QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Alloy Poly-Putty Base- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Alloy Poly-Putty Base market, including market size, share, demand, industry development status, and forecasts for the next few years.

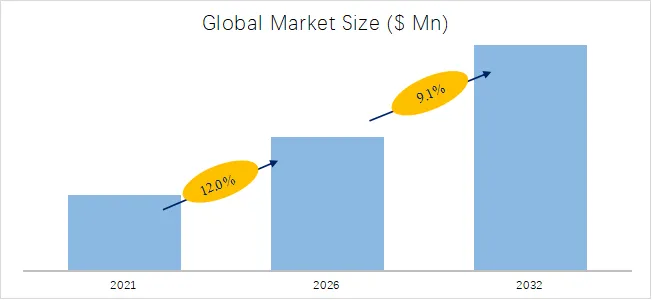

The global market for Alloy Poly-Putty Base was estimated to be worth US$ 776 million in 2025 and is projected to reach US$ 1072 million, growing at a CAGR of 4.8% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6116195/alloy-poly-putty-base

Alloy Poly-Putty Base Market Summary

Alloy Poly-Putty Base is a polymer-based putty or filler used for filling, repairing, and leveling surface defects in metals, wood, concrete, or composite substrates. It typically comprises resins (such as epoxy, polyester, or acrylic), fillers (calcium carbonate, talc, glass-fiber etc.), hardeners or curing agents, and other additives. Its favorable properties—good adhesion, sandability, strength, and ease of finishing—make it widely used in automotive repair, construction and renovation, furniture manufacturing, marine and industrial equipment repair.

According to the new market research report “Global Alloy Poly-Putty Base Market Report 2025-2031”, published by QYResearch, the global Alloy Poly-Putty Base market size is projected to reach USD 1.01 billion by 2031, at a CAGR of 4.8% during the forecast period.

According to QYResearch Top Players Research Center, the global key manufacturers of Alloy Poly-Putty Base include 3M, Akzo Nobel, DuPont, Axalta, Nippon Paint, etc. In 2024, the global top five players had a share approximately 67.0% in terms of revenue.

Market Drivers:

Growing Demand for Automotive Repair and Renovation: With the continued rise in vehicle ownership, especially in emerging markets (such as China, India, and Southeast Asia), repairs for minor bruises, scratches, and sheet metal deformation are increasingly common. Alloy Poly-Putty Base is a crucial finishing and finishing material for sheet metal/body repair.

Automotive Lightweighting and Use of New Materials: To improve fuel efficiency and range (for electric vehicles), new vehicles are increasingly using aluminum, plastic, and composite materials. These materials place higher demands on the compatibility, adhesion, and shrinkage of the repair materials used during repair and filling, prompting Alloy Poly-Putty Base manufacturers to upgrade their formulations.

Demand for Improved Application Efficiency and Performance: Fast drying speed, easy sanding, good adhesion, weather resistance (water, heat, and UV resistance), and low cracking are key priorities for repair shops, sheet metal workers, and home improvement engineers. These properties directly affect the construction period, rework rate and final cost. Market competition also prompts manufacturers to make continuous improvements in these aspects.

Market Barriers:

Raw Material Cost Fluctuations and Price Increases: Chemical raw materials such as resins, curing agents, pigments, and solvents required for putty production are significantly affected by international petrochemical prices, supply and demand, and transportation costs. Frequent fluctuations in raw material prices can squeeze manufacturers’ profit margins and increase pricing risks, particularly for small and medium-sized manufacturers.

Competition Between Alternative Materials and Repair Technologies: As repair technologies advance, some alternative materials or methods may challenge traditional putty. For example, high-performance adhesives, resin spraying, nano-repair materials, 3D printing repairs, laser repairs, or dry film fillers may offer better performance or lower costs in certain applications. This could reduce demand for traditional putty.

Risk of economic cycle and shrinking repair market: If the macroeconomy declines, consumer spending decreases or vehicle ownership stagnates/slows down, disposable spending on auto repairs (especially cosmetic/sheet metal repair) may be affected, indirectly suppressing the demand for putty products.

Market Opportunities:

Environmental Regulations and Increasing Consumer Demand for Low-VOC/Sustainable Products: Many countries and regions are tightening regulations on volatile organic compounds (VOCs), air quality, and chemical emissions. Putty products that reduce VOC content, use water-based or bio-based resins, and incorporate renewable or recyclable fillers may offer regulatory advantages while catering to environmentally conscious car owners and repair shops.

Regional Market Expansion and Localized Production: Rapid urbanization and rising vehicle ownership in regions like China, India, and Southeast Asia are driving a surge in demand for repair shops and body repair services. While these regions are price-sensitive, they are also increasingly prioritizing product quality and environmental protection. Manufacturers who can establish local production or distribution networks in these regions, reduce transportation costs and tariffs, and customize products to meet local regulations and requirements, stand to benefit significantly.

Growth of DIY and Consumer-Oriented Products: The market for home car owners and minor car repair enthusiasts (DIY repair) is expanding in North America, Europe, and some Asian countries. Products with easy-to-use packaging (such as pre-mixed pastes/small sachets), ease of use, low odor, and fast curing characteristics are gaining popularity. Manufacturers can develop formulations and packaging formats targeted at non-professional users, thereby opening up new market segments.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Alloy Poly-Putty Base market is segmented as below:

By Company

3M

Akzo Nobel

DuPont

Axalta

Nippon Paint

Sika AG

Alps Coating

SANVO CHEMICAL

Bangni Coatings

Wuxi Federal Coatings

Changxing Baodi Environmental Protection Technology

Segment by Type

Single-Component

Two-Component

Segment by Application

Automotive

Marine

Others

Each chapter of the report provides detailed information for readers to further understand the Alloy Poly-Putty Base market:

Chapter 1: Introduces the report scope of the Alloy Poly-Putty Base report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Alloy Poly-Putty Base manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Alloy Poly-Putty Base market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Alloy Poly-Putty Base in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Alloy Poly-Putty Base in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Alloy Poly-Putty Base competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Alloy Poly-Putty Base comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Alloy Poly-Putty Base market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Alloy Poly-Putty Base Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Alloy Poly-Putty Base Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Alloy Poly-Putty Base Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp