Global Leading Market Research Publisher QYResearch announces the release of its latest report, *“Detonation Controller – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”*. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Detonation Controller market, including market size, share, demand, industry development status, and forecasts for the next few years.

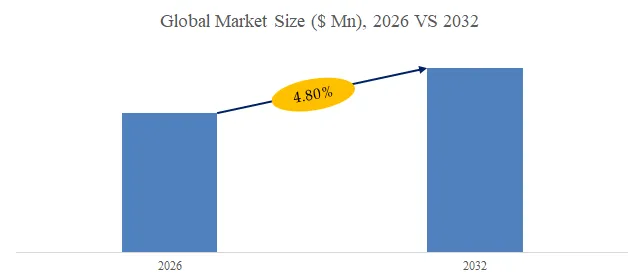

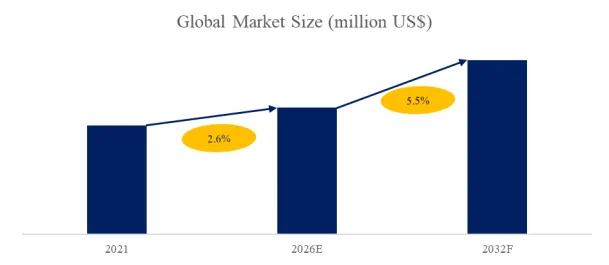

The global market for Detonation Controller was estimated to be worth US245millionin2025∗∗andisprojectedtoreach∗∗US245millionin2025∗∗andisprojectedtoreach∗∗US 385 million by 2032, growing at a CAGR of 6.7% from 2026 to 2032. Detonation controllers (also known as electronic detonators or blasting control systems) are electronic devices that precisely initiate explosion sequences in commercial blasting operations, replacing traditional safety fuse and detonating cord methods. These controllers offer millisecond-precise timing (typically ±0.1–0.5ms) to optimize fragmentation, reduce ground vibration, and improve blasting safety through remote initiation. They are essential in coal mining, oil exploration (seismic surveys), infrastructure construction (tunneling, quarrying, road cuts), geological exploration, and specialized firefighting (controlled demolition for forest firebreaks). However, distinct requirements between integrated detonation controllers (all-in-one units with built-in power and timing logic, for smaller operations) vs. split detonation controllers (separate control unit + multiple detonator modules, for large-scale, sequential blasting in mining and infrastructure) demand a deeper analytical lens across blasting scale, safety certification, electronic timing accuracy, and regulatory compliance.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5934728/detonation-controller

1. Market Valuation & Recent Trajectory (H2 2024 – H1 2026)

Supplementing the market baseline, recent six-month trends (Q4 2024 – Q1 2026) show a 4.3% sequential revenue increase in Q1 2026 compared to Q4 2025, driven by infrastructure stimulus in China (railway and highway expansion requiring rock blasting) and coal mine production recovery in India and Indonesia. Global unit shipments of detonation controllers reached approximately 1.2 million units (including both integrated controllers and split-system control modules) in 2025, with average selling prices ranging from 85(integratedcontroller,10–20detonatorcapacity)∗∗to∗∗85(integratedcontroller,10–20detonatorcapacity)∗∗to∗∗1,200 (split controller base unit with 100–500 detonator network capacity) . Notably, split detonation controllers captured 72% of market revenue in early 2026 (up from 67% in 2023), driven by large-scale coal mining, quarrying, and major infrastructure projects requiring hundreds to thousands of blasts per operation with precise sequencing.

2. Type Segmentation: Integrated vs. Split Detonation Controllers

As segmented by system architecture and application scale:

- Integrated Detonation Controller – Self-contained, portable unit combining timing logic, power source (internal battery), and detonator firing circuits in one enclosure. Typically supports 10–50 detonators per controller. Used in smaller operations: small quarries, geological exploration drilling, minor construction blasting, and specialized firefighting. Lower cost, simpler operation, fewer regulatory requirements. Dominant in smaller-scale mining and contractor blasting services.

- Split Detonation Controller – Distributed system: central control unit (programmable timer, user interface, safety interlock) connected to multiple remote detonator modules via twisted-pair bus, fiber, or wireless (in approved configurations). Supports 100–1,000+ detonators in a single network. Used in large-scale coal surface mining, massive infrastructure excavation (tunnel boring preparatory blasting), oil seismic exploration arrays. Offers advanced features (sequential timing down to 0.1ms intervals, misfire detection, blast simulation). Higher cost, requires trained personnel.

Depth Analysis Insight: Since Q3 2025, split detonation controller demand has grown at a CAGR of 7.8% (vs. 6.7% market average), driven by increasing blasting scale in coal mining (Australia’s Bowen Basin, China’s Inner Mongolia surface mines, India’s Singareni Collieries). A key technical challenge remains intrinsic safety certification for underground coal mining (ATEX, IECEx, MA certification in China): split controllers must prevent any spark or thermal ignition source in methane/coal dust environments. In Q4 2025, Wuxi Holyview Microelectronics and Norinco Group received updated MA (Mining Approval) certification for their integrated and split detonation controllers per new AQ 1049-2025 standard (coal mine electronic detonator systems) from China’s National Mine Safety Administration, requiring twice the previous electrostatic discharge (ESD) immunity (15kV vs. 8kV). Non-certified controllers are now restricted from China’s underground coal mines, accelerating market consolidation.

3. Application Segmentation, User Case & Coal Mining vs. Infrastructure Contrast

The report segments applications into:

- Coal Mine – Surface and underground coal mining. Largest application segment. Requires detonation controllers with intrinsic safety certification (especially underground), misfire detection, and ability to sequence hundreds of blasting holes per blast cycle (longwall mining development, overburden removal). Split detonation controllers dominate.

- Oil Exploration – Seismic surveying on land (vibroseis replaced by controlled explosive sources in some terrains) and oil well perforation. Requires portability (integrated controllers often adequate), extreme reliability (remote locations). Smaller segment fast-growing due to oil price recovery.

- Firefighting – Controlled demolition to create forest firebreaks (pre-detonation of controlled areas to deny fuel to advancing fires), avalanche control in mountainous regions. Requires portability and rapid deployment (integrated controllers). Small but stable segment.

- Geological Exploration – Core sample blasting in mineral prospecting (gold, copper, lithium). Integrated controllers dominate due to small shot sizes and remote field locations.

- Infrastructure Construction – Highway/railway tunnel boring (advance blasting), quarrying for aggregate, dam foundations, building excavation. Mix of integrated (small quarries, contractors) and split (large tunnel projects, major infrastructure).

User Case Example – Underground Coal Mine Digital Blasting Upgrade: A Chinese state-owned coal mine (Shanxi province, 4.5 million tonnes/year) upgraded from traditional safety fuse + detonating cord to split detonation controllers (Wuxi Holyview system, 500 detonator capacity, 0.5ms timing precision). After 12 months (data from February 2026 safety report), the mine achieved:

- 88% reduction in misfire incidents (from 0.24% of blasts to 0.03%)

- 45% reduction in face advance time per blasting cycle (2.5 hours to 1.4 hours) due to simultaneous instead of sequential hole initiation

- Improved coal fragmentation (50% less oversize boulders >500mm), reducing secondary breaking cost

- Zero safety incidents (no premature detonations) vs. 3 recordable incidents in previous year

The mine’s return on investment was 9 months based on productivity gains and safety incident reduction.

Coal Mining vs. Infrastructure vs. Oil Exploration Contrast: In coal mining (especially underground), priorities are intrinsic safety certification (ATEX/IECEx/MA), misfire detection (to avoid dangerous fumbling), and scalability (split controllers for >100 blasting holes). In infrastructure construction (tunnels, quarries, dams), priorities are portability (construction sites move), ruggedness (dust, moisture, impact resistance), and sequential timing accuracy (to control blast vibration and protect nearby structures). Split controllers dominate major infrastructure; integrated controllers dominate small contractor blasting. In oil exploration, priorities shift to remote operation (GPS-synchronized controllers for expansive arrays), low power consumption (battery operation for weeks in field), and data logging (to document blast parameters for clients). This depth analysis clarifies that coal mining accounts for 48% of split detonation controller revenue (largest segment), infrastructure construction represents 25% (growing with global stimulus), and oil exploration and geological exploration together account for 15%.

4. Policy, Safety Standards & Regulatory Landscape

Recent policy and safety standards updates significantly impact the detonation controller market. China’s AQ 1049-2025 (replacing 1049-2008, effective January 2026) applies to electronic detonator systems for coal mines, requiring: (1) ambient temperature range -20°C to +70°C (previously -10°C to +55°C), (2) ESD immunity ±15kV (previously ±8kV), (3) IP54 minimum enclosure rating (dust/water resistant), (4) 10-year storage life for electronics (previously 5 years). Suppliers lacking updated certification (e.g., some smaller Chinese manufacturers and most non-Chinese suppliers) are effectively excluded from China’s coal mining market (largest single national market).

Atmospheric protection regulations (EU, Australia) have also increased detonation controller adoption: blast vibration monitoring (required to avoid damage to neighboring structures) demands precise timing control (split controllers with sub-1ms accuracy), while traditional detonating cord cannot provide such precision.

Digital transformation mandates: India’s Coal Mines Digital Blasting Initiative (2025) requires all large surface mines (>5 million tonnes/year) to adopt electronic detonator systems with data logging by 2027—expanding detonation controller demand in India’s rapidly growing coal sector (Coal India Ltd. targets 1 billion tonnes by 2027).

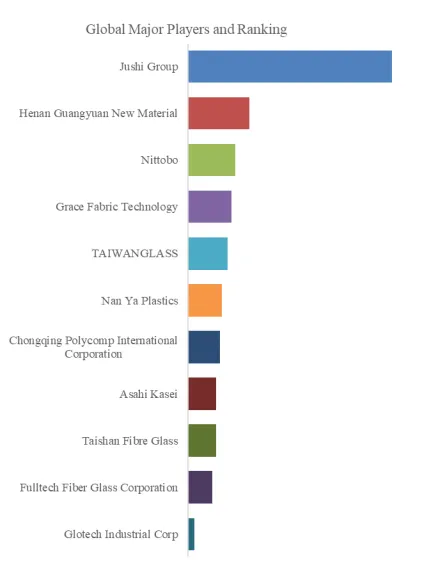

Key market participants include:

Wuxi Holyview Microelectronics Co., Ltd, Wuxi ETEK Microelectronics Co. Ltd, Poly Permanent Union Holding Group Limited, Beijing RGSC Technology Co., Ltd., Norinco Group, Guangxi Jinjianhua Industrial Explosive Materials Co. Ltd, ckbstech, shkcdz, lyzstech, Shanxi Huhua Group Co., Ltd.

Exclusive Observation – The China-Dominated Market and Consolidation: The detonation controller market is heavily China-centric, with all 10 listed participants being Chinese entities. Norinco Group (state-owned defense conglomerate) and Wuxi Holyview Microelectronics are the market leaders (estimated combined share 45–50%), benefiting from deep relationships with state-owned coal mining enterprises and early compliance with AQ 1049-2025. Wuxi ETEK and Beijing RGSC Technology (spin-offs from defense research institutes) hold the next tier (15–20% combined). Smaller suppliers (ckbstech, shkcdz, lyzstech) are less than 5% each, serving localized or non-coal markets (quarrying, firefighting, geological exploration).

Notably, non-Chinese suppliers (e.g., Orica, Dyno Nobel, Hanwha) have negligible presence in the detonation controller market as standalone products—they instead integrate detonation control functionality into broader electronic blasting systems (e-waste) with proprietary detonators. QYResearch’s report scope focuses on standalone detonation controllers (compatible with multiple detonator brands), a segment dominated by Chinese independents. We project consolidation in this market, with the top 4 players reaching 65–70% share by 2028 as AQ 1049-2025 compliance and scale advantages squeeze smaller suppliers.

5. Demand Forecast & Strategic Implications (2026–2032)

With a projected 6.7% CAGR, the Detonation Controller market will add approximately **US140million∗∗by2032,growingfrom140million∗∗by2032,growingfrom245 million in 2025 to $385 million. Unit volume will reach an estimated 1.9 million units by 2032 (up from 1.2 million in 2025, includes both integrated controllers and split-system control modules). The split detonation controller segment will outpace the market at 7.5% CAGR (revenue), driven by large-scale coal mining and infrastructure projects. The integrated segment will grow at 5.8% CAGR, maintaining unit volume leadership (65% of units) but at lower average selling price.

For mining operations engineers, blasting contractors, and safety regulators, the strategic considerations increasingly involve:

- System architecture selection (split controllers for >50 blasting holes per blast, integrated for small quarries, exploration, firefighting)

- Intrinsic safety certification (ATEX/IECEx/MA for underground coal mining)

- Blast timing precision (standard ±0.5–1.0ms adequate for fragmentation; sub-0.5ms required for vibration control near structures)

- Data logging & reporting (regulatory requirements increasingly mandate digital blast records for safety compliance)

- Supplier certification (AQ 1049-2025 compliant for China coal; check local approvals for each mining jurisdiction)

The depth analysis concludes that coal mining (China, India, Indonesia, Australia) remains the single largest market driver for detonation controllers, with China alone accounting for 55–60% of global demand. However, infrastructure construction (global highway, rail, tunnel projects, especially India’s Bharatmala, US Bipartisan Infrastructure Law, ASEAN road/rail corridors) is the fastest-growing application (8–9% CAGR), as urbanization and connectivity investments accelerate. Oil exploration segment will recover with oil prices >$70/bbl, growing at 7–8% CAGR. Manufacturers who invest in AQ 1049-2025 compliant controllers (for China coal access), GPS-synchronized split systems (for seismic exploration arrays), and intrinsically safe wireless detonator communication (emerging technology to reduce cabling effort and misfire risk) will capture the highest margins. Additionally, the emerging smart mine integration (detonation controllers feeding blast data into mine planning software for fragmentation optimization) could create a software/services revenue stream for leading suppliers (Norinco, Wuxi Holyview) beyond hardware sales, representing a potential margin-accretive opportunity through 2030.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp