QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “All Electric SUV- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global All Electric SUV market, including market size, share, demand, industry development status, and forecasts for the next few years.

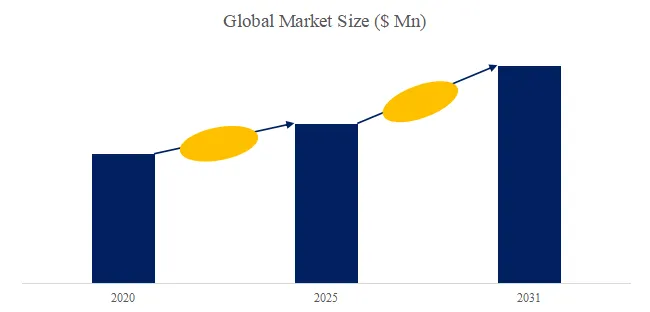

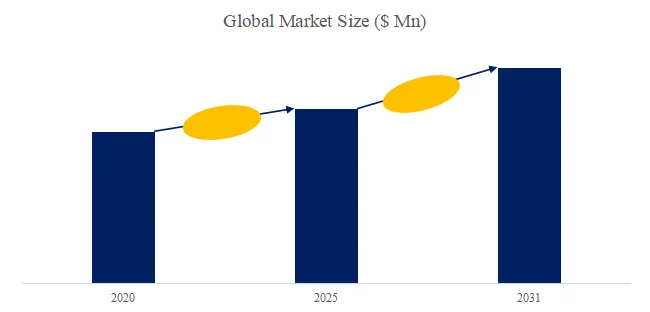

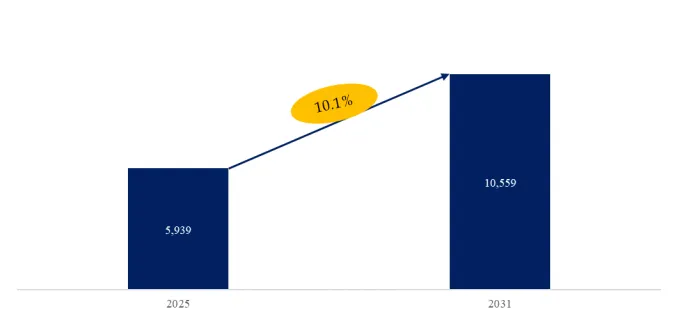

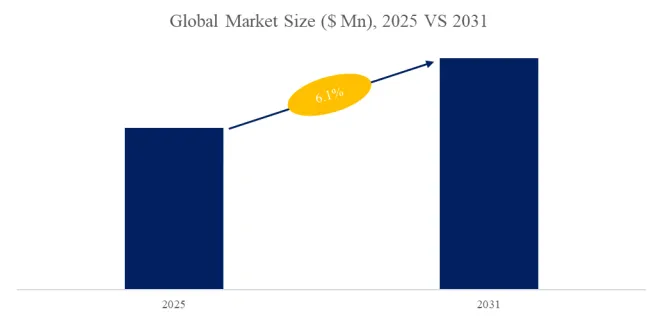

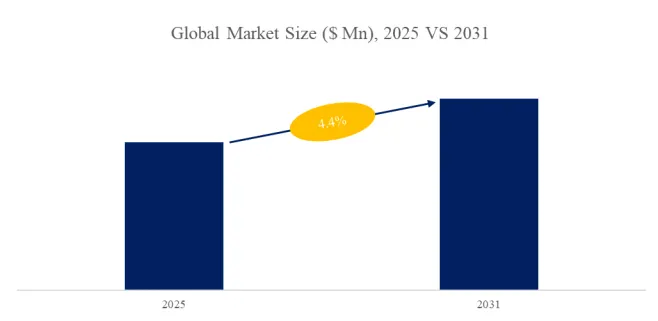

The global market for All Electric SUV was estimated to be worth US$ 1802 million in 2025 and is projected to reach US$ 4346 million, growing at a CAGR of 13.6% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5543757/all-electric-suv

1. All Electric SUV Introduction

The core demands and business opportunities for All Electric SUVs can be summarized into four key points: First, the anxiety over range and charging drives opportunities for battery technology innovation (such as solid-state batteries) and the deployment of ultra-fast charging networks. Second, the intelligent experience (including advanced driver-assistance systems and smart cockpits) has become a new core purchasing driver and a source of profitability for software services. Third, platform-based vehicle manufacturing enables optimization of R&D costs and opens up space for personalized, modular product definition. Fourth, ecosystem expansion based on the vehicle’s global electronic and electrical architecture, such as V2G (vehicle-to-grid) and data value-added services, fosters innovative business models in the aftermarket.

Figure1: All Electric SUV Product Picture

Based on or includes research from QYResearch:

2. All Electric SUV Development Factors

2.1. The Improvement of Charging Infrastructure Drives the Rapid Development of All Electric SUVs

The rapid improvement of charging infrastructure has become a core driving force behind the rapid development of All Electric SUVs, prompting consumers to shift from extended-range vehicles to pure electric powertrains. This transformation has completely eliminated the long-standing “charging anxiety” that users faced, amplifying the inherent drawbacks of extended-range vehicles, such as high fuel consumption and noise when in a depleted state. In terms of charging efficiency and convenience, the widespread adoption of the 800V high-voltage platform marks a revolutionary breakthrough in All Electric SUV charging technology. Currently, mainstream models can charge 400-600 kilometers in 10-15 minutes, and some models support ultra-fast charging with a peak charging power of over 360kW, significantly reducing charging time. The experience now approaches or even surpasses the convenience of traditional refueling. Even more disruptive is the battery swap model, represented by NIO, which further improves charging efficiency. It only takes 3-5 minutes to swap the battery and depart with a full charge, far surpassing the waiting time at fuel stations. This has become the preferred solution for All Electric SUV users on long-distance trips. By 2025, NIO’s battery swap station network has surpassed 3,000 stations, with plans to cover most county-level administrative areas across the country within the year. Furthermore, NIO is collaborating with other companies to standardize battery swapping, enhancing the network effect. Meanwhile, the increasingly complete charging network provides solid support for All Electric SUVs: the total number of charging infrastructure nationwide has surpassed 13.7 million units, with over 3.9 million public charging stations, showing significant growth; highway service areas have a charging station coverage rate of over 98%, with more than 38,000 charging stations built, achieving near-total coverage; the charging infrastructure coverage rate in counties exceeds 97%, while coverage in townships reaches over 76%, and the number of public and private charging stations in cities continues to grow steadily, meeting daily commuting and long-distance travel needs. The accelerated construction of these infrastructures has not only broken the charging bottleneck but also eliminated the traditional advantages of extended-range vehicles, such as “no range anxiety,” highlighting the inherent advantages of All Electric SUVs in terms of low energy consumption, low noise, and high efficiency. This has driven a rapid increase in the market share of All Electric SUVs, making them the first choice for consumers in family and travel vehicles.

2.2. The Comprehensive Competitiveness of All Electric SUV Products Completely Surpasses Alternative Routes

The comprehensive leap in the product capabilities of All Electric SUVs has become a key driving force for their rapid development and for surpassing fuel and extended-range vehicles in user experience. This transformation stems not only from the structural advantages of the pure electric platform but also from leading factors across multiple dimensions, including lifetime operating costs, space and driving comfort optimization, and the practicality of technical specifications. In terms of lifetime operating costs, All Electric SUVs have a simpler structure and do not require engines or complex transmission systems. The average annual maintenance cost is only about 500-800 RMB, far lower than the 1,500-2,000 RMB maintenance cost of extended-range SUVs, which need to maintain both the electric and fuel systems. The maintenance items mainly focus on battery health checks, brake systems, and air conditioning filters, with longer cycles and lower costs. Meanwhile, the electricity cost per kilometer is only 0.06-0.3 RMB (home charging with off-peak electricity as low as 0.07 RMB/km, with mainstream models consuming 13-15kWh per 100 km, leading to annual energy costs of only 1,200-3,000 RMB based on 20,000 km/year), which is significantly lower than the fuel consumption costs of fuel vehicles or extended-range vehicles when their electric power runs out. This results in significant long-term ownership cost advantages, further enhancing the economic appeal of All Electric SUVs. In terms of space and driving comfort optimization, the pure electric platform eliminates the need for engines, fuel tanks, and exhaust systems, allowing the front trunk to be converted into a large front storage space (some models have a capacity of over 200-300 liters). The vehicle’s wheelbase is utilized more efficiently, offering more spacious seating and storage capacity, especially in large three-row configurations, which perfectly meet the needs of multi-person families. The third-row legroom easily exceeds 1 meter, the seat comfort is comparable to the first row, and the total front and rear trunk volume can easily accommodate more than 10 suitcases, solving the problem of insufficient luggage space when fully loaded. The pure electric drivetrain naturally provides exceptional quietness (NVH performance is superior to fuel and extended-range vehicles), and the linear smooth acceleration significantly improves the comfort of long-distance family trips, far surpassing the noise and vibrations from the generator when the extended-range vehicle is in operation. In terms of technical specifications, mainstream large All Electric SUVs in 2025 will have a CLTC range generally exceeding 600-800 km (high-end models exceeding 800 km). With the improvement of battery energy density, lightweight design, and efficient thermal management systems, energy consumption performance is better, and actual mileage achievement rates are higher, effectively eliminating range anxiety. The widespread adoption of the 800V high-voltage platform further enhances charging efficiency, supporting 10-15 minute quick charges to add 300-400 kilometers. Combined with the increasingly complete charging network, All Electric SUVs now lead in daily commuting and long-distance travel. These product advancements not only highlight the inherent advantages of All Electric SUVs in terms of efficiency, comfort, and practicality but also drive their emergence as the first choice for family users, pushing the market from extended-range vehicles to the mainstream adoption of All Electric SUVs.

2.3. Market Demand Shifts Towards Full-Cycle Experience, Driving the Rapid Development of All Electric SUVs

The fundamental shift in market demand towards a “full-cycle experience” has become the core driving force behind the rapid development of All Electric SUVs and the creation of vast market space. This transformation arises from the change in consumer car purchase decision-making logic, from blindly pursuing single parameters such as range and acceleration performance to more rational, comprehensive considerations of the entire lifecycle experience, including car purchase, usage, maintenance, and second-hand value retention. Additionally, the rigid demand for family travel scenarios further amplifies the unique advantages of All Electric SUVs. In terms of shifting from parameter comparison to prioritizing experience, early electric vehicle consumers often focused on “range number games” and “0-100 acceleration rankings.” However, by 2025, the market has matured, and consumer awareness has become more rational. According to surveys by institutions such as J.D. Power, over 70% of potential users now consider charging efficiency, smart cabin experience, space comfort, long-term operating costs, and second-hand value retention as the primary decision-making factors. All Electric SUVs, with their innate quietness (NVH performance 20-30 dB better than extended-range/fuel vehicles), linear smooth acceleration, intelligent connectivity systems (such as the HarmonyOS ecosystem, DiLink large screens), and electricity costs as low as 0.1 RMB/km, now lead in the full-cycle experience. Especially in maintenance, the annual cost of pure electric vehicles is only 500-800 RMB, and their second-hand residual value rate is 5-10% higher than that of extended-range vehicles, completely overturning the old logic of “parameters reign supreme” and making All Electric SUVs a “true fragrant choice” for consumers. In family travel scenarios becoming a necessity, with the continuous effects of the two-child policy and the shift of China’s family structure towards multi-person and multi-generation living, the proportion of two-child/three-child families has risen to over 35%, and the rate of self-driving trips has significantly increased (with a remarkable rise in travel spending by elderly users). Consumers have a strong demand for “large three-row” or “large six-seat” SUVs that can meet the comfortable travel needs of the whole family. The pure electric platform, which does not require the layout of engines and fuel tanks, transforms the front trunk into a large front storage space (200-300 liters), with higher wheelbase utilization, offering third-row legroom exceeding 900mm, optimized seat height, and luxurious configurations such as independent heating/ventilation. Meanwhile, when fully loaded, the luggage space is ample, completely solving the problem of “fit but not enough” in extended-range/fuel models. By 2025, the penetration rate of large three-row All Electric SUVs will increase from less than 5% to over 18%, with sales growth far exceeding that of extended-range and plug-in hybrid counterparts (such as NIO’s new ES8, Leado L90, and Li Auto i8 models, all seeing explosive order numbers). These models precisely match high-frequency scenarios such as weekend family self-driving and long-distance travel, further strengthening the inherent advantages of All Electric SUVs in terms of quietness, space flexibility, and smart family ecosystem. This market demand shift not only opens up a full-price market space for All Electric SUVs, from economical to high-end models, but also signifies the shift from the “range anxiety era” to the “experience-first era,” driving All Electric SUVs to become the mainstream choice for family vehicles.

2.4. The Rise of the All Electric SUV Market: Cost Reduction and Intense Competition Drive Technological Popularization and Industrial Transformation

The rapid development of All Electric SUVs is driven by the dual forces of cost reduction and intense market competition. These factors have not only accelerated their market adoption and technological iteration but have also deeply reshaped the structure of the new energy vehicle industry. In terms of battery costs, with the global supply chain optimization, the significant drop in prices of raw materials like lithium and cobalt, and the emergence of large-scale production effects, the overall manufacturing cost of electric vehicles continues to decrease. This directly promotes the process of technological equality, enabling advanced features that were once limited to high-end models, such as 800V high-voltage platforms, advanced driving assistance systems (including NOA city navigation), and lidar hardware, to rapidly spread to mid- and low-priced models. For example, in the 200,000 RMB price segment, consumers can easily purchase mid-to-large All Electric SUVs equipped with the 800V architecture, supporting both highway and city NOA, which not only enhances charging efficiency and range performance but also lowers the entry barrier, allowing more ordinary consumers to enjoy the convenience and fun of electric mobility. At the same time, the pure electric mid-to-large SUV market is viewed by many automakers as a strategic battleground. This niche market, with its broad market scale, strong growth potential, and high added-value attributes, has become the core platform for brand image enhancement and technological showcase. Major manufacturers such as Li Auto, NIO, Xpeng, and Xiaomi have concentrated resources to launch competitive models like the Li Auto L8, Xpeng G7, and Xiaomi SU7. These products compete fiercely in areas such as smart cabins (with multi-screen interaction, AI voice control), range (up to 700 km or more under CLTC conditions), performance (0-100 km/h acceleration in under 4 seconds), and safety features (such as full-scenario perception fusion systems), while further compressing profit margins through price wars. Ultimately, this benefits consumers by offering more cost-effective choices and drives the entire All Electric SUV ecosystem toward a more mature and inclusive direction. In conclusion, these intertwined development factors have jointly ushered in the golden age of the transformation of All Electric SUVs from niche markets to the mainstream, injecting strong momentum into the sustainable transportation transition.

3. All Electric SUV Development Trends

3.1. The All-Electric Midsize and Large SUV Market is Entering a New Era of “Multi-Power Competition

The all-electric SUV market is undergoing a profound transformation from the long-standing dominance of the Tesla Model Y to a structure of “multi-power competition.” It has now formed an intense competitive landscape featuring new forces brands represented by NIO’s Ledao L90, Xpeng’s G7, Xiaomi’s YU7, and Li Auto’s i8, as well as the full entry of traditional automakers’ premium sub-brands. These brands cover a broad price range from 150,000 to 400,000 RMB, encompassing almost all mainstream consumer demand scenarios. Meanwhile, each automaker is deploying distinctly differentiated competitive strategies based on their core strengths. Xpeng Motors continues to strengthen its leading position in high-level intelligent driving, committed to providing users with a safer and more convenient full-scenario NOA intelligent driving experience. Xiaomi Auto relies on its “Human x Car x Home” full ecosystem strategy, deeply integrating smartphones, smart home devices, and vehicles to build a unique usage loop. NIO consistently reinforces its hold on the premium all-electric user mindset with its parallel charging and battery-swapping energy replenishment system and user community operations. Li Auto, through its family-oriented positioning and strategic transition from extended-range to all-electric, is further enriching its product matrix. Although the Tesla Model Y still maintains a significant market position relying on its global brand influence and technological accumulation, its single model struggles to sustain its past overwhelming advantage when confronted with a siege of products from multiple brands, categories, and price segments. Looking ahead, the all-electric SUV market will gradually form a stable “1+N” competitive pattern, where Tesla continues to hold a major pole, while 2 to 3 leading Chinese brands successfully ascend to the first tier by leveraging their unique advantages in smart technology, user experience, energy replenishment systems, or ecosystem integration, jointly dominating market discourse with Tesla. This multi-power, differentiated coexistence will not only drive rapid technological iteration in the industry but also bring consumers continuously upgraded product capabilities and better choices, marking the formal entry of China’s all-electric SUV industry into a new, mature, open, and vibrant stage of development.

3.2. All-Electric SUVs Moving Towards an Era of “Technology Democratization

The core competition in all-electric SUVs has comprehensively shifted from the early battles over range and basic performance to the rapid dissemination and popularization of high-end technologies, formally entering the era of “technology democratization.” The fundamental driver of this shift lies in the continuous maturation of the local supply chain and the significant reduction in manufacturing costs, enabling cutting-edge features once confined to luxury models, such as 800V high-voltage platforms and high-level intelligent driving assistance systems, to accelerate their penetration into the mainstream 200,000 to 300,000 RMB market. Multiple mainstream automakers, including BYD’s brands Denza, Yangwang, and Fangchengbao, as well as Xiaomi, Zeekr, and Chery’s Exeed Sterra, have made the full-domain 800V high-voltage architecture standard for their mid-to-high-end all-electric SUVs, achieving a substantial increase in charging efficiency and revolutionary optimization of the energy replenishment experience. Simultaneously, intelligent configurations like high-level driving assistance, cloud-based intelligent chassis systems, and AI-powered cabins are gradually trickling down from flagship models priced around a million RMB to a broader user base. Relevant statements from the Ministry of Industry and Information Technology indicate that during the “14th Five-Year Plan” period, China has built the world’s most complete and resilient new energy vehicle industry and supply chain system, with electrification accelerating its integration with intelligent and connected features, transforming first-mover advantages into industrial leadership. Official actions by multiple automakers further corroborate this trend: premium brands have taken the lead in making 800V platforms standard across their lineups and, through scaled production and technological iteration, are continuously extending these core capabilities to more accessible price points. Future all-electric SUVs will no longer use “feature stacking” as their selling point but will be characterized by the democratization of technology as their essence, allowing more consumers to enjoy near-luxury-level replenishment speed, ride quality, and intelligent interaction in daily usage scenarios. This will thoroughly break down the previous market barrier of “high price equals high configuration,” propelling the entire category towards a more balanced, efficient, and intelligent evolution.

3.3. User Perception Upgrade Driven by Full-Cycle Experience

As the market matures and technology advancesthe competitive focus is shifting from single-parameter comparisons to the complete user experience covering purchase, usage, and residual value. User attention on energy replenishment efficiency is no longer limited to increasing range but places greater emphasis on the convenience and efficiency of charging infrastructure and service networks. Fast-charging technology is becoming a core factor in enhancing the all-electric SUV experience. Traditional range anxiety is gradually being alleviated through diverse energy replenishment solutions such as high-voltage fast charging, intelligent charging network deployment, and battery swap modes. These changes, which enhance convenience for users in both daily and long-distance travel, are defining the future user perception experience of all-electric SUVs. Meanwhile, users are beginning to more rationally consider full-cycle costs and long-term usage feelings in their purchase decisions, including dimensions like energy consumption costs and maintenance convenience. This is also prompting automakers to expand their focus from singular performance metrics to comprehensive service capabilities throughout the entire vehicle lifecycle. Official automaker initiatives and corporate deployments of self-built charging networks and smart energy services clearly demonstrate the trend of strategic planning centered around the user’s full-cycle experience. Therefore, the future development of all-electric SUVs will place greater emphasis on the comprehensive optimization of replenishment experience and cost efficiency, enabling users to enjoy a convenient, efficient, and low-friction vehicle ecosystem after purchase. This will drive the entire all-electric SUV market towards a more mature and user-experience-led direction of evolution.

4. Leading Manufacturer in the Industry

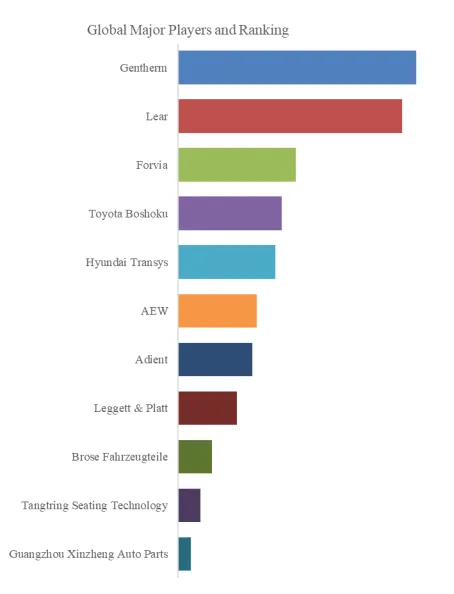

4.1. Porsche

Porsche, as a manufacturer focused on high-end sports cars, centers its core business on the design and production of luxury models that blend classic sports-car heritage with modern innovation, spanning a complete product portfolio from two-door sports cars to sporty sedans and versatile SUVs. The company adheres to a flexible powertrain strategy by offering efficient internal-combustion engines, powerful plug-in hybrid systems, and fully electric drivetrains to meet the diverse driving needs of customers around the world, while continuous technological advancement and extensive personalization options further strengthen the brand’s distinctive positioning in performance, handling, and everyday usability.

Porsche’s All Electric SUV lineup is currently led by the Macan electric series, which is developed on a dedicated all-electric platform and includes multiple regular models such as the rear-wheel-drive entry version, the all-wheel-drive Macan 4, the Macan 4S, and the high-performance Macan Turbo. These models emphasize sports-car-like driving dynamics, long-distance practicality, and highly efficient charging capability, while customers may further configure highly customized specifications through the Porsche Exclusive Manufaktur program, enabling personalized selections ranging from exterior paint and carbon-fiber elements to interior details. In addition, the all-new All Electric Cayenne has now been officially launched; as a larger-size All Electric SUV, it likewise offers both a standard version and a high-performance Turbo version and can be tailored through official customization programs to create unique equipment combinations, further expanding the diversity of Porsche’s All Electric SUV offerings.

4.1.1. Key Features of Macan EV

The Porsche Macan EV is the brand’s first premium All Electric SUV, built on an advanced 800-volt all-electric platform architecture and equipped with a 100 kWh lithium-ion battery. It supports maximum 270 kW fast charging and features combined charging functionality that enables efficient parallel charging on 400-volt charging stations, requiring only 21 minutes to charge from 10% to 80%. The model range consists of the Macan 4 and Macan Turbo, both featuring dual-motor all-wheel-drive systems: the former delivers a maximum output of 300 kW and peak torque of 650 Nm, accelerates from 0–100 km/h in 5.2 seconds, and achieves a WLTP range of 613 km, while the latter offers a maximum output of 470 kW and peak torque of 1130 Nm, completes 0–100 km/h in just 3.3 seconds, and provides a WLTP range of 591 km. With body dimensions of 4784/1938/1622 mm and a wheelbase of 2893 mm, it is positioned as a midsize coupé-style SUV. The exterior preserves the streamlined design of the combustion-engine version while adopting a closed-off grille and split-headlight layout, and the interior continues the Taycan-inspired tri-screen T-shaped cockpit design with smartphone integration. The front and rear luggage compartments offer flexible practicality, with an 84-liter front trunk and a rear cargo capacity expandable from 480 to 1348 liters depending on the variant. The rear axle is equipped with a silicon-carbide pulse inverter to improve efficiency, delivering a comprehensive blend of sports-car-grade dynamic handling, long-range practicality, and luxury-level comfort and equipment.

4.2. Seres Auto (HUAWEI)

Seres Auto, through deep cross-industry collaboration with Huawei, leverages the strengths of both parties to jointly design, develop, and manufacture high-end intelligent electric vehicles, providing users with smart luxury mobility solutions under the AITO brand. The company focuses on new energy vehicles as its core business, covering the research, development, and production of key electrification systems as well as complete-vehicle sales and services. It adheres to a software-defined-vehicle strategy and builds a fully connected automotive ecosystem, with AITO-series models equipped with Huawei’s advanced intelligent cockpit and driving technologies. These vehicles emphasize safe and reliable range-extended electric and high-voltage all-electric platforms, aiming to drive the transformation of automotive energy and create an intelligent mobile lifestyle.

Seres Auto’s All Electric SUV lineup is primarily represented by the AITO series, with current regular models including the AITO M8 All Electric version, a flagship midsize-to-large family-oriented intelligent All Electric SUV available in five-seat or six-seat configurations. It is built on an 800-volt high-voltage all-electric platform that supports ultra-fast energy replenishment and highly efficient electric drive, and is equipped with lidar and an advanced intelligent driving system. The interior offers generous and comfortable space, with seats supporting multi-way adjustment and zero-gravity mode, while the air-suspension system ensures both handling stability and a refined, luxurious ride experience. At the same time, the AITO M5 All Electric version and AITO M9 All Electric version also belong to the All Electric SUV category, with the former positioned as a city-performance All Electric SUV that emphasizes high performance and intelligent interaction, and the latter positioned as a full-size flagship All Electric SUV focused on ultimate luxury and advanced technological configuration. All All Electric models are developed on a unified platform to meet the diverse all-electric mobility needs of family users across multiple scenarios.

4.2.1. Key Features of Aito M8

The AITO M8 All Electric version is a midsize-to-large family-oriented flagship intelligent All Electric SUV with body dimensions of 5190×1999×1795 mm and a wheelbase of 3105 mm, offering flexible five-seat or six-seat layouts and a spacious, luxurious cabin. The second-row seats support multi-directional electric adjustment, electric leg rests, and zero-gravity mode, while both the front and second rows feature Nappa leather upholstery with ventilation, heating, and massage functions to create a mobile luxury lounge experience. Powered by Huawei’s DriveONE 800-volt high-voltage All Electric platform, it supports single-motor rear-wheel drive or dual-motor all-wheel drive configurations and is equipped with a 100 kWh “Whale” battery, enabling ultra-fast charging and efficient all-electric performance. Its intelligent features include Huawei’s advanced ADS assisted-driving system with lidar, multiple millimeter-wave radars, and high-resolution cameras, supporting omnidirectional collision prevention, urban and highway navigation assistance, and valet parking. The interior integrates a One-Glass triple-screen layout, AR-HUD head-up display, and HUAWEI SOUND audio system, while the closed dual-chamber air suspension and continuously variable damping shock absorbers ensure both ride comfort and handling stability. Practical storage solutions include an electric front trunk, a multifunctional cooling-and-heating compartment, and a flexible folding rear cargo area, fully meeting the needs of long-distance family travel and multi-scenario daily use, while highlighting the integration of zero-emission all-electric driving with technological luxury.

4.3. Li Auto

Li Auto focuses on the design, research and development, manufacturing, and sales of premium intelligent electric vehicles, providing safe, convenient, and comfortable mobility solutions for family users through product innovation, technological breakthroughs, and business model optimization. Centered on the needs of family users, the company adheres to a dual-energy strategy that advances range-extended electric and high-voltage all-electric technologies in parallel. Its core product lineup includes the L Series range-extended electric SUVs and the MEGA all-electric MPV, models that emphasize large interior space, multi-seat layouts, intelligent driving capabilities, and “magic carpet” air suspension systems. These vehicles are designed to address the key challenges of long-distance family travel and daily mobility, while the self-developed ultra-fast-charging network further enhances energy-replenishment convenience, creating a “mobile home” experience of happiness for users. Li Auto’s All Electric SUV lineup is centered on the i Series, with the first model, Li Auto i8, already launched as a six-seat family-oriented All Electric SUV. It adopts an 800-volt high-voltage platform and 5C ultra-fast-charging battery technology, and is equipped with lidar and an advanced intelligent driving system. The vehicle design prioritizes aerodynamics and a low drag coefficient, while offering a spacious interior and a comfortable riding experience. Future plans include the introduction of additional i Series models such as the i6, forming a complete All Electric SUV matrix that, together with the L Series and MEGA, meets the diverse all-electric mobility needs of different family users.

4.3.1. Key Features of Li i8

Li Auto i8 is Li Auto’s first family-oriented six-seat All Electric SUV, built on an all-new 5C all-electric platform and equipped with a self-developed silicon-carbide electric drive system and a 97.8 kWh ternary-lithium ultra-fast-charging battery. It supports 5C ultra-fast-charging technology, enabling an additional 500 kilometers of range with just 10 minutes of charging and effectively addressing range anxiety. The vehicle adopts an intelligent dual-motor all-wheel-drive layout with front and rear motors, delivering a combined output of 400 kW and peak torque of 660 Nm, achieving 0–100 km/h acceleration in 4.5 seconds. It is equipped with a dual-chamber “magic carpet” air suspension and multiple road-condition driving modes, offering a well-balanced combination of SUV off-road capability and refined driving comfort. With a drag coefficient as low as 0.218, the exterior integrates a yacht-inspired streamlined profile, three-dimensional star-ring lighting, and Li Auto’s signature clean design language. The interior emphasizes a wraparound luxury layout, full-vehicle dual-layer acoustic glass for enhanced cabin quietness, zero-gravity seats in the second row, and family-oriented features such as an intelligent refrigerator, while the AD Max intelligent driving system and the VLA driver large model enable defensive driving capability, natural-language interaction, and proactive safety protection. Overall, the model delivers class-leading interior space, an intelligent energy-replenishment network, and a premium private mobility experience tailored for multi-member families.

4.4. NIO

NIO focuses on the design, research and development, manufacturing, and delivery of premium intelligent all-electric vehicles, providing users with high-performance driving experiences and an enjoyable lifestyle through innovative technology platforms and a comprehensive service ecosystem. The company adheres to a user-centric philosophy and is building a global intelligent electric mobility ecosystem, with its vehicle lineup equipped with advanced intelligent cockpits, intelligent driving assistance systems, and the NOMI intelligent assistant. Together with NIO’s self-developed battery-swap network and charging infrastructure, these capabilities enable convenient and efficient energy-replenishment services, supporting the advancement of sustainable intelligent mobility while creating a warm and engaging community experience for users. NIO’s All Electric SUV lineup consists entirely of regular production models, including the ES8, positioned as an all-scenario technological flagship All Electric SUV offering six-seat or seven-seat configurations with an emphasis on generous interior space and luxury appointments; the ES6, positioned as an intelligent all-round midsize All Electric SUV that focuses on high-performance dual-motor drive, air suspension, and precise handling, with an interior featuring an embracing design and the Queen Passenger Seat to create a comfortable mobile space; the EC6, an intelligent coupe-style All Electric SUV that adopts a fastback silhouette and low-drag design to highlight sporty aesthetics and efficient all-electric performance; and the ES7 and EC7, which belong to the midsize-to-large All Electric SUV segment, with the former delivering a premium five-seat luxury experience and the latter enhancing dynamic driving pleasure through its coupe-inspired styling. All models are based on the NT platform, support advanced intelligent driver-assistance functions and battery-swap architecture, and comprehensively meet the diverse All Electric mobility needs of families across multiple usage scenarios.

4.4.1. Key Features of ES6

NIO ES6 is an intelligent electric midsize All Electric SUV positioned as a high-performance luxury family vehicle, with body dimensions of 4854×1995×1703 mm and a wheelbase of 2915 mm. It features a five-seat layout with a spacious and comfortable interior, where the second-row seats support electric adjustment and multi-angle backrest recline, complemented by the Queen Passenger Seat and Nappa leather upholstery to create a luxurious mobile living-room experience. The exterior adopts NIO’s X-Bar family design language with heartbeat-style taillights, hidden intelligent door handles, and frameless doors, achieving an elegant yet dynamic low-drag profile. Powered by the second-generation NT2.0 platform, it offers a dual-motor intelligent all-wheel-drive system combining a front induction asynchronous motor with a rear permanent-magnet synchronous motor for instant response and high-efficiency all-electric performance, while supporting air suspension and Continuous Damping Control (CDC) to ensure precise handling and refined ride comfort. Intelligent features include the NOMI Mate smart system, a panoramic digital cockpit, and AR-HUD head-up display, with the advanced NOP+ assisted-driving system covering both urban and highway scenarios. Equipped with lidar and the Aquila super-sensing system, the vehicle delivers proactive safety and intelligent protection. Energy replenishment is enabled through NIO’s battery-swap architecture, supporting rapid battery swapping and high-power charging, while versatile storage solutions — including front and rear luggage compartments and multiple flexible in-cabin storage areas — fully meet the needs of daily commuting and long-distance family All Electric travel, highlighting the fusion of zero-emission driving pleasure with technological luxury.

4.5. Xiaomi

Xiaomi, as a consumer electronics and intelligent manufacturing company centered on smartphones, smart hardware, and its IoT platform, focuses its core business on the global expansion of smartphones, the deep interconnection of its AIoT ecosystem, and the diversified growth of internet services, while accelerating innovation-driven businesses such as smart electric vehicles through its “Human x Car x Home” full-ecosystem strategy. The company adheres to a technology-driven and user-experience-oriented approach, building a complete intelligent connectivity system that extends from smartphones to smart homes and further to electric vehicles, with the goal of enabling users worldwide to enjoy an efficient and convenient lifestyle empowered by technology.

Xiaomi’s All Electric SUV lineup is centered on the YU7 series, a midsize-to-large premium intelligent electric SUV family that offers regular models including the standard rear-wheel-drive version, the Pro long-range version, and the Max high-performance all-wheel-drive version. These models emphasize powerful single- or dual-motor drive systems, advanced intelligent chassis tuning, and a highly efficient electrified architecture, combining sports-car-level acceleration with the practicality of SUV interior space. Through official customization services, customers may further select highly personalized configurations, including exclusive exterior paint colors, distinctive quilted interior craftsmanship, and other bespoke design elements, to better satisfy individualized preferences for both exterior styling and interior details.

4.5.1. Key Features of YU7

The Xiaomi YU7 is the second midsize-to-large All Electric SUV under Xiaomi Auto, positioned as a premium intelligent electric model with a price range from 253,500 to 329,900 yuan. It is available in multiple single-motor rear-wheel-drive and dual-motor all-wheel-drive variants and is equipped with 96.3 kWh or 101.7 kWh high-capacity lithium-ion battery packs supplied by CATL. The 96.3 kWh version corresponds to single-motor models and delivers CLTC ranges of up to 820 km, 810 km, or 725 km, while the 101.7 kWh version corresponds to dual-motor models with ranges of 760 km, 750 km, or 670 km. Overall energy consumption is maintained at approximately 13 kWh per 100 km, with optimized battery energy density and mass efficiency supporting a highly efficient electrified system layout. Integrating long-range practicality, strong power delivery, and an intelligent electric architecture, the model is designed to provide users with a balanced experience that combines sports-car-grade acceleration with the spaciousness of a luxury SUV.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The All Electric SUV market is segmented as below:

By Company

Porsche

BMW

Mercedes Benz

Audi

Land Rover

Subaru

Kia

Honda

Volvo

Lexus (Toyota)

Cadillac (General Motors)

Nissan Motor

Hyundai

Polestar

Geely Auto

Seres Auto (HUAWEI)

Leapmotor

Li Auto

XPENG

Xiaomi

NIO

Dongfeng Motor

Beijing Automotive

Chery Automobile

IM Motors(SAIC Motor)

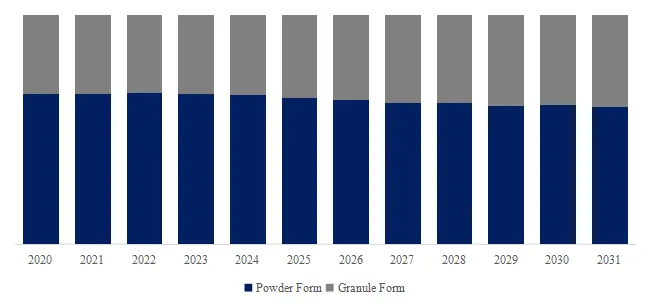

Segment by Type

Regular

Customized

Segment by Application

Personal Use

Commercial Use

Each chapter of the report provides detailed information for readers to further understand the All Electric SUV market:

Chapter 1: Introduces the report scope of the All Electric SUV report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of All Electric SUV manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various All Electric SUV market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of All Electric SUV in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of All Electric SUV in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth All Electric SUV competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides All Electric SUV comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides All Electric SUV market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global All Electric SUV Market Outlook, In‑Depth Analysis & Forecast to 2032

Global All Electric SUV Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global All Electric SUV Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp