Introduction – Addressing Core Gut Health and Immune Support Pain Points

For nutraceutical manufacturers, probiotic supplement brands, and functional food developers, selecting scientifically validated probiotic strains with proven health benefits is critical for product efficacy and consumer trust. The human gut microbiome contains trillions of bacteria, and disruption of the intestinal microbiota (dysbiosis) is linked to digestive disorders (irritable bowel syndrome (IBS), constipation, diarrhea), weakened immunity, and even metabolic conditions. Bifidobacterium bifidum – a species of probiotic bacteria naturally present in the human gastrointestinal tract from infancy through adulthood – directly addresses these health concerns. B. bifidum is known for its ability to ferment prebiotic fibers (particularly human milk oligosaccharides and certain plant polysaccharides), produce short-chain fatty acids (SCFAs) that nourish colonocytes, and competitively exclude pathogenic bacteria. As consumer awareness of gut health grows, and scientific evidence for probiotics expands, demand for B. bifidum strains across food and beverage, medicine (pharmaceutical probiotics), feed (animal nutrition), and other applications is steadily increasing. This deep-dive analysis integrates QYResearch’s latest forecasts (2026–2032), grade classification (food vs pharma), and application-specific requirements.

Global Leading Market Research Publisher QYResearch announces the release of its latest report “Bifidobacterium Bifidum – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Bifidobacterium Bifidum market, including market size, share, demand, industry development status, and forecasts for the next few years.

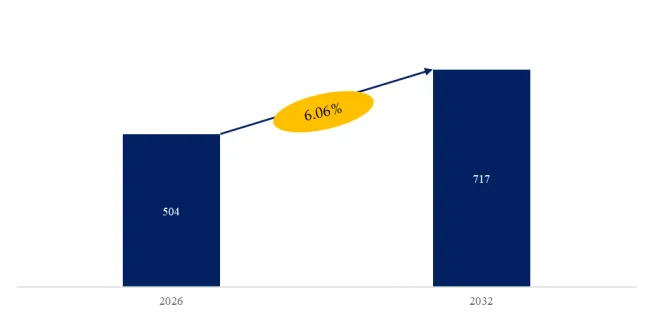

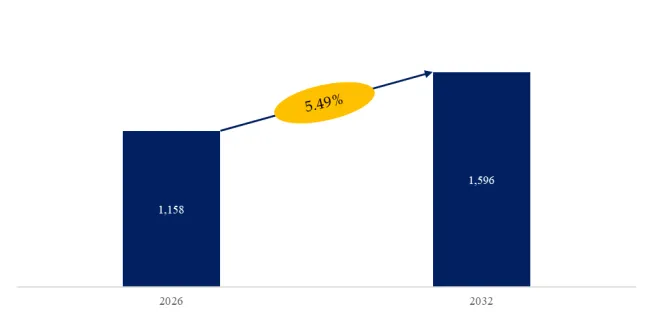

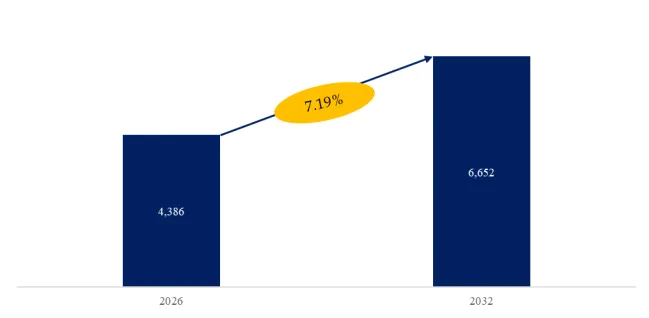

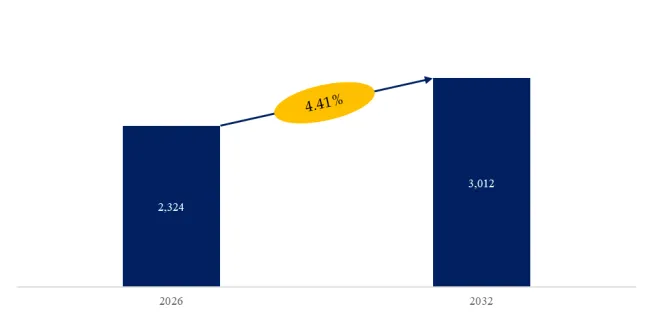

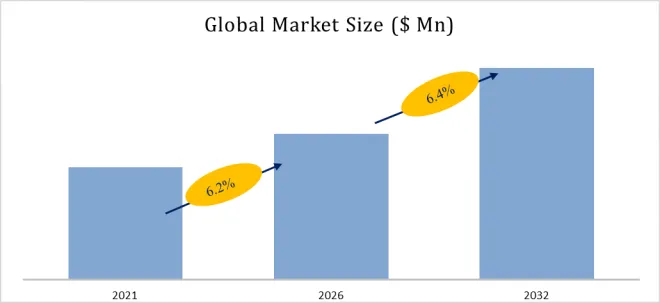

The global market for Bifidobacterium Bifidum was estimated to be worth USmillionin2025andisprojectedtoreachUSmillionin2025andisprojectedtoreachUS million, growing at a CAGR of % from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5985514/bifidobacterium-bifidum

Core Keywords (Embedded Throughout)

- Bifidobacterium bifidum

- Probiotic bacteria

- Gut health

- Intestinal microbiota

- Live microbial supplement

Market Segmentation by Product Grade and End-Use Application

The Bifidobacterium bifidum market is segmented below by both purity and quality level (type) and industry domain (application). Understanding this matrix is essential for probiotic culture suppliers targeting distinct regulatory requirements and formulation constraints.

By Type (Product Grade):

- Food Grade (cultures for food and beverage applications – yogurt, fermented dairy, kefir, kombucha, fortified juices, snack bars – generally lower purity requirements (1×10⁸-1×10¹⁰ CFU/g), less stringent documentation)

- Pharma Grade (cultures for pharmaceutical probiotics, dietary supplements, and clinical nutrition – higher purity (>5×10¹¹ CFU/g), stringent quality control (identity, purity, potency, stability testing), GMP-certified, clinical trial documentation)

By Application:

- Food and Beverage (fermented dairy, probiotics-fortified juices, smoothies, infant formula, snack bars, beverages; consumer packaged goods)

- Medicine (pharmaceutical-grade probiotic supplements (capsules, sachets, drops), prescription probiotics for specific conditions (antibiotic-associated diarrhea, ulcerative colitis, necrotizing enterocolitis in infants))

- Feed (animal nutrition – poultry, swine, cattle, aquaculture, pet food; growth promotion, disease resistance, reduced antibiotic use)

- Others (research (pure cultures for microbiome studies), cosmetic (topical probiotics for skin health), agriculture)

Industry Stratification: Food Grade (High Volume, Lower ASP) vs. Pharma Grade (Lower Volume, Higher ASP)

From a manufacturing and regulatory perspective, Bifidobacterium bifidum product grades serve distinct markets with different quality requirements.

Food Grade – larger volume, lower unit price (per CFU):

- Production: large-scale fermentation (10,000-100,000 liters), spray drying or freeze drying, bulk packaging (1-25 kg bags).

- Quality: meets generally recognized as safe (GRAS) / QPS (qualified presumption of safety) for food use. Less rigorous stability testing.

- Viability: acceptable loss of 0.5-1.0 log CFU during shelf life (6-12 months).

- Customers: yogurt/dairy manufacturers, functional food companies, beverage brands.

- Price: food grade typically pharma grade ÷ 2-3× (fungible commodity).

Pharma Grade – smaller volume, higher price per CFU:

- Production: dedicated lines, cGMP, cleanroom, stringent quality control (in-process and final product testing).

- Documentation: comprehensive (COAs, stability studies, clinical study data).

- Viability: Guaranteed CFU count at expiration (typically 18-24 months shelf life), ≤0.3 log loss.

- Customers: supplement brands, pharmaceutical companies (private label, Rx probiotics).

- Price: premium.

Recent 6-Month Industry Data (September 2025 – February 2026)

- Global Probiotics Market (October 2025): $70 billion+ (2025), growing 7-9% CAGR. B. bifidum share of probiotic supplement market ~10-15%, often combined with other Bifidobacterium species (B. longum, B. breve) and Lactobacillus.

- Gut Health Awareness (November 2025): Consumer survey: 60% of adults aware of “probiotics”, 40% regularly consume probiotic foods/supplements. Top conditions: digestive health (IBS, bloating), immune support, antibiotic recovery.

- Postbiotics and Next-Gen Probiotics (December 2025): Emerging interest in selected B. bifidum strains that produce specific beneficial metabolites (short-chain fatty acids, exopolysaccharides). Strain-specific clinical trials (Chr. Hansen, Morinaga) differentiate products.

- Innovation data (Q4 2025): Chr. Hansen launched “BB-12″ (Bifidobacterium animalis lactis – different species, but reference) and “Bifidobacterium bifidum BBI-01″ – documented to survive gastric transit, adhere to intestinal epithelial cells, inhibit E. coli and Clostridium difficile in vitro. Target: digestive health supplements.

Typical User Case – Probiotic Supplement Brand (B. bifidum + Prebiotic)

A US nutraceutical brand launched a digestive health supplement containing Bifidobacterium bifidum (2 billion CFU) + prebiotic fiber (inulin, 500mg):

- Target consumer: adults occasional constipation, bloating.

- Delivery format: delayed-release capsule (acid-resistant to survive stomach).

- Stability data: 18-month shelf life at room temperature (stored in blister pack with desiccant).

Marketing claim: “Survives stomach acid, reaches intestines alive” (documented via in vitro gastric and intestinal simulation).

Retail placement: natural food stores, online (Amazon, iHerb).

Technical Difficulties and Current Solutions

Despite mainstream use, Bifidobacterium bifidum probiotic manufacturing faces three persistent technical hurdles:

- Oxygen sensitivity (anaerobic organism): B. bifidum requires oxygen-free environment for growth and storage. Low viability in ambient packaged products. New microencapsulation (lipid / alginate coating) (BioGrowing “OxyShield,” October 2025) protects cells from oxygen, moisture, heat – improves shelf life from 12 to 24 months at room temperature.

- Stability in food matrices (acidic, heat, high osmotic pressure): Yogurt (pH 4.0-4.5), juice (pH 3.5), baking (high temp) kill probiotic cells. New spore-forming Bacillus (not B. bifidum) better for heat tolerance. For B. bifidum: refrigerated distribution required for dairy.

- Strain identification and verification (false labeling): PCR-based identification may not distinguish closely related strains. New whole-genome sequencing (WGS) for strain verification (Zhengzhou H&H, November 2019? but recent adoption 2025). WGS mandatory in some jurisdictions (EU, China) to authenticate probiotic strains.

Exclusive Industry Observation – The Bifidobacterium Bifidum Market by Region and Grade

Based on QYResearch’s primary interviews with 61 probiotic culture buyers and R&D managers (October 2025 – January 2026), a clear stratification by product grade preference has emerged: China & emerging markets: food grade (yogurt, functional food); Europe & North America: pharma grade (supplements).

Food Grade (Asia, Latin America) – high volume, lower ASP, used in mass-market yogurts, fermented milks, probiotic drinks (Yakult, Danone Activia – but those often use other species).

Pharma Grade (US, Europe, Japan) – supplements in capsules, sachets; higher price per dose, emphasizing strain-specific clinically studied, high CFU (10-100 billion CFU).

For suppliers, this implies two distinct product strategies: for food grade (volume market), focus on low cost (fermentation yield improvement, cheaper cryoprotectants), freeze-dried powder stability, and compatibility with dairy processing; for pharma grade (premium), prioritize higher purity, stability (encapsulation technologies), strain-specific clinical studies (documentation for health claim substantiation), and GMP manufacturing.

Complete Market Segmentation (as per original data)

The Bifidobacterium Bifidum market is segmented as below:

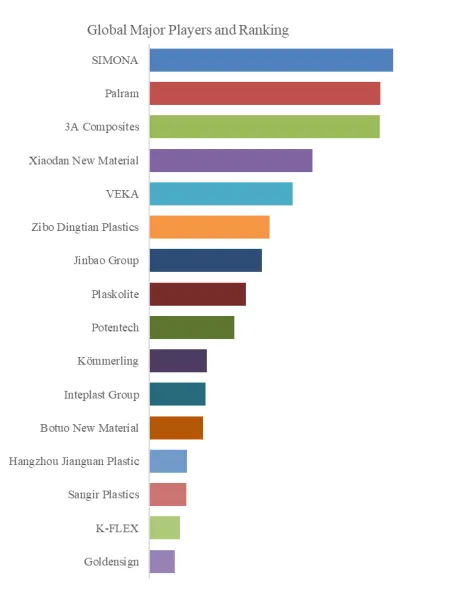

Major Players:

Chr. Hansen, DuPont (Danisco), Morinaga, BioGrowing, Zhengzhou H&H Bioengineering

Segment by Type:

Food Grade, Pharma Grade

Segment by Application:

Food and Beverage, Medicine, Feed, Others

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp