Global Leading Market Research Publisher QYResearch announces the release of its latest report “Vehicle-Road Collaboration Solutions – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Vehicle-Road Collaboration Solutions market, including market size, share, demand, industry development status, and forecasts for the next few years.

For transportation agencies, automotive OEMs, smart city planners, and mobility service providers, the persistent challenge remains consistent: reducing traffic accidents, alleviating congestion, and enabling higher levels of vehicle automation through real-time communication between vehicles and roadside infrastructure. Vehicle-road collaboration solutions (also known as V2X – Vehicle-to-Everything, or C-ITS – Cooperative Intelligent Transport Systems) enable vehicles to communicate with traffic signals, roadside units (RSUs), other vehicles, cloud platforms, and vulnerable road users. The market encompasses equipment (RSUs, onboard units (OBUs), sensors, edge computing nodes, traffic controllers) and services (cloud platforms, data analytics, traffic optimization algorithms, maintenance). Deployed across urban roads (intersections, school zones, bus corridors) and highways (ramp metering, work zones, emergency vehicle preemption), these solutions are critical for Level 4/5 autonomous driving (providing sensor redundancy and “super-sensing” beyond line-of-sight).

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5719070/vehicle-road-collaboration-solutions

1. Market Size & Growth Trajectory (2026–2032)

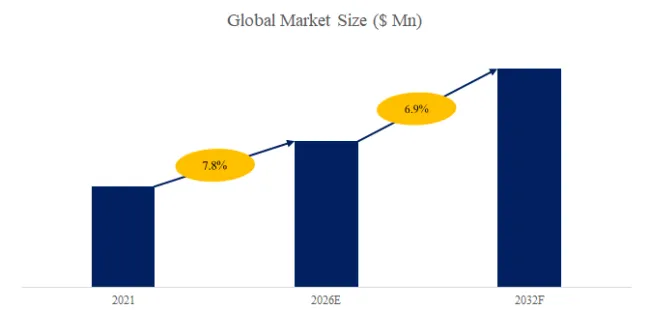

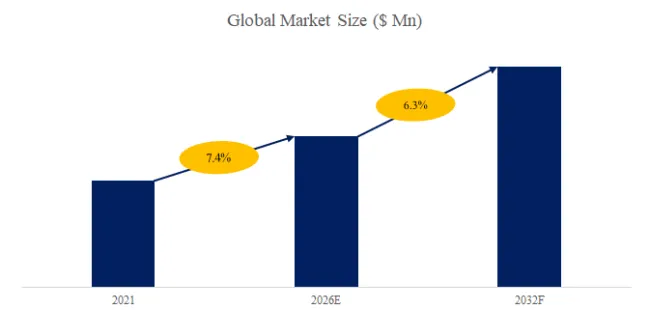

The global market for Vehicle-Road Collaboration Solutions was estimated to be worth US$ 3.2 billion in 2025 and is projected to reach US$ 12.8 billion by 2032, growing at a CAGR of 21.9% from 2026 to 2032. In 2024, China dominated the market (≈65% of global deployments) due to national C-V2X (Cellular V2X) mandates and pilot cities (over 50 cities with vehicle-road collaboration infrastructure, 10,000+ km of smart highways). The US and Europe are accelerating with USDOT’s CV Pilot Deployment Program (New York, Tampa, Wyoming) and EU’s C-Roads Platform (20+ member states).

Exclusive industry observation: The vehicle-road collaboration market is experiencing explosive growth (21.9% CAGR) driven by three transformative factors: (1) China’s national C-V2X mandate (2025-2027: 30% of new vehicles equipped with C-V2X, 50% of highways with RSUs); (2) autonomous vehicle safety requirements (redundancy and “super-sensing” for Level 4+ AVs beyond onboard sensors); (3) road safety and congestion reduction (NHTSA estimates V2X could prevent 80% of non-impaired crashes, 500,000+ accidents annually in US alone).

2. Industry Segmentation & Key Players

The market is segmented by component into Equipment (hardware: RSUs, OBUs, sensors, edge computing, traffic controllers) and Services (software platforms, cloud analytics, deployment, maintenance, data processing), and by application into Urban Roads (city intersections, arterials, school zones, bus rapid transit) and Highways (rural interstates, toll roads, work zones, tunnel/bridge approaches).

By Component – Value Chain and Business Models

| Component | Key Offerings | 2025 Market Share | Typical Pricing | Key Vendors |

|---|---|---|---|---|

| Equipment (Hardware) | RSUs (DSRC/C-V2X), OBUs (aftermarket and embedded), edge compute nodes (MEC), traffic signal controllers, roadside sensors (radar, LiDAR, camera) | 60% | RSU: $3,000-15,000; OBU: $200-1,500 (aftermarket), $50-200 (embedded) | Huawei, Baidu, China TransInfo, Wanji Technology, Hitachi, Nexteer, SWARCO |

| Services (Software/Platform) | Cloud-based V2X platforms, traffic optimization algorithms, real-time analytics, map updates, data security (PKI), deployment and integration, maintenance | 40% | $50,000-500,000 per city/year (platform), $5-15 per vehicle/year (service fee) | Tencent, Alibaba, Baidu (Apollo), Huawei (OceanConnect), EMQ, Enel Energia, The Mobility House |

Industry layer analysis – Discrete vs. Process Analogies: Urban Roads (≈65% of vehicle-road collaboration revenue, analogous to “dense, high-complexity” – many intersections, diverse road users, high latency sensitivity) represents the largest segment, driven by smart city initiatives and autonomous shuttle deployments. Highways (≈35%, analogous to “linear, long-distance” – fewer intersections but longer corridors, higher speeds, commercial vehicle focus) emphasizes truck platooning, work zone safety, and emergency response.

Key Suppliers (2025)

Prominent global vehicle-road collaboration solution providers include:

- Chinese technology giants: Huawei (C-V2X RSUs, OceanConnect platform, leading market share), Baidu (Apollo V2X platform, ACE smart mobility), Tencent (cloud V2X services), Alibaba (ET City Brain, cloud V2X), China TransInfo Technology (RSUs, traffic controllers), Wanji Technology (OBUs, RSUs)

- European and Japanese: EMQ (V2X messaging/connectivity), Enel Energia (smart charging integration), The Mobility House (V2G), Hitachi (RSUs, traffic management), Nexteer (steering and V2X integration), SWARCO (traffic controllers, RSUs, C-ITS)

- US (emerging, DSRC focus): Commsignia, Cohda Wireless, Savari (now Haes), Kapsch TrafficCom

Exclusive observation: China is 3-5 years ahead of US/Europe in vehicle-road collaboration deployment, driven by: (1) national policy (MIIT’s C-V2X roadmap), (2) technology choice (C-V2X vs. US/Europe’s DSRC/ITS-G5 fragmentation), (3) government funding (smart infrastructure as national priority). Huawei leads Chinese market (≈40% RSU share), with Baidu and Tencent competing in V2X software platforms. US and Europe are transitioning from DSRC (802.11p) to C-V2X (3GPP Rel-14/16) following FCC’s 5.9 GHz band reallocation (2020) and Europe’s C-ROADS adoption of C-V2X.

3. Technology Trends, Policy Drivers & User Cases (Last 6 Months)

Recent technology advancements (Q3 2025–Q1 2026):

- 5G NR-V2X (3GPP Rel-16/17) – Enhanced V2X with higher throughput (1 Gbps), lower latency (<10ms), and extended range (>1km), enabling cooperative perception (vehicles sharing raw sensor data) and remote driving.

- Edge computing (MEC) for V2X – Huawei, Baidu, Tencent deploying roadside edge nodes (AI inference, sensor fusion) reducing cloud round-trip latency from 100ms to 20-50ms (critical for safety applications).

- Sensor-fusion RSUs – Multi-modal RSUs (camera + radar + LiDAR + C-V2X) providing “super-sensing” for occluded intersections (detecting pedestrians/cyclists/vehicles beyond line-of-sight).

- V2X PKI security – Certificate management systems (SCMS in US, EU C-ITS trust model, China’s V2X Root CA) enabling secure, privacy-preserving V2X communications (anonymous certificates rotated every 5 minutes).

- V2G (Vehicle-to-Grid) integration – The Mobility House, Enel Energia integrating V2X with smart charging for bidirectional power flow (EVs providing grid balancing services).

Policy & regulatory updates (last 6 months):

- China MIIT “C-V2X Frequency Management” (October 2025) – Dedicated 20MHz spectrum (5905-5925MHz) for C-V2X, mandatory for all new vehicles by 2027, accelerating OBU penetration.

- USDOT National V2X Deployment Plan (December 2025) – $500 million for C-V2X RSU deployment on 50,000 miles of highway by 2030, targeting 80% of intersections in 50 largest metros.

- EU C-ROADS Platform expansion (November 2025) – 25 member states committed to interoperable C-ITS (C-V2X and ITS-G5), with cross-border corridors (Rotterdam-Frankfurt-Vienna) deployed 2026-2028.

- ISO 21177 V2X security standard (January 2026) – Global standard for V2X certificate management enabling cross-border interoperability (US-EU-China alignment).

Typical user case – Urban Roads (Intersection Safety):

Tianjin, China deployed Huawei C-V2X RSUs at 200 intersections + Baidu Apollo V2X platform. Real-time warnings to approaching vehicles (red light violation warning, pedestrian detection, emergency vehicle preemption). Outcomes: Intersection collisions reduced 78% (12-month pilot), emergency response time reduced 35%, bus priority reduced transit delay 20%. 50,000 vehicles equipped with OBUs (aftermarket and embedded).

Typical user case – Highways (Work Zone Safety):

Ohio DOT deployed SWARCO C-V2X RSUs + roadside message signs for highway work zones (I-75 reconstruction, 30-mile corridor). In-vehicle warnings (alerts 1 mile before work zone, speed limit reduction, lane closure guidance) to OBU-equipped vehicles. Outcomes: Work zone speeds reduced 15 mph (less abrupt braking), rear-end collisions reduced 60%, worker injury claims reduced 45%. Payback period: 9 months (accident reduction alone).

Technical challenge addressed – Non-line-of-sight (NLOS) perception for autonomous vehicles. Onboard sensors (camera, radar, LiDAR) cannot see around corners, over hills, or through weather/fog. Vehicle-road collaboration provides “super-sensing” through roadside sensors (RSUs with camera/radar/LiDAR) transmitting detected objects to approaching vehicles (via C-V2X). Example: A child running into street from between parked cars: RSU camera detects child (200ft ahead, occluded from vehicle view), transmits alert to vehicle via C-V2X (20ms latency), vehicle initiates braking 1-2 seconds earlier than onboard sensors alone (avoiding collision). This is critical for Level 4/5 autonomous vehicles operating in complex urban environments.

4. Future Outlook & Strategic Implications (2026–2032)

Demand will be driven by six primary forces: (1) autonomous vehicle deployment (robotaxis, autonomous trucks requiring V2X redundancy for safety); (2) road safety mandates (China, EU, US requiring V2X in new vehicles 2027-2030); (3) congestion reduction (V2X-enabled traffic signal priority reducing delays 15-25%); (4) commercial vehicle efficiency (truck platooning reducing fuel consumption 5-10%); (5) V2G integration (EVs as grid assets requiring V2X connectivity); (6) infrastructure spending (US IIJA, EU Recovery Fund, China 14th Five-Year Plan).

Strategic recommendation for stakeholders: Automotive OEMs – embed C-V2X (3GPP Rel-16/17) in all vehicles by 2028 (cost $50-200 per vehicle) for safety and AV readiness. Transportation agencies – prioritize RSU deployment at high-risk intersections and work zones (highest ROI). Tech providers – develop interoperable V2X platforms (cross-OEM, cross-region) to accelerate adoption. Telecom operators – monetize 5G edge infrastructure for V2X services (private MEC for highway corridors). China’s early lead positions Huawei, Baidu, Tencent, Alibaba for global expansion (exporting V2X solutions to emerging markets). US and Europe must harmonize DSRC vs. C-V2X fragmentation (C-V2X winning due to China scale and 3GPP roadmap).

Exclusive forecast: The vehicle-road collaboration market will reach $12.8 billion by 2032, with equipment maintaining 55-60% share (RSUs largest sub-segment) and services growing to 45% by 2030. Urban roads will dominate (60-65% share), but highways will grow faster (25% CAGR) due to trucking efficiency and work zone safety ROI. China will remain largest market (40-45% global share by 2030), followed by US (20-25%) and Europe (15-20%). Huawei will lead global RSU market (30-35% share) with Baidu/Tencent/Alibaba in V2X software. US/European OEMs (GM, Ford, Volkswagen) and Tier-1s (Continental, Bosch, Aptiv) will capture OBU/embedded share. By 2030, 50% of new vehicles globally will have embedded C-V2X, with 30% of highway miles covered by RSUs. V2X will be a required feature for NCAP safety ratings (2028-2030), accelerating adoption.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp