QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Multi-Layer Blow Molding Machines- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Multi-Layer Blow Molding Machines market, including market size, share, demand, industry development status, and forecasts for the next few years.

The global market for Multi-Layer Blow Molding Machines was estimated to be worth US$ 600 million in 2025 and is projected to reach US$ 761 million, growing at a CAGR of 3.5% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5987641/multi-layer-blow-molding-machines

Multi-Layer Blow Molding Machines

Multi-layer blow molding machines are specialized equipment that use co-extrusion technology to combine two or more plastic melts with different properties (such as different resins or recycled materials) into a multilayer preform within a die, and then blow-form it into hollow products. Its core function is to manufacture plastic containers and products with multilayer functional structures (such as barrier, reinforcement, and aesthetics) in a single production step, overcoming the limitations of single-layer products in terms of barrier properties (prevention of oxygen/water vapor penetration), mechanical strength, cost control (allowing the use of inexpensive recycled materials as intermediate layers), and appearance design. Upstream suppliers mainly include manufacturers of special extruders and dies (such as co-extrusion system suppliers), manufacturers of multilayer plastic particles (such as EVOH and PA barrier materials), and suppliers of high-precision hydraulic/servo control systems. Downstream suppliers directly serve end-product packaging manufacturers, with core application areas including food and beverage (barrier preservation bottles), pharmaceuticals (sterile medicine bottles), and chemicals (corrosion-resistant containers).

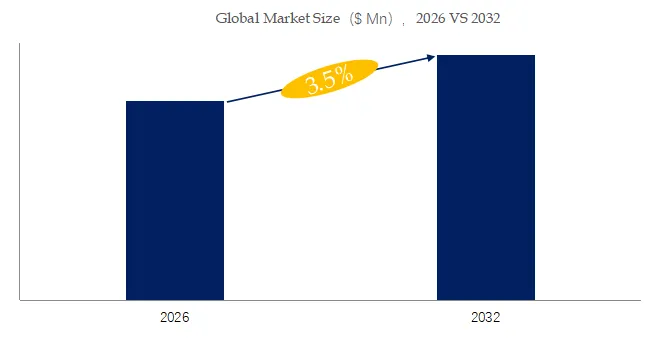

According to QYResearch’s latest research report, ” Multi-Layer Blow Molding Machines – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″ the multi-layer blow molding machines market size is projected to reach US$761 million by 2032, with a CAGR of 3.5% over the next few years.

Figure00001. Multi-Layer Blow Molding Machines Market Size (US$ Million), 2026 VS 2032

Above data is based on report from QYResearch: Multi-Layer Blow Molding Machines- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Market Overview

The global multi-layer blow molding machines market is in a phase of steady growth, driven primarily by strong demand for high-performance plastic packaging in the food and beverage, pharmaceutical, and personal care industries. Multi-layer containers with high barrier properties, lightweight design, and environmentally friendly features are particularly favored. On the technological front, the industry is undergoing profound changes, with automation, intelligent control, and deep integration with Industry 4.0 systems becoming mainstream trends. At the same time, in response to global carbon reduction and circular economy initiatives, equipment manufacturers are actively developing machines capable of efficiently processing recyclable materials and bio-based polymers to meet increasingly stringent environmental regulations. Despite the promising outlook, the market still faces challenges such as high initial investment, complex operation and maintenance, and competition from other molding processes.

Regional Analysis

The Asia-Pacific region is currently the main force in the global multi-layer blow molding machine market, not only holding the largest market share but also being the fastest-growing area. China, as the engine of the region, with its vast manufacturing base and industrial clusters, is both the world’s largest equipment producer and consumer market, and has nurtured numerous local manufacturers with international competitiveness, dominating the mid- to low-end market while accelerating penetration into the high-end segment. In contrast, European and American manufacturers, represented by German companies, firmly hold the high-end market, possessing unshakable technological advantages and brand barriers in ultra-wide, ultra-precision, and special-function film equipment. Meanwhile, Southeast Asia is becoming a new hotspot for global capacity transfer, while the North American market, driven by policies such as the renewable plastics act, has seen a surge in demand for biobased material processing equipment.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Multi-Layer Blow Molding Machines market is segmented as below:

By Company

Bekum Maschinenfabriken GmbH (Unlisted, Berlin Germany)

Kautex Maschinenbau GmbH (Unlisted, Bonn Germany)

Mauser Packaging Solutions (Unlisted,Ohio USA)

Davis-Standard, LLC (Unlisted, Connecticut USA)

The Japan Steel Works, Ltd. (TYO: 5631, Tokyo Japan)

SACMI Imola S.C. (Unlisted, Imola Italy)

Jomar Corporation (Unlisted, New Jersey USA)

Central Machinery & Plastic Products (Unlisted, Mumbai India)

Blow Enterprises Inc (Unlisted, Mumbai India)

Parker Plastic Machinery Co., Ltd. (Unlisted, Taiwan China)

Taizhou Huangyan Maiwei Machinery Co., Ltd. (Unlisted, Zhejiang China)

Bestar Blow Molding Machinery Co., Ltd. (Unlisted, Jiangsu China)

Qingdao Yankang Plastic Machinery Co., Ltd. (Unlisted, Qingdao China)

Full Shine Plastic Machinery Co., Ltd. (Unlisted, Taiwan China)

Guangdong Jinming Plastics Equipment Co., Ltd. (Unlisted, Guangdong China)

Segment by Type

Horizontal Multi-Layer Blow Molding Machines

Vertical Multi-Layer Blow Molding Machines

Segment by Application

Food and Beverage

Pharmaceutical

Chemical

Other

Each chapter of the report provides detailed information for readers to further understand the Multi-Layer Blow Molding Machines market:

Chapter 1: Introduces the report scope of the Multi-Layer Blow Molding Machines report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Multi-Layer Blow Molding Machines manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Multi-Layer Blow Molding Machines market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Multi-Layer Blow Molding Machines in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Multi-Layer Blow Molding Machines in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Multi-Layer Blow Molding Machines competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Multi-Layer Blow Molding Machines comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Multi-Layer Blow Molding Machines market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Multi-Layer Blow Molding Machines Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Multi-Layer Blow Molding Machines Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Multi-Layer Blow Molding Machines Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp