Introduction: Addressing Container Leakage, Tamper Evidence, and Product Integrity

For pharmaceutical manufacturers, food packagers, and chemical companies, container closure integrity (CCI) is critical to product safety, shelf life, and regulatory compliance. Traditional screw caps, snap caps, and lug caps without liners cannot provide hermetic sealing – gas (oxygen), moisture, and microbial ingress degrades product quality (oxidation, hydrolysis, microbial growth). Leakage during transport (vibration, temperature, pressure changes) causes product loss, contamination, and customer complaints. Aluminum foil sealing gaskets (induction sealing liners) address these challenges with a composite structure – aluminum foil substrate laminated with thermoplastic adhesive layer – that bonds to container mouth (plastic, glass, metal) via electromagnetic induction or thermal conduction. The hermetic seal provides tamper evidence (visual indication of opening), barrier protection (gas, moisture, microbial), and extended shelf life (12–36 months). As pharmaceutical regulations tighten (USP page front 1207, container closure integrity testing), food safety standards (FDA, EFSA) require tamper-evident packaging, and e-commerce growth demands leak-proof shipping, demand for aluminum foil sealing gaskets is growing. Global Leading Market Research Publisher QYResearch announces the release of its latest report “Aluminum Foil Sealing Gasket – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Aluminum Foil Sealing Gasket market, including market size, share, demand, industry development status, and forecasts for the next few years.

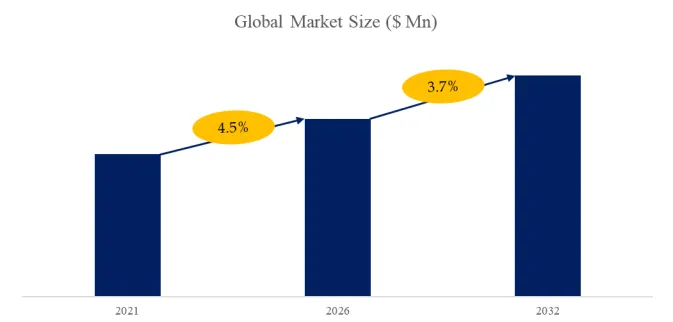

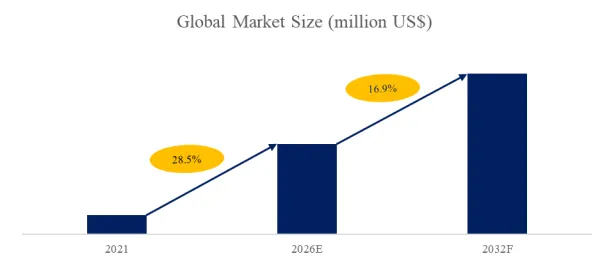

For packaging procurement managers, quality assurance directors, and container closure engineers, the core pain points include achieving hermetic seal (leak-free), tamper evidence (visual indication), and compatibility with container materials (HDPE, PET, PP, glass, metal). According to QYResearch, the global aluminum foil sealing gasket market was valued at US$ 61 million in 2025 and is projected to reach US$ 74.8 million by 2032, growing at a CAGR of 3.0% .

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/releases/6092884/aluminum-foil-sealing-gasket

Market Definition and Core Capabilities

Aluminum Foil Sealing Gasket is a composite sealing component consisting of aluminum foil substrate laminated with thermoplastic adhesive layer, designed for container closure through electromagnetic induction or thermal conduction. Core capabilities:

- Induction Sealing: Electromagnetic induction heats aluminum foil (eddy currents), melting thermoplastic adhesive layer. Adhesive bonds to container mouth (HDPE, PET, PP, glass, metal). Foil remains as barrier layer, liner peels off when cap removed (tamper evidence). Speed 100–1,000 bottles per minute.

- Barrier Properties: Oxygen transmission rate (OTR) <0.05 cc/m²/day (aluminum foil). Moisture vapor transmission rate (MVTR) <0.05 g/m²/day. Light barrier (UV, visible). Microbial barrier (sterility).

- Tamper Evidence: Foil liner bonded to container mouth – when cap removed, liner remains on container (visual indication of opening). Broken foil, torn liner indicates tampering.

- Container Compatibility: HDPE (high-density polyethylene) – most common. PET (polyethylene terephthalate). PP (polypropylene). Glass. Metal (aluminum, tinplate). PVC (polyvinyl chloride).

Market Segmentation by Gasket Type

- One-Piece (Push-Through) Liner (60–65% of revenue, largest segment): Foil liner bonded to container mouth, remains on container after cap removal. User pushes through foil with finger, tool, or straw. Tamper-evident (foil broken). Used for pharmaceuticals (oral liquids, syrups, suspensions), food (juices, sauces, oils), daily chemical (shampoo, lotion, detergent). Lower cost, simpler manufacturing.

- Two-Piece (Peel-Off) Liner (35–40% of revenue, fastest-growing at 4–5% CAGR): Foil liner bonded to pulpboard or foam backing. User peels off entire liner (foil + backing). Clean removal, no foil residue. Used for dry products (powders, tablets, capsules), high-value products (cosmetics, premium food). Higher cost, better user experience.

Market Segmentation by Application

- Pharmaceutical (35–40% of revenue, largest segment): Oral liquids (syrups, suspensions, solutions), oral solids (tablets, capsules, powders), topical (creams, ointments, gels), ophthalmic (eye drops), otic (ear drops), nasal (sprays), veterinary. USP page front 1207 (container closure integrity testing) requires hermetic seal, tamper evidence. Induction sealing liners standard for pharmaceutical packaging.

- Food (25–30% of revenue, fastest-growing at 4–5% CAGR): Juices, sauces (ketchup, mayonnaise, mustard, soy sauce), oils (olive, vegetable, coconut), dressings (salad, vinaigrette), condiments (hot sauce, barbecue sauce), baby food, nut butters (peanut, almond), honey, syrups, jams, jellies, pickles, olives. Tamper-evident packaging (FDA, EFSA) for food safety. E-commerce (online grocery, meal kits) requires leak-proof packaging.

- Daily Chemical (15–20% of revenue): Shampoo, conditioner, body wash, lotion, cream, gel, sunscreen, hand soap, dish soap, laundry detergent, cleaning products. Induction sealing prevents leakage during transport (e-commerce), extends shelf life (2–3 years).

- Pesticide (5–10% of revenue): Herbicides, insecticides, fungicides, rodenticides. Chemical resistance (aluminum foil, HDPE, PET). Child-resistant (CR) closures (ASTM D3475). Induction sealing prevents leakage, contamination.

- Others (5–10% of revenue): Automotive (oil, coolant, brake fluid, windshield washer fluid), industrial (lubricants, adhesives, solvents, paints, coatings), petrochemical.

Technical Challenges and Industry Innovation

The industry faces four critical hurdles. Container Material Compatibility – HDPE, PET, PP, glass, metal have different surface energies, requiring different adhesive formulations (EAA, EMA, EVA, PU, epoxy). Adhesive must bond to container mouth without delamination (peel strength >5–10 N/15mm). Induction Sealing Equipment – sealing requires induction cap sealer (1–10 kW, 50–200 kHz). Consistent seal strength across bottle-to-bottle variation (cap torque, container finish, foil liner alignment). Tamper Evidence & Child Resistance – foil liner must provide clear visual indication (broken foil) upon first opening. Child-resistant (CR) closures for pharmaceutical, pesticide, daily chemical (ASTM D3475, 16 CFR 1700). Sustainability – aluminum foil is recyclable (separate from plastic container). Paperboard backing (recyclable). Mono-material (PE) liners for recyclability (no foil). Induction sealing liner removal (clean removal) improves recyclability.

独家观察: Pharmaceutical & Food Fastest-Growing Segments for Induction Sealing Liners

An original observation from this analysis is the double-digit growth (4–5% CAGR) of pharmaceutical and food aluminum foil sealing gaskets due to USP page front 1207 (container closure integrity testing) for pharmaceuticals (oral liquids, topicals, ophthalmics) and tamper-evident packaging regulations for food (FDA, EFSA). E-commerce (online grocery, meal kits, supplement delivery) requires leak-proof, tamper-evident packaging. Pharmaceutical & food segments projected 70%+ of aluminum foil sealing gasket revenue by 2030 (vs. 60% in 2025). Additionally, two-piece (peel-off) liners for clean removal (no foil residue) are gaining share in premium food (organic, natural, specialty), cosmetics, and dry products (powders, tablets, capsules). Two-piece segment projected 45%+ of liner revenue by 2028 (vs. 35% in 2025).

Strategic Outlook for Industry Stakeholders

For CEOs, product line managers, and packaging investors, the aluminum foil sealing gasket market represents a steady-growth (3.0% CAGR), essential packaging component opportunity anchored by pharmaceutical regulations, food safety, and e-commerce growth. Key strategies include:

- Investment in pharmaceutical-grade induction sealing liners (USP page front 1207 compliant) for oral liquids, topicals, ophthalmics (fastest-growing segment).

- Development of two-piece (peel-off) liners for clean removal (no foil residue) for premium food, cosmetics, dry products.

- Expansion into sustainable liners (paperboard backing, mono-material PE, recyclable) for eco-friendly packaging.

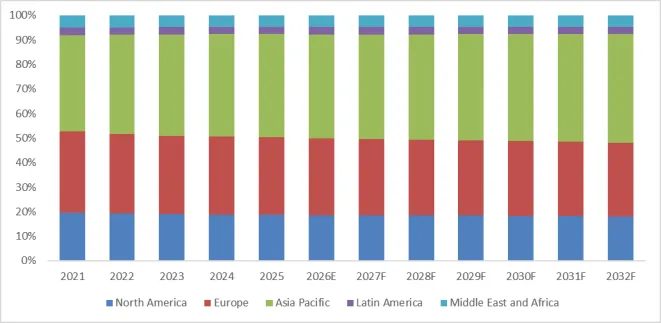

- Geographic expansion into Asia-Pacific (China, India, Southeast Asia) for pharmaceutical, food, daily chemical packaging growth; North America and Europe for regulatory compliance (USP, FDA, EFSA).

Companies that successfully combine hermetic seal, tamper evidence, and container compatibility will capture share in a $74.8 million market by 2032.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp