QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Data Center Transceiver- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Data Center Transceiver market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for Data Center Transceiver was estimated to be worth US$ 407 million in 2025 and is projected to reach US$ 603 million, growing at a CAGR of 5.8% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6262804/data-center-transceiver

Data Center Transceiver Market Summary

Data center transceiver is a core photoelectric conversion device used for high-speed data communication among servers, switches and storage devices in data centers. Its main function is to convert electrical signals into optical signals at the device end for transmission through optical fibers and restore optical signals to electrical signals at the receiving end, thus achieving high-speed, long-distance, low-loss data interconnection. Its typical packaging forms include SFP, QSFP, OSFP, etc., supporting speeds from 1G to 800G and even higher. It is a key component for building modern data center network infrastructure.

According to the new market research report “Global Data Center Transceiver Market Report 2026-2032″, published by QYResearch, the global Data Center Transceiver market size is projected to grow from USD 406.58 million in 2025 to USD 603 million by 2032, at a CAGR of 5.8% during the forecast period.

Table. Global Data Center Transceiver Main Manufacturers

| Headquarter | Company | Business Introduction |

| USA | Coherent Corp | Coherent is a leading global photonics technology company focusing on the data center, communications, and industrial markets. Its business encompasses optical transceivers, optical modules, lasers, amplifiers, optoelectronic devices, and related materials and system solutions. It also provides laser and materials technologies for precision manufacturing, semiconductors, and display devices. Its core strength lies in its vertically integrated capabilities, from materials and devices to modules and systems. |

| USA | Lumentum | Lumentum is a leading global optics and photonics technology company focusing on AI, cloud computing, and next-generation communications infrastructure. Its main businesses encompass optical devices, modules, and subsystems for data centers and telecommunications networks, as well as laser and photonic solutions for applications such as industrial manufacturing and 3D sensing. Its core strengths lie in high-speed optical connectivity and precision optoelectronics technologies. |

| USA | Source Photonics | Source Photonics is a manufacturer of optical devices and modules specializing in optical communication and data connectivity technologies, providing products for the data center, telecom access, fixed broadband, and wireless broadband markets. Its business encompasses data center optical transceivers, optical devices and subsystems, PON access products, and transmission-related solutions. Its core competency lies in the integrated design and manufacturing of optoelectronic devices, optical sub-components, and modules. |

| USA | CommScope | CommScope is a network connectivity infrastructure provider focusing on wired and wireless network construction, serving scenarios such as data centers, enterprise campuses, broadband access, and carriers. Its main businesses cover fiber optic and copper cabling, data center connectivity platforms, enterprise networks, access networks, and related network solutions. Its core value lies in providing end-to-end highly reliable connectivity and network infrastructure support. |

| China | ELVAST OPTICS | ELVAST OPTICS is a manufacturer specializing in optical communication modules, primarily providing optical transceivers for enterprise networks, access networks, metropolitan area networks, and core networks. Its business focuses on research, design, production, and sales of optical modules, with products designed to meet the data transmission needs of various optical network scenarios. The company positions itself as a supplier of cost-effective and standard-compatible optical communication devices. |

| China | 3C-LINK | 3C-LINK is a supplier of optical communication and FTTX solutions, whose main business covers optical transceivers, high-speed networks, OTN systems, CWDM/DWDM systems, and active and passive FTTX products. Its products include SFP/QSFP optical modules, PON equipment, Ethernet fiber optic conversion equipment, and WDM devices, positioning itself as a provider of one-stop optical connectivity solutions for data communication, access networks, and carrier networks. |

| USA | Applied Optoelectronics, Inc. | Applied Optoelectronics, Inc. (AOI) is a company specializing in optical communication and network access products for the data center, wired broadband, wireless, and telecommunications markets. Its main businesses encompass optical transceivers, lasers and optics, CATV and FTTH access equipment, and related high-speed connectivity products. Its core strength lies in its vertically integrated manufacturing capabilities, from key optical components to modules. |

| USA | Wavesplitter Corporation | Wavesplitter Corporation is a supplier of optical communication devices and modules, specializing in high-performance optical connectivity solutions. Its business encompasses laser chips, photodetectors, optical engines, optical transceivers, and products such as PON and CWDM/DWDM, targeting the AI/HPC, data center, 5G communication, and broadband access markets. A key feature is its vertically integrated capability, from optical chip design and packaging to module development. |

| USA | Cisco Systems | Cisco Systems is a leading global networking and digital infrastructure technology company focused on connectivity, security, observability, and collaboration for the AI era. Its main businesses encompass switches, routers, data center networks, security, and collaboration software and services, providing digital and network infrastructure solutions for enterprises, carriers, and the public sector through a combination of hardware and software. |

| USA | Molex | Molex is a leading global provider of electronic interconnect solutions, dedicated to providing critical connectivity for data centers, automotive, industrial, medical, and consumer electronics. Its main businesses encompass connectors, cable assemblies, optical connections, antennas, industrial automation, data center infrastructure, and related customized solutions. Its core strengths lie in its highly reliable interconnect products and cross-industry engineering collaboration capabilities. |

| Japan | Sumitomo Electric Industries | Sumitomo Electric Industries is a diversified materials and advanced manufacturing company with businesses spanning information and communications, automotive, environmental energy, industrial materials, and electronics. Its main businesses include fiber optic cables, communication devices and network products, automotive wiring harnesses and components, power cables and energy systems, as well as rigid materials, electronic wires, and industrial equipment. A key characteristic is its reliance on materials technology to support diverse industrial applications. |

| Japan | Fujitsu Optical Components | Fujitsu Optical Components (FOC) is a subsidiary of Fujitsu specializing in high-speed optical communication devices and modules, targeting the backbone network, metropolitan area network, data center, and optical transmission markets. Its business encompasses lithium niobate modulators, integrated coherent receivers, coherent optical modules, client optical modules, and thin-film lithium niobate (TF-LN) related technologies. Its core strength lies in its capabilities for high-performance optical device design, packaging, and mass production. |

| Japan | NEC Corporation | NEC Corporation is a leading global ICT and social infrastructure company, committed to creating safe, secure, equitable, and efficient social value through digital technologies. Its main businesses encompass IT services, systems integration, cloud and outsourcing services, as well as solutions related to social infrastructure such as communications infrastructure, optical transmission, mobile networks, submarine cables, aerospace, and defense. |

| Switzerland | HUBER+SUHNER | HUBER+SUHNER is a global company specializing in electrical and optical connectivity technologies, developing and manufacturing components and system solutions for the communications, industrial, and transportation markets. Its main business revolves around three core technologies: radio frequency (RF), fiber optics, and low frequency (LHF). Its products include connectors, cables, antennas, fiber optic assemblies, and related connectivity systems, emphasizing high performance, high reliability, and long lifespan applications. |

| German | Flexoptix GmbH | Flexoptix is a manufacturer specializing in optical communication transceivers and network connectivity products, targeting the data center, telecommunications, and enterprise network markets. Its main business encompasses programmable general-purpose optical modules, DAC/AOC high-speed cables, and the accompanying configuration tool FLEXBOX. A key feature is its support for multi-vendor equipment compatibility and rapid configuration, helping customers reduce inventory complexity and improve network operation and maintenance flexibility. |

| Korea | Lightron Inc. | Lightron is a manufacturer specializing in optical communication devices and modules, serving wireless backhaul, fixed broadband, telecom/data communication, and CATV markets. Its main products include optical transceivers, PON equipment and devices, photonic components, and related optical module solutions, with a focus on high-speed optical connectivity and access network applications. |

Above data is based on report from QYResearch: Global Data Center Transceiver Market Report 2026-2032 (published in 2026). If you need the latest data, plaese contact QYResearch.

Data Center Transceiver Supply Chain Analysis:

Upstream: Includes core components such as DSP/PHY, lasers (EML/CW laser), silicon photonics chips, drivers/TIAs, connectors, and optical fibers.

Midstream: Optical module manufacturers complete the design, packaging, coupling, calibration, and testing of 800G/1.6T transceivers, and are highly dependent on manufacturing collaborations with companies like Fabrinet.

Downstream: Mainly AWS, Meta, Google, Microsoft, and switch manufacturers. Current growth is primarily driven by the increased use of 800G in AI data centers, with 1.6T beginning to be adopted; however, bottlenecks are concentrated in the supply, yield, power consumption, and advanced packaging of key optical components such as 100G EML, and the industry is gradually evolving from traditional pluggable modules to silicon photonics and co-packaged optics (CPO).

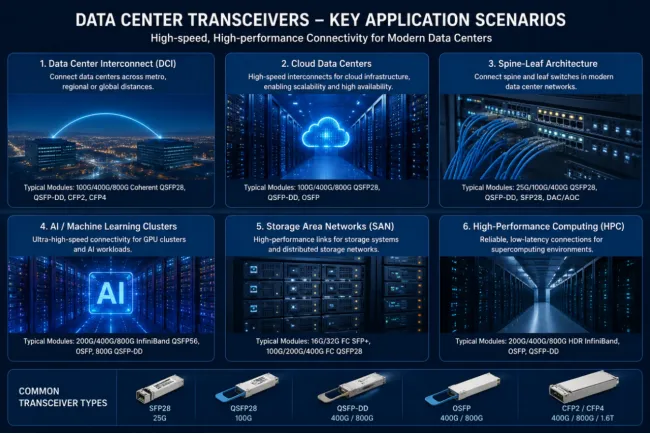

Main Application Scenarios for Data Center Transceivers:

Key Driving Factors:

The core driver lies in the exponential data interaction demands brought about by AI large-scale model training and inference. This necessitates that the interconnection of GPU clusters within intelligent computing centers rely on high-bandwidth, low-latency optical interconnect solutions, directly driving up the deployment ratio and procurement scale of high-speed transceivers such as 800G and 1.6T. Simultaneously, the penetration of digital services such as cloud computing, streaming media, and the Internet of Things has led to a continuous surge in data center traffic. Traditional electrical interconnects are encountering bandwidth and power consumption bottlenecks, making low-power, highly integrated technologies such as pluggable optical modules, silicon photonics, and CPO key upgrade priorities. Furthermore, the expansion of global hyperscale data centers, the deployment of edge computing nodes, and the rising demand for DCI long-distance interconnects, coupled with infrastructure policies such as “Eastern Data, Western Computing” and green energy efficiency requirements, have collectively propelled the industry towards rapid iteration and mass deployment of higher-speed, smaller-size, lower-power, and more reliable hot-swappable transceivers.

Key Obstacles:

The primary obstacle lies in the exponential deterioration of channel loss and crosstalk in high-speed signal transmission with increasing data rate. This places near-stringent demands on the consistency of PCB materials, connectors, and optical devices, leading to immense pressure on yield control and mass production costs. Simultaneously, thermal management challenges under high-density deployments are extremely severe. Optoelectronic devices are highly sensitive to temperature; poor heat dissipation directly causes wavelength drift and a surge in bit error rate. Existing cooling solutions often conflict with high-density designs, and the power consumption wall becomes increasingly prominent with increasing data rates. Especially when using traditional DSP solutions for 800G and above modules, the power consumption of a single module is approaching the power supply limit of the server interface, severely restricting rack power budgets. Furthermore, interoperability testing between chips and modules from different manufacturers is extremely complex, with frequent protocol compatibility and timing matching issues slowing down the introduction of new products. In addition, the requirements for carrier-grade reliability standards and dispersion compensation for long-distance transmission further increase R&D barriers and material costs. These factors collectively constitute the technological and cost barriers restricting the large-scale adoption of higher-speed transceivers in data centers.

Industry Development Opportunities:

The industry is rapidly iterating towards ultra-high speeds such as 800G and 1.6T to match the surging bandwidth demands of AI computing clusters and cloud data centers. Pluggable form factors remain the mainstream but are gradually approaching power consumption and density limits, driving the rise of new architectures such as linear-driven pluggable optics and co-packaged optics. Silicon photonics technology is accelerating its penetration due to its cost and integration advantages. Low power consumption and high thermal efficiency design have become core considerations to meet the requirements of green data centers. At the same time, optical interconnects are transforming from auxiliary components into a key link affecting the expansion of AI infrastructure. The supply chain is shifting its focus to ensuring the production capacity of core optoelectronic chips and advanced packaging and testing capabilities. Product form factors will also be closer to switch chips or direct I/O to achieve extreme latency and energy efficiency.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Data Center Transceiver market is segmented as below:

By Company

Coherent Corp

Lumentum

Source Photonics

CommScope

ELVAST OPTICS

3C-LINK

Applied Optoelectronics, Inc.

Wavesplitter Corporation

Cisco Systems

Applied Optoelectronics (AAOI)

Molex

Sumitomo Electric Industries

Fujitsu Optical Components

NEC Corporation

HUBER+SUHNER

Flexoptix GmbH

Lightron Inc.

Segment by Type

Above 800Gb/s

400-800Gb/s

100-300Gb/s

Below 100Gb/s

Segment by Application

Online Commerce

Streaming Video

Social Network

Software and Cloud Services

Others

Each chapter of the report provides detailed information for readers to further understand the Data Center Transceiver market:

Chapter 1: Introduces the report scope of the Data Center Transceiver report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Data Center Transceiver manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Data Center Transceiver market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Data Center Transceiver in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Data Center Transceiver in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Data Center Transceiver competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Data Center Transceiver comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Data Center Transceiver market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Data Center Transceiver Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Data Center Transceiver Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Data Center Transceiver Market Research Report 2026

Global 800G Data Center Transceiver Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global 800G Data Center Transceiver Market Outlook, In‑Depth Analysis & Forecast to 2032

Global 800G Data Center Transceiver Market Research Report 2026

800G Data Center Transceiver- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp