Global Leading Market Research Publisher QYResearch announces the release of its latest report “Industrial Low NOx Burner – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Industrial Low NOx Burner market, including market size, share, demand, industry development status, and forecasts for the next few years.

Why are power plant operators, oil refinery managers, and food processing facility engineers accelerating replacement of conventional burners with industrial low NOx burner technology? Three converging pressures define the combustion equipment landscape in 2026: tightening nitrogen oxide (NOx) emission limits (the EU Industrial Emissions Directive 2024 revision mandates NOx below 50 mg/Nm³ for new combustion plants), rising carbon pricing mechanisms (EU ETS allowance prices exceeding €90/tonne), and community opposition to industrial air permits in densely populated areas. Industrial low NOx burners address these challenges through advanced flame engineering – controlling fuel-air mixing to create larger, more branched flames that reduce peak flame temperature and suppress thermal NOx formation. The result: 50–80% NOx reduction compared to conventional burners, compliance with IED and EPA Boiler MACT standards, and avoidance of production curtailment during air quality action days.

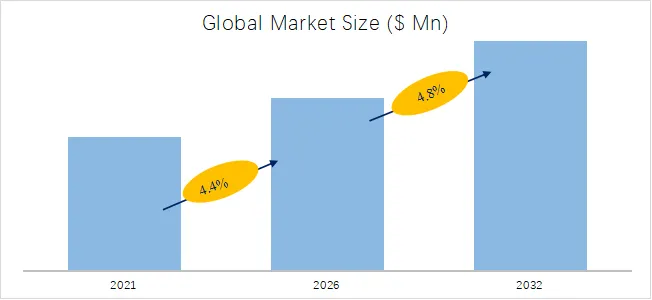

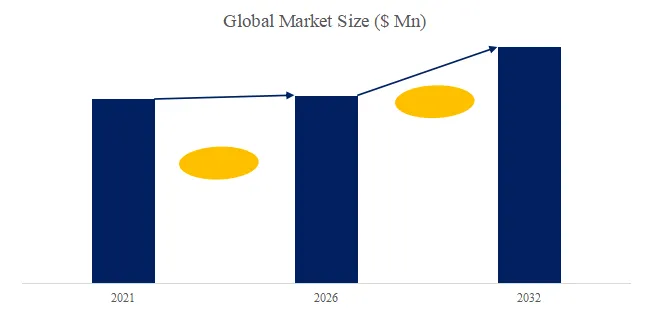

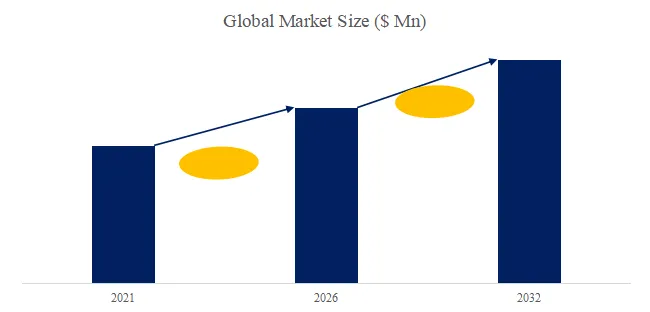

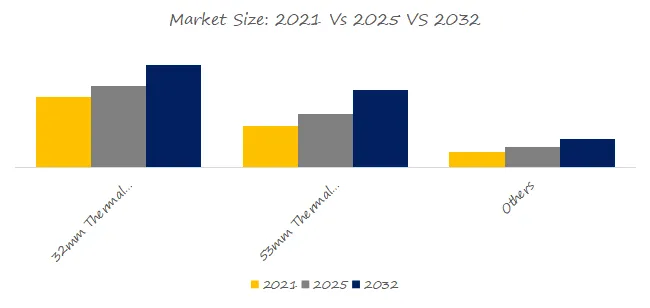

The global market for Industrial Low NOx Burner was estimated to be worth US$ 1,503 million in 2025 and is projected to reach US$ 2,175 million by 2032, growing at a CAGR of 5.5% from 2026 to 2032. This steady growth reflects both retrofit demand (replacing legacy burners installed before 2010) and new capacity additions in emerging industrial economies.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/reports/5762444/industrial-low-nox-burner

Product Definition: What Is an Industrial Low NOx Burner?

An industrial low NOx burner is a combustion device designed to control fuel and air mixing at each burner nozzle to create larger, more branched flames. By staging combustion – either through air staging (introducing combustion air in multiple zones) or fuel staging (distributing fuel injection across the flame zone) – peak flame temperature is reduced below 1,500°C, the threshold at which thermal NOx formation accelerates exponentially. Unlike conventional burners that achieve complete combustion in a compact flame zone (1,400–1,650°C), low NOx designs extend the flame volume while maintaining stable ignition. Key technical parameters include: flame length (typically 2–5x longer than conventional equivalents), excess O₂ levels (2–4% vs. 3–6%), and flue gas recirculation (FGR) rates (10–25% of flue gas returned to combustion zone). NOx reduction efficiency ranges from 50% (simple staged air design) to 80% (FGR-equipped designs), with corresponding capital cost premiums of 20–60% over conventional burners.

Market Segmentation: Capacity Tiers and End-User Verticals

By Burner Size (Thermal Capacity):

- Compact Burner – Thermal output <1 MW. Typical applications: small industrial boilers (1–10 tonnes/hour steam), food processing ovens, drying kilns, and space heating for industrial facilities. Key characteristics: packaged design (burner + controls + blower integrated), quick installation (1–3 days), and lower absolute NOx reduction requirements (compliance with local air permits rather than major source regulations).

- Medium Burner – Thermal output 1–10 MW. Typical applications: industrial steam boilers (10–100 tonnes/hour), thermal oil heaters, air heaters for drying processes (textiles, paper, chemicals), and district heating plants. Largest market segment by volume (45–50% of units), featuring modular designs with separate blower and control cabinets.

- Large Burner – Thermal output >10 MW. Typical applications: power plant utility boilers (co-firing or dedicated gas/oil), refinery process heaters (crude heaters, reformers, cokers), ethylene crackers, and large-scale industrial CHP (combined heat and power) plants. Highest value segment (55–60% of market value by revenue), requiring custom engineering, extended lead times (6–12 months), and specialized commissioning.

By Application (End-User Vertical):

- Power Plant – Gas-fired combined cycle plants (CCGT), coal-to-gas conversion boilers, biomass co-firing plants, and peaking plants. Key drivers: environmental permits requiring NOx <30 mg/Nm³ for new gas turbines (EU and US EPA Tier 4 standards), and operating flexibility (low NOx burners enable plants to run at partial load without emissions excursions).

- Oil Refinery – Process heaters (crude distillation, catalytic reforming, hydrocracking), reformers (hydrogen production), and cokers. Refineries face some of the strictest NOx limits due to dense surrounding communities (e.g., US EPA Refinery Sector Rule requiring NOx <0.04 lb/MMBtu). Low NOx burners also reduce fouling of downstream selective catalytic reduction (SCR) systems, extending catalyst life by 20–30%.

- Food Processing – Industrial ovens (baking, drying), fryers, cookers, and sterilization autoclaves. Food processors prioritize burner reliability (avoiding production loss) and cleanliness (minimizing soot and unburned hydrocarbons that affect product quality). Low NOx designs with electronic flame monitoring and auto-tuning controls are gaining adoption.

- Others – Chemical manufacturing, pulp and paper (recovery boilers, lime kilns), cement kilns (precalciner burners), and metal processing (annealing furnaces, heat treatment lines).

Key Industry Characteristics Driving Strategic Decisions (2026–2032)

1. Regulatory Ratcheting: The Primary Demand Driver for Industrial Low NOx Burners

Emission standards for NOx have tightened across all major industrial regions over the past 36 months, with further reductions scheduled through 2030:

| Region | Current NOx Limit (new sources) | 2028–2030 Target | Applicable Standard |

|---|---|---|---|

| European Union | 50 mg/Nm³ (gas), 80 mg/Nm³ (oil) | 30 mg/Nm³ (gas) by 2028 | IED 2024 Revision |

| United States | 0.04 lb/MMBtu (refineries), 0.07 lb/MMBtu (boilers) | 0.025 lb/MMBtu proposed | EPA Boiler MACT Review (2025) |

| China | 50 mg/Nm³ (key regions), 100 mg/Nm³ (national) | 30 mg/Nm³ (national) by 2027 | GB 13271-2025 Revision |

| India | 150 mg/Nm³ (existing), 100 mg/Nm³ (new) | 50 mg/Nm³ by 2029 | MoEFCC Notification (August 2025) |

For plant operators, non-compliance carries significant penalties: EU Member States impose fines of €5,000–50,000 per day of exceedance; US EPA can levy penalties up to US$50,000 per day under Clean Air Act Section 113. Industrial low NOx burners represent the most cost-effective compliance pathway for most boiler and heater applications, with payback periods of 1.5–3 years when accounting for avoided fines, reduced SCR reagent consumption (ammonia/urea), and potential emission credit trading revenue.

2. Technology Evolution: From Basic Staged Air to Advanced FGR and Flameless Oxidation

First-generation low NOx burners (pre-2015) relied solely on staged air designs, achieving 40–50% NOx reduction but suffering from flame instability at low fire rates (below 30% load) and higher CO emissions (50–100 ppm).

Second-generation (2015–2022) added external flue gas recirculation (FGR), recirculating 10–20% of flue gas back into the combustion zone. FGR reduces flame temperature through dilution, achieving 60–75% NOx reduction with improved flame stability. Key manufacturers including Weishaupt, Riello, and Honeywell have standardized FGR ports on medium and large burner models.

Third-generation (2023 onward) introduces flameless oxidation (also known as colorless combustion or distributed combustion), where fuel and air are pre-mixed with high levels of recirculated flue gas (30–50%) to eliminate visible flame and reduce peak temperatures below 1,200°C. Early adopters (John Zink, Zeeco) report NOx below 15 mg/Nm³ – meeting the most stringent targets without SCR – with CO below 10 ppm and thermal efficiency equal to conventional designs. However, flameless burners require precise control of preheat temperatures (>600°C), limiting application to continuous high-load operations (refinery heaters, power boilers) rather than cycling processes.

3. Technical Challenge: The Low-NOx / CO Trade-off

A fundamental combustion engineering constraint persists: NOx reduction techniques (lower peak temperature, shorter residence time at high temperature) tend to increase carbon monoxide (CO) and unburned hydrocarbon (UHC) emissions. In staged-air designs, the fuel-rich primary zone operates below stoichiometric conditions, producing intermediate species (CO, H₂, radicals) that must be fully oxidized in the secondary zone. If mixing is incomplete, CO emissions can exceed 100 ppm – violating air permits in jurisdictions with CO limits (e.g., California South Coast AQMD Rule 1146 requires CO <50 ppm). Leading suppliers address this through: (a) computational fluid dynamics (CFD) optimization of burner tile geometry, (b) active flame monitoring with O₂/CO trim control, and (c) selective catalytic reduction (SCR) downstream when ultra-low NOx (<10 mg/Nm³) is required. For plant operators, specifying a burner requires balancing NOx reduction targets against CO compliance, thermal efficiency, and capital budget.

4. Industry Segmentation: Continuous Process vs. Batch Process Applications

The industrial low NOx burner market serves two fundamentally different operational paradigms:

- Continuous process industries (refineries, power plants, chemical manufacturing): Burners operate at steady load for extended periods (weeks or months between outages). Key requirements: long service intervals (>8,000 hours), high turndown ratio (ability to operate from 20–100% load), and compatibility with predictive maintenance systems (vibration monitoring, flame scanners, O₂ sensors). Suppliers serving this segment (John Zink, Zeeco, Honeywell) emphasize durability, field service networks, and digital twin integration for combustion optimization.

- Batch process industries (food processing, pharmaceuticals, textiles): Burners cycle frequently (multiple starts/stops per shift), with varying load profiles. Key requirements: rapid response (ignition to full load in <30 seconds), consistent emissions across load range, and compact footprint for retrofitting into existing equipment. Suppliers serving this segment (Riello, Baltur, Ariston Thermo Group) emphasize packaged designs, self-diagnostics, and ease of maintenance (quick-access burner heads, plug-in control modules).

5. Recent Policy and Project Milestones (July 2025 – March 2026)

- EU (September 2025): The European Commission published the Best Available Techniques (BAT) reference document for large combustion plants, setting NOx emission levels of 30–50 mg/Nm³ for new gas-fired boilers >50 MWth, effective January 2027. This triggers a retrofit wave: QYResearch estimates 1,200–1,500 industrial boilers across Germany, France, Italy, and Poland will require burner replacements or upgrades by 2028.

- China (November 2025): The Ministry of Ecology and Environment issued updated emission standards for industrial boilers (GB 13271-2025), lowering the national NOx limit from 100 mg/Nm³ to 50 mg/Nm³ for all new boilers >10 MWth, with existing boilers required to comply by December 2028. Baite Burners and Lingyun Redsun have launched localized low NOx burner lines targeting this retrofit market, priced 30–40% below imported equivalents.

- India (January 2026): The Maharashtra Pollution Control Board mandated low NOx burners for all process heaters and boilers in the Mumbai–Pune industrial corridor (over 3,000 facilities) following high smog events in Q4 2025. Enertech Group and Bohui have announced joint venture manufacturing in Pune to serve this demand.

- United States (February 2026): The EPA finalized the Boiler MACT residual risk and technology review (RRTR), maintaining existing NOx limits but adding digital monitoring requirements (continuous emission monitoring systems or predictive emission monitoring systems) for all boilers >10 MMBtu/hr. This increases demand for low NOx burners with integrated CEMS connectivity.

6. Exclusive Industry Observation: The Hydrogen Co-firing Transition

As industrial facilities plan for decarbonization, a new requirement is emerging: low NOx burner compatibility with hydrogen-natural gas blends. Hydrogen combustion presents unique challenges: higher flame speed (3–4x natural gas), wider flammability range, and higher adiabatic flame temperature (2,100°C vs. 1,950°C for methane), which can increase thermal NOx formation by 30–50% if not managed. Leading burner manufacturers are developing dual-fuel low NOx designs capable of handling 0–100% hydrogen blends:

- Weishaupt launched the WK-H2 series (September 2025), featuring modified burner heads, flashback arrestors, and specialized flame ionization detection. The burner maintains NOx <40 mg/Nm³ up to 50% H₂ blend without FGR, and <20 mg/Nm³ with FGR.

- John Zink announced (January 2026) a hydrogen-ready version of its CoJet burner for refinery heaters, incorporating micro-mixing nozzles that reduce flame temperature by 200°C compared to conventional designs.

For plant operators planning hydrogen co-firing (e.g., EU refineries targeting 30% H₂ by 2030 under RePowerEU), specifying hydrogen-ready low NOx burners now avoids costly replacement later. QYResearch estimates that hydrogen-compatible burners will command a 15–25% price premium over conventional low NOx designs through 2030, representing a US$200–300 million incremental market opportunity.

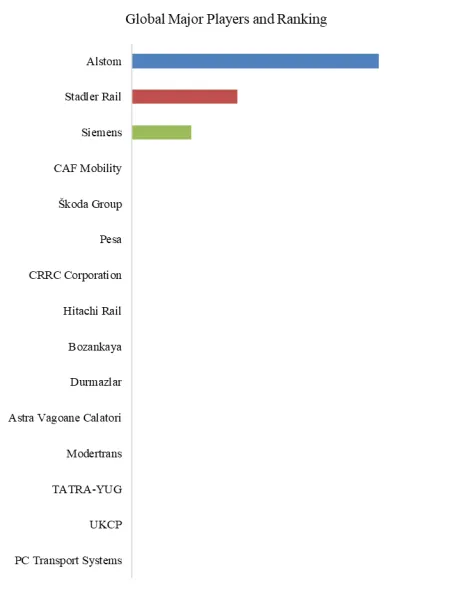

Key Players Shaping the Competitive Landscape

The market features European combustion engineering leaders, North American process burner specialists, and rapidly growing Asian manufacturers:

Weishaupt, Honeywell, Riello, John Zink, Oilon, Baite Burners, Enertech Group, Bohui, Ariston Thermo Group, Baltur, Zeeco, Chugai Ro, Lingyun Redsun, Wuxi Saiwei Burner, Faber Burner.

Strategic Takeaways for Plant Operators, EPC Contractors, and Investors

- For plant operators and facility engineers: Conduct a burner inventory audit immediately. If any boiler or heater exceeds 5,000 operating hours since 2018, NOx emissions likely exceed current permit levels. The most cost-effective compliance pathway is staged replacement of conventional burners with low NOx units during scheduled outages – incremental capital cost of US$20,000–100,000 per burner (depending on size) avoids US$50,000–500,000 in potential fines annually.

- For EPC contractors and engineering firms: Differentiate by offering hydrogen-ready low NOx burners as a standard specification for all new combustion equipment, even if hydrogen co-firing is not planned until 2030–2035. This future-proofing adds minimal upfront cost (5–10% premium) but provides clients with regulatory flexibility and decarbonization optionality.

- For investors: Target companies with (a) proprietary flameless oxidation or advanced FGR technology achieving sub-20 mg/Nm³ NOx without SCR, (b) established field service networks in high-growth regions (India, Southeast Asia, Middle East), and (c) hydrogen-compatible product lines validated at scale. The 5.5% CAGR understates value creation for leaders capturing share in the retrofit wave triggered by 2025–2026 regulatory updates across the EU, China, and India – QYResearch estimates this retrofit opportunity alone exceeds US$800 million through 2030.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666 (US)

JP: https://www.qyresearch.co.jp