DSLR and mirrorless systems. The company has actively supported the school photography segment through targeted incentives, financing programs, and educational distributor partnerships, enabling professional photographers to adopt robust camera platforms with lower upfront costs. Sony, recognized for its advanced mirrorless technology and sensor leadership, maintains strong relevance among studios and high-volume shooters, though it has taken a less promotional stance toward this specific market niche. Nikon and Fujifilm reinforce the competitive environment with balanced portfolios that appeal to different workflow preferences and budget tiers.

Beyond the top four, several other manufacturers play meaningful roles. Panasonic and OM Digital Solutions (including Olympus legacy designs) hold smaller but important shares, particularly in niches that value portability and specialized optics. On the premium end, companies such as Leica Camera AG and Ricoh Imaging have minimal direct engagement with school photography but underscore the broader vitality of the imaging ecosystem.

Technological Shifts: DSLR to Mirrorless Migration

One of the most significant structural trends shaping the Cameras for School Photography market is the rapid shift from DSLR to mirrorless systems. In 2025, DSLR cameras still accounted for 50.88% of unit share, with mirrorless cameras comprising 49.12%. However, by 2032, industry forecasts project a substantial inversion: mirrorless systems are expected to command 69.56% of the segment, with DSLRs declining to 30.44%.

This transition reflects both technological advancement and changing professional preferences. Mirrorless cameras offer compelling advantages for school photography workflows, including:

Reduced weight and improved ergonomics, making extended shooting sessions in classrooms, auditoriums, and outdoor events more manageable.

Significantly faster and more accurate autofocus systems, including face and eye detection, which improve portrait consistency across large student populations.

Silent or near-silent operation, especially valuable in environments where disruptive shutter noise is undesirable.

Enhanced video capabilities, enabling hybrid photo-video content for school promotions, event recaps, and digital yearbooks.

Manufacturers have responded by accelerating their mirrorless roadmaps. Canon has expanded its EOS R/RF mount ecosystem with robust mid-tier models that balance performance and cost. Sony continues to refine its Alpha line, pushing boundaries in sensor performance and autofocus intelligence. Nikon’s Z series and Fujifilm’s X series both provide strong options for school photographers, with intuitive controls and compelling imaging quality.

Drivers Behind Growth

Several interlocking drivers underpin the market’s resilient expansion:

1. Recurring Institutional Demand

School photography inherently generates repeat business. Most educational institutions schedule annual photography sessions — including individual portraits, class group shots, alumni events, and extracurricular documentation — creating a predictable market that drives demand for durable and reliable cameras.

2. Professional Service Outsourcing

Many schools outsource photography to specialized service providers rather than managing in-house efforts. This outsourcing fosters ongoing procurement of advanced camera gear as providers seek to maintain quality standards and operational efficiency, particularly under tight scheduling.

3. Digital Workflow Integration

The adoption of cloud-enabled workflow solutions — enabling tethered shooting, rapid image transfer, proofing platforms, and parent delivery portals — enhances the value proposition of dedicated cameras. Vendors increasingly emphasize network connectivity, software compatibility, and high-speed data throughput, aligning product capabilities with modern operational requirements.

Persistent Challenges

Despite positive growth, the market faces several challenges:

High Equipment Costs: Professional camera systems remain significant investments, particularly for smaller photography studios and independent shooters.

Technical Skill Requirements: Effective operation of advanced mirrorless systems demands trained personnel proficient in composition, lighting, and real-time problem solving.

Market Saturation in Developed Regions: In North America and parts of Western Europe, the school photography market is well-penetrated, making new contract acquisition more competitive.

Manufacturers and service providers are responding by offering financing packages, bundled accessories, and training resources to lower barriers to technology adoption.

Regional Outlook and Future Prospects

While demand in mature regions remains substantial, the most promising growth is emerging in Asia-Pacific and Latin America, where expanding educational infrastructure, growing middle-class populations, and increasing investment in school events and extracurricular documentation create new opportunities. The proliferation of digital portfolios, online galleries, and hybrid learning environments also broadens the role of imaging equipment beyond traditional print yearbooks.

Looking forward, the Cameras for School Photography segment is expected to remain robust through 2032 and potentially beyond, driven by technological innovation, recurring institutional demand, and evolving content delivery practices. As mirrorless technology continues to gain traction and manufacturers refine solutions tailored to professional workflows, the market is poised for continued expansion and diversification.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 17 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting (data is widely cited in prospectuses, annual reports and presentations), industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp