QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Nuclear Industry Piping System- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Nuclear Industry Piping System market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for Nuclear Industry Piping System was estimated to be worth US$ 438 million in 2025 and is projected to reach US$ 561 million, growing at a CAGR of 3.7% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6098973/nuclear-industry-piping-system

Nuclear Industry Piping System Market Summary

A Nuclear Industry Piping System is a specialized pipeline network within nuclear facilities used to transport various media (such as coolant, gas, liquid, and radioactive substances). It serves as a core component of nuclear reactors, nuclear fuel cycles, and auxiliary systems. Its core functions encompass three aspects: First, it acts as the “artery” for reactor coolant circulation, transporting light water, heavy water, or liquid metal through high-pressure pipelines to remove heat from nuclear fission and drive steam generators; second, it supports the entire nuclear fuel handling process, including fuel rod transport, spent fuel storage, and waste liquid conveyance in reprocessing, requiring leak-proof, radiation-resistant, and corrosion-resistant characteristics; third, it builds safety barriers, utilizing redundantly designed emergency pipelines to rapidly inject boric acid solution or cooling water under accident conditions to prevent core meltdown. The system employs full-penetration welded structures with materials made from special metals such as stainless steel, nickel-based alloys, or titanium alloys, ensuring stable operation under high-temperature, high-pressure, and intense radiation environments. It is critical infrastructure ensuring nuclear facility safety and economic viability.

The system’s core value lies in achieving stable, and reliable medium transport and pressure boundary sealing under the extreme conditions of high temperature, high pressure, intense radiation, and corrosive media, thereby ensuring the integrity of the nuclear safety barrier. The system typically consists of pipe base materials (stainless steel, nickel-based alloys, zirconium alloys), pipe fittings (elbows, tees, reducers), valves, flanges, welded joints, and support structures. It can withstand thermal cycling impacts ranging from vacuum to supercritical pressure, and from normal temperature to above 350°C. In nuclear power plant primary circuits, secondary circuits, auxiliary systems, and fuel reprocessing facilities, the Nuclear Industry Piping System has become an irreplaceable “nuclear safety-grade lifeline,” with its technological evolution focused on continuous improvement of material corrosion resistance, enhanced weld reliability, full lifecycle traceability, and ongoing refinement of aging management systems.

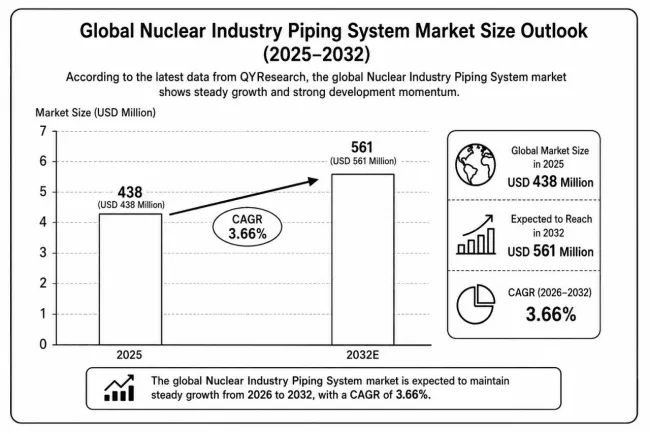

Driven by the continuous growth of global nuclear power installed capacity, the release of life extension and retrofit needs for operating nuclear units, and the accelerated construction of nuclear fuel cycle facilities, the Nuclear Industry Piping System market is undergoing a strategic transformation from “conventional industrial piping” to “nuclear safety-grade long-life piping systems.” According to the latest data from QYResearch, the global market size reached US

438million in2025 and is projected to climb to US 561 million by 2032, registering a steady CAGR of 3.66% from 2026 to 2032.

This growth is underpinned by three core factors: the rigid demand for nuclear-grade piping systems from global under-construction and planned nuclear power units, the replacement and retrofit needs brought by life extension upgrades of operating units, and the continuous拉动 from the construction of nuclear fuel reprocessing and nuclear waste management facilities for specialized piping systems. However, the impact of global trade landscape changes in 2025 on the supply chain of specialty materials such as nickel-based alloys and zirconium alloys, as well as large-diameter seamless pipe forging processes, coupled with industry characteristics such as long certification cycles for nuclear-grade piping and stringent welding inspection standards, is profoundly shaping the product structure and competitive landscape of the global Nuclear Industry Piping System market. This report analyzes product performance classification, competitive dynamics, and industry application characteristics, providing data-driven insights for strategic decision-making.

The global market presents a pattern of “Europe leading in technology, Asia rising in manufacturing, and North America focusing on existing capacity replacement.” Europe, its technological accumulation in nuclear-grade piping material R&D, welding processes, and full lifecycle management, occupies a dominant position in high-end nuclear island primary circuit piping systems. Asia (especially China and South Korea), relying on the world’s largest new nuclear build market and improving local manufacturing capabilities, has become the core engine of global market growth. North America focuses on piping replacement and modernization of operating nuclear units, forming a stable existing capacity market.

Figure00001. Global Nuclear Industry Piping System Market Size

Above data is based on report from QYResearch: Global Nuclear Industry Piping System Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Technology Characteristics & Product Classification

The core technological value of the Nuclear Industry Piping System lies in integrating the three nuclear safety requirements—”extreme condition tolerance, long-term reliability, inspectability and repairability”—into the full lifecycle management of piping, providing a “safe, reliable, traceable” fluid transport barrier for nuclear facilities. Its technological evolution presents three major trends: First, continuous breakthroughs in material performance, evolving from conventional austenitic stainless steels to advanced alloys with higher corrosion resistance and lower radiation sensitivity (such as 316L with higher molybdenum content, niobium-containing nickel-based alloys), while advancing the engineering application of FeCrAl and SiC composite materials for accident-tolerant fuel cladding; second, upgrading of manufacturing processes toward automation and digitalization, adopting narrow-gap automatic welding, laser-arc hybrid welding, phased array ultrasonic testing, and other technologies to enhance weld quality stability and inspection reliability; third, maturation of aging management and life extension technologies, establishing pipeline remaining life assessment models based on probabilistic fracture mechanics, and developing in-service repair (such as build-up welding, sleeving) and replacement technologies to support unit life extension to 80 years.

By Pressure Level Classification:

High-Pressure Piping System (Design Pressure ≥10MPa): Mainly used in nuclear power plant primary circuit main coolant systems, main steam systems, and pressurizer surge lines, with design temperatures typically between 300°C-350°C. High-pressure piping systems require materials with excellent high-temperature creep strength, low-cycle fatigue resistance, and resistance to stress corrosion cracking. Pipes are typically large-diameter thick-walled seamless tubes (outer diameter up to 800mm or more), with wall thickness up to 50mm-100mm. This category has the highest technical barriers and most stringent quality requirements in the nuclear industry piping market; almost all are Nuclear Safety Class 1 equipment, requiring equipment manufacturing licenses and surveillance throughout the manufacturing process. Estimated average price: 25,000−50,000 USD/ton.

Medium-and Low-Pressure Piping System (Design Pressure <10MPa): Covers nuclear power plant secondary circuit feedwater systems, circulating cooling water systems, equipment cooling water systems, compressed air systems, and chemical volume control systems. These systems require materials with good corrosion fatigue resistance and erosion-corrosion resistance, but have smaller design wall thicknesses (typically 10mm-50mm), with lower manufacturing difficulty and certification levels (Nuclear Safety Class 2/3 or non-safety). In nuclear power plants, this category has the largest and longest total length, accounting for approximately 60%-70%. Due to higher standardization, prices are relatively transparent, with estimated average price: 8,000−18,000 USD/ton.

Vacuum Piping System: Used in uranium hexafluoride (UF₆) transport in nuclear fuel cycle facilities, accelerator vacuum chambers in nuclear research facilities, and some reprocessing process steps. Vacuum piping systems require extremely low leak rates (≤10⁻⁹ Pa·m³/s at room temperature) and good internal surface cleanliness, typically using electropolishing or electrolytic polishing. Due to small batch sizes and high customization, estimated average price: 30,000−60,000 USD/ton.

By Application:

Nuclear Power Plants (Nuclear Island + Conventional Island): The largest application segment for Nuclear Industry Piping Systems, accounting for approximately 70%, covering primary circuit main coolant piping, main steam piping, feedwater piping, and various auxiliary piping.

Nuclear Fuel Cycle Facilities (uranium conversion, uranium enrichment, fuel element manufacturing, spent fuel reprocessing): Approximately 20%, with special requirements for corrosion resistance (nitric acid, fluorides) and cleanliness.

Nuclear Research Facilities (research reactors, critical assemblies, hot cells): Approximately 10%, mainly small-diameter precision piping and special alloy piping.

Actual Procurement & Application Characteristics

The procurement process for Nuclear Industry Piping Systems involves nuclear power engineering general contractors (EPC contractors), nuclear power plant owners, nuclear fuel cycle facility construction entities, and research institutions. The process is highly specialized and depends on nuclear safety classification, material certification, and long-term supply stability, centering on material grades, manufacturing process certification, non-destructive testing standards, and supply track records.

In the early procurement stage, buyers typically conduct rigorous technical reviews and source verifications of pipe manufacturers, including inspection of manufacturing licenses, material retesting (chemical composition, mechanical properties, metallographic structure, grain size), process qualification (welding processes, heat treatment processes), and product qualification (ultrasonic testing, radiographic testing, liquid penetrant testing). After validation, nuclear power projects typically adopt a public tender + first article qualification + batch production model, requiring suppliers to provide complete material traceability documentation (from melt number to finished pipe section) and quality plans, with witnessing of critical process steps (such as forging, piercing, solution heat treatment).

In terms of procurement structure, new nuclear build projects have concentrated demand in large batches, typically locking production capacity 2-3 years in advance. Spare parts procurement for operating units is characterized by “small batches, multiple varieties, emergency delivery,” demanding high inventory and rapid response capabilities from suppliers. In the post-procurement phase, owners continuously evaluate the long-term reliability of manufacturer products based on in-service inspection data (such as evolution of ultrasonic testing defect signals, oxide film thickness), forming a complete application system of “technical specifications—tender procurement—manufacturing surveillance—in-service tracking—aging assessment. ”

Tariff Policies & Supply Chain Restructuring

Changes in the global trade landscape in 2025 are having structural impacts on the Nuclear Industry Piping System market:

1. Supply Chain Risks for Specialty Alloy Raw Materials Become Evident. The melting and hot working capabilities for nickel-based alloys (Inconel 690/718/625), zirconium alloys, and advanced stainless steels are highly concentrated among a few European, American, and Japanese companies. Trade policy fluctuations may lead to extended delivery times and increased costs for large-diameter seamless tubes, forgings, and other semi-finished products, forcing companies in emerging markets like China to accelerate the localization of specialty alloys and establish safety stocks and diversified procurement channels.

2. Regional Barriers in Nuclear-Grade Piping Certification Intensify. Differences exist in the certification systems of nuclear safety regulators across countries (e.g., US ASME certification, French RCC-M certification, Chinese HAF certification). Cross-regional supply requires repeated qualification, increasing supplier compliance costs and market access timelines. Some nuclear power projects strengthen localization manufacturing requirements in tenders, requiring international suppliers to meet准入 thresholds through local joint ventures or technology transfer.

3. Increased Supply Chain Risks in Transport and Installation. International transport of large-diameter thick-walled pipes (up to 12 meters or more in length) is affected by shipping routes, ports, customs clearance, and other factors. Geopolitics and trade policy changes may lead to project delays. Some nuclear power projects promote “localized manufacturing +分段 supply” models to reduce dependence on long-distance cross-border transportation.

4. Digital Traceability Becomes a New Dimension of Supply Chain Competition. Nuclear-grade piping requires full-chain data traceability from melt number to installation weld. Suppliers with digital quality management systems (e.g., electronic quality plans, blockchain traceability) have a competitive advantage in bidding.

Market Participant Competitive Landscape Analysis

Global participants in the Nuclear Industry Piping System market exhibit a distinct multi-level competitive landscape of “Europe leading in high-end materials, Asia expanding in manufacturing scale, North America supplementing with specialized services.”

The upstream core focuses on specialty alloy melting and tube blank hot working. Global supply of high-quality nickel-based alloys, zirconium alloys, and large-diameter stainless steel seamless tube blanks is highly concentrated among NIPPON STEEL (Japan, globally leading specialty steel manufacturer), Sandmeyer Steel Company (USA, stainless steel and nickel alloy plate/pipe), Tubacex (Spain, leading stainless steel and nickel alloy seamless pipe), Centravis (Ukraine/Global, seamless stainless steel pipe specialist), TSINGCO (China, specialty alloy pipe), and others. These companies have built deep technical in alloy composition optimization, hot piercing processes, and non-destructive testing.

The midstream segment is Nuclear Industry Piping System manufacturing and integration. Through pipe rolling/extrusion, pipe bending, beveling, heat treatment, and surface treatment processes, tube blanks are processed into finished pipe sections and fittings meeting nuclear-grade requirements. Core participants include: Bilfinger (Germany, nuclear-grade piping system integration and services), ISCO Industries (USA, specialty piping system supplier), Stenflex (nuclear-grade hoses and expansion joints), Anvil (pipe supports and hangers), Langfields (UK, nuclear-grade tanks and piping systems), Laker-vent (ventilation ducts and nuclear-grade penetrations), Sunny Steel (China, specialty steel pipe exporter), Shanghai Zhongsu Pipe (China, nuclear-grade plastic piping and lined piping), and Amerplastics (USA, nuclear-grade plastic piping systems). Companies in this segment typically also provide prefabrication, welding, modular assembly, and on-site installation services, with project-based delivery as the main model.

Downstream end demand is primarily composed of nuclear power engineering companies, nuclear power plant owners, nuclear fuel cycle facility operators, and research institutions. Fives Group (France, industrial engineering and piping system services) and NIPPON STEEL also vertically extend into pipe supply. Overall, the Nuclear Industry Piping System market exhibits a “high-end materials + specialized manufacturing + engineering services” vertical integration trend, with companies possessing complete qualification chains and track records having competitive advantages.

Future Development Outlook

In the future, the Nuclear Industry Piping System will continue to evolve three major sectors: new nuclear build, operating unit life extension, and nuclear fuel cycle facility construction, achieving industrial upgrading driven by three forces: material localization, manufacturing intelligence, and management digitalization.

In the nuclear power plant construction sector, with the construction of Generation III technologies (China’s Hualong One, Russia’s VVER, South Korea’s APR1400, US AP1000, Europe’s EPR) and the commercial advancement of Generation IV reactors (such as high-temperature gas-cooled reactors, sodium-cooled fast reactors), demand will emerge for advanced pipe materials suitable for higher temperatures and higher neutron fluxes (such as FeCrAl, SiC composites). Pipe manufacturers need to collaborate with reactor designers to conduct out-of-core and in-core material performance verification.

In the operating nuclear unit life extension sector, approximately 70% of global operating nuclear units are over 30 years old. Piping aging (thermal aging, irradiation embrittlement, corrosion thinning, fatigue accumulation) is a key focus of life extension reviews. Pipe remaining life assessment based on probabilistic fracture mechanics, in-service repair (local build-up welding, sleeving reinforcement), and replacement technologies will form a stable technical service market.

In the nuclear fuel cycle facility sector, with the construction of spent fuel reprocessing plants (such as France’s La Hague, UK’s Sellafield, China’s spent fuel reprocessing plant) and advanced fuel manufacturing facilities, demand will increase for specialty piping systems resistant to nitric acid corrosion, with high cleanliness and low cobalt equivalent, forming a differentiated development direction from nuclear power plant piping.

In the technology convergence direction, digital twin technology will cover the entire lifecycle of piping from design, manufacturing, installation, operation, to decommissioning; deep integration of robotic automatic welding and phased array ultrasonic testing will the manufacturing and in-service inspection of piping systems toward unmanned, precision direction.

Overall, the Nuclear Industry Piping System industry remains in a phase of parallel continuous technological progress and steady market growth. With the continuous improvement of global nuclear power industry safety standards, steady of new projects, and release of life extension needs for operating units, the industry’s long-term growth is highly certain. It is expected to gradually upgrade from “nuclear safety-grade conventional equipment” to the “basic carrier for nuclear power plant full-lifecycle intelligent management.”

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Nuclear Industry Piping System market is segmented as below:

By Company

Fives Group

Tubacex

Bilfinger

Amerplastics

ISCO Industries

Stenflex

Anvil

Sandmeyer Steel Company

Langfields

NIPPON STEEL

TSINGCO

Laker-vent

Sunny Steel

Shanghai Zhongsu Pipe

Centravis

Segment by Type

High-Pressure Piping System

Medium- And Low-Pressure Piping System

Vacuum Piping System

Segment by Application

Nuclear Power Plants

Nuclear Fuel Cycle Facilities

Nuclear Research Facilities

Other

Each chapter of the report provides detailed information for readers to further understand the Nuclear Industry Piping System market:

Chapter 1: Introduces the report scope of the Nuclear Industry Piping System report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Nuclear Industry Piping System manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Nuclear Industry Piping System market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Nuclear Industry Piping System in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Nuclear Industry Piping System in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Nuclear Industry Piping System competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Nuclear Industry Piping System comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Nuclear Industry Piping System market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Nuclear Industry Piping System Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Nuclear Industry Piping System Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Nuclear Industry Piping System Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp