QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Rack-scale AI Solution for Datacenter- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Rack-scale AI Solution for Datacenter market, including market size, share, demand, industry development status, and forecasts for the next few years.

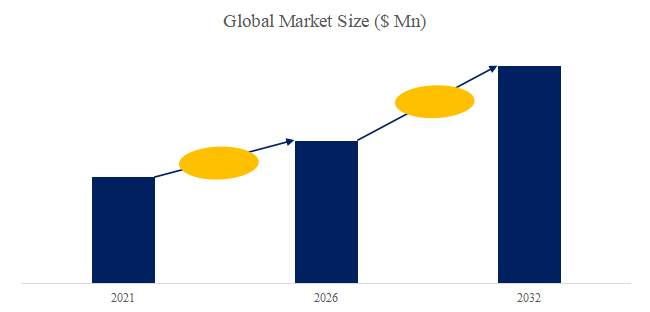

The global market for Rack-scale AI Solution for Datacenter was estimated to be worth US$ 1655 million in 2025 and is projected to reach US$ 5930 million, growing at a CAGR of 20.0% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5797793/rack-scale-ai-solution-for-datacenter

1. Rack-scale AI Solution for Datacenter Introduction

Rack-scale AI solutions for datacenters are designed to revolutionize the processing capabilities of large-scale computing environments by integrating multiple AI inference engines within a single rack. This approach enables the concurrent execution of numerous complex AI tasks, leading to unparalleled scalability and efficiency. By aggregating processing power across a rack, these solutions effectively reduce latency and bandwidth constraints, while also optimizing resource utilization and power management. The outcome is a cohesive, high-performance computing platform that can handle vast data volumes with precision and speed, thereby enhancing the overall infrastructure’s adaptability and responsiveness to dynamic workloads.

2. Rack-scale AI Solution for Datacenter Development Factors

2.1. Evolution of Rack-scale AI Architecture for Datacenter Driven by Dual Forces of Compute Density and Energy Efficiency

At the data center level, the rapid development of Rack-scale AI Solution for Datacenter is fundamentally driven by the combined forces of explosive growth in AI computing demand and the energy efficiency and thermal challenges brought by rising power density. On one hand, as large models—particularly large language models—continue to scale in both training and inference, computing demand is increasing exponentially. Pre-training scaling laws indicate that expanding model parameters and data volume can deliver predictable gains in intelligence, but only on the premise of massive and sustained compute investment. This dynamic renders traditional server-centric deployment models increasingly ineffective in terms of resource density, interconnect efficiency, and system-level optimization, forcing data centers to evolve toward highly integrated, highly parallel AI infrastructure with the rack as the fundamental unit. By integrating large numbers of GPUs or specialized accelerators within a single rack, such architectures support coordinated operation of ultra-large-scale clusters comprising thousands or even tens of thousands of nodes. On the other hand, the rapidly rising power consumption and thermal density of AI workloads are placing unprecedented pressure on data center power delivery and cooling systems. Traditional air cooling and low-power racks are no longer sufficient, driving Rack-scale AI Solution for Datacenter to incorporate liquid cooling technologies, cooling distribution units (CDUs), and megawatt-class power delivery capabilities from the outset, fundamentally restructuring power and thermal management architectures at the system level to ensure stability and reliability under high-load, long-duration operation. The interaction of these two forces is transforming data centers from collections of “stacked servers” into deeply optimized “rack-scale AI computing platforms” centered on compute density, energy efficiency, and scalability, establishing the core infrastructure paradigm for the next generation of AI development.

2.2. Evolution of Rack-scale AI Solution for Datacenter Driven by Scalability and Energy Efficiency

As modern data centers confront AI-driven, dynamic workloads, the demand for scalability and operational simplification has become a central force propelling the evolution of Rack-scale AI Solution for Datacenter. To respond rapidly to AI tasks of varying scales and types, rack-scale designs integrate servers, storage, networking, and cooling as a unified system-level building block. Through preconfigured standardized racks and shared resource pools, deployment and management processes are simplified, enabling more efficient resource expansion, disaggregation, and dynamic scheduling. This approach reduces operational complexity while enhancing business agility, allowing enterprises to respond more quickly to demands such as big data analytics and machine learning, shortening infrastructure time-to-production and effectively supporting rapidly changing market environments. Complementing this is the intense pressure to improve energy efficiency and optimize costs. The growth of AI workloads has significantly increased energy consumption, making energy costs and environmental impact core concerns for data center operators. Rack-scale AI Solution for Datacenter helps reduce total cost of ownership (TCO) and operating expenses (OPEX) by optimizing resource utilization, reducing overall server counts, adopting high-efficiency components, and implementing intelligent energy management strategies, thereby improving energy efficiency and supporting sustainability objectives. In addition, this integrated and efficient architecture facilitates multi-cloud deployment and edge computing integration, enhancing the overall flexibility and economic efficiency of IT resources. Taken together, the pursuit of scalability, operational simplification, and dual optimization of energy and cost is the key force driving the continued evolution of rack-scale AI infrastructure in data centers.

2.3. Key Technological Drivers of Rack-scale AI Solution for Datacenter

The evolution of Rack-scale AI Solution for Datacenter is strongly driven by a set of critical technological factors, with disruptive advances in chip and interconnect technologies at the core. Silicon photonics is emerging as a foundational technology for high-speed communication within data centers, replacing traditional electrical signaling with optical transmission to dramatically increase bandwidth while reducing latency and power consumption, enabling physical disaggregation and high-speed interconnection of compute, storage, and networking resources within and across racks. At the same time, the maturation of high-speed interconnect fabrics—such as NVLink, CXL, and emerging coherent optical links—further establishes low-latency, high-bandwidth resource pooling networks that support dynamic recomposition and pooling of CPUs, GPUs, memory, and storage. Together, these innovations enable the realization of disaggregated architectures, in which compute, storage, and networking resources are no longer statically bound to a single server but can be independently scaled and combined on demand, significantly improving resource utilization and infrastructure elasticity. For heterogeneous workloads such as AI training, network function virtualization, and big data analytics, this architecture allows independent upgrades and optimization of specialized hardware—including GPU clusters, smart NICs, and storage modules—without replacing entire systems, thereby enabling rapid adaptation to the fast pace of AI technology iteration. In addition, dynamic resource allocation capabilities enhance data center energy efficiency and reliability, supporting more granular power management and fault tolerance mechanisms. In summary, advances in chip technologies and the transformation of interconnect paradigms are jointly driving data centers from static, fixed architectures toward flexible, efficient, and scalable Rack-scale AI Solution for Datacenter, laying a solid foundation for addressing increasingly complex and large-scale computing scenarios.

3. Rack-scale AI Solution for DatacenterDevelopment Trends

3.1. Rack as Compute: The Inevitable Direction of Data Center Infrastructure Evolution in the AI Era

Against the backdrop of deep integration between cloud computing and artificial intelligence, data centers are transitioning from “server stacking” toward a stage of system-level competition where the rack becomes the smallest unit of innovation. Major North American cloud service providers have made it clear in public earnings calls and official statements that the core focus of future capital expenditures will be full-rack AI systems designed for large-model training and inference. These systems are typically built around NVIDIA’s latest-generation GPU platforms and achieve high-density integration of compute, networking, and power modules within a single rack, thereby shortening deployment cycles and increasing compute density. At the same time, companies such as Google, AWS, and Meta have continuously emphasized the importance of self-developed AI chips in their official technical blogs and annual reports. Rather than diminishing the value of rack-level solutions, this trend further reinforces the rack as the key carrier for unified delivery and scheduling of heterogeneous compute. Chinese technology companies, through policy documents and corporate announcements, have also proposed strengthening the autonomy and controllability of computing infrastructure, which likewise points toward a systemized construction path centered on full racks. From a technical perspective, the power wall and bandwidth wall brought about by the continued expansion of large model scale have been repeatedly highlighted in enterprise technical white papers and data center design documents. Traditional server-centric power delivery and interconnect models are no longer sufficient to support clusters of thousands or even tens of thousands of accelerators, driving data centers to introduce higher-voltage DC power architectures at the rack level as well as high-speed communication architectures centered on optical interconnects, thereby reshaping the physical organization of compute. More importantly, the high degree of system integration within a single rack significantly increases design, deployment, and operations complexity. Cloud service providers and equipment vendors, in official releases, generally regard “rack-level standardization” and “intelligent operations and maintenance” as key responses, moving system engineering capabilities forward into the manufacturing and delivery stages through pre-integrated and pre-validated AI rack solutions, and achieving dynamic optimization of energy efficiency, reliability, and performance during operation through AI-driven operations platforms. In this context, coupled with policy orientations in multiple countries promoting sovereign AI and domestic compute infrastructure development, rack-scale AI solutions for datacenter are evolving from configurations exclusive to high-end cloud providers into a general form of global data center construction. Their essence is not merely a hardware form factor upgrade, but an inevitable outcome of data centers shifting from component-level competition to competition based on system capabilities.

3.2. Energy as the Boundary: Structural Evolution of Rack-Scale AI Data Centers Driven by Sustainability Regulation

As global demand for AI compute accelerates, policy and energy constraints are shifting from peripheral conditions to core variables that determine the architectural direction of data centers. Represented by the Corporate Sustainability Reporting Directive published and implemented in official EU gazettes, regulators have explicitly required enterprises to disclose environmental impacts across the entire supply chain and operational lifecycle. This institutional constraint has directly driven cloud service providers and data center operators to list energy efficiency improvement and green power adoption as long-term strategic priorities in official statements and annual reports. In this context, rack-scale AI solutions become a key lever for implementing compliance and sustainability goals: by achieving tight coordination of compute, power delivery, and cooling at the rack level, operators can manage energy consumption and carbon footprints with greater granularity, pushing energy optimization from the data hall level down to the smallest system unit. Meanwhile, multiple leading cloud providers have publicly emphasized in corporate press releases that stable and sustainable energy access has become the primary consideration in hyperscale data center site selection and expansion. Energy is no longer merely a cost factor, but a strategic bottleneck that directly constrains the pace of compute deployment. Under such constraints, rack-scale AI solutions, due to their modularity and standardization, are more easily integrated with renewable energy supplies and new types of power infrastructure. For example, power density and cooling methods can be designed around specific energy conditions at the planning stage, thereby reducing reliance on traditional grid expansion. From a broader perspective, enterprises are increasingly treating the rack as the basic unit for energy efficiency management and compliance accounting in official technical documentation. This not only helps meet regulatory requirements for transparency and traceability, but also provides a practical foundation for cross-regional replication and rapid deployment. Thus, in an era characterized by tightening sustainability regulations and concurrent scarcity of green energy, rack-scale AI data center solutions are evolving from an engineering choice aimed at improving compute efficiency into an inevitable path for enterprises to address policy pressure, energy constraints, and long-term development responsibilities.

3.3. From Data Centers to “AI Factories”: Rack-Scale Systems Define a New Paradigm for Compute Infrastructure

Multiple leading cloud service providers and chip companies have explicitly stated in official announcements and annual reports that “AI factories” will gradually replace traditional general-purpose data centers. The essential characteristic of this new type of infrastructure is the use of large-scale, standardized deployments of rack-scale AI solutions as core production units. This new paradigm no longer centers on servers or individual devices, but instead resembles a highly automated industrial production line, achieving deep coordination and unified design of compute, power, cooling, and networking at the rack level, thereby transforming compute delivery into a replicable and scalable industrial capability. In terms of technical roadmap selection, cloud providers and system suppliers generally emphasize the importance of open architectures in official technical blogs and press releases. Rack-scale designs based on open standards such as OCP are regarded as key prerequisites for avoiding vendor lock-in, enhancing ecosystem compatibility, and maintaining future upgrade flexibility, a direction that has received sustained support from multiple international technology companies in public statements. At the same time, as sustainability goals are formally embedded into long-term corporate strategies, the weighting between compute efficiency and energy efficiency is undergoing a fundamental shift. In financial reports and sustainability disclosures, enterprises no longer focus solely on peak compute capability, but increasingly regard the effective compute delivered per unit of energy consumption as the core metric for assessing the advancement of AI infrastructure, as this directly affects long-term operating costs and compliance risks. Looking across the full lifecycle, cloud service providers are increasingly incorporating procurement, deployment cycles, operational energy consumption, and potential carbon constraints into a unified decision-making framework in official investment disclosures. Rack-scale solutions, due to their high degree of integration and predictability, are more conducive to full-lifecycle cost management. Within this logic, key technologies such as liquid cooling and energy storage, repeatedly highlighted in corporate announcements, may involve higher upfront investment, but demonstrate superior overall value in long-term operation, energy efficiency, and policy alignment. Overall, rack-scale AI solutions are becoming the physical foundation of the “AI factory” paradigm. Their significance goes beyond a simple technological upgrade and is reshaping the construction logic of compute infrastructure and the mode of competition across the industry.

4. Leading Manufacturer in the Industry

4.1. Supermicro

Supermicro is a global leader in application-optimized IT solutions, focused on delivering end-to-end servers, storage, networking, and green computing systems for enterprise, cloud, AI, and 5G telecom edge infrastructure. Through its distinctive Building Block Solutions architecture, the company provides highly customizable, high-performance hardware platforms spanning data centers, cloud computing, big data, high-performance computing, artificial intelligence, and edge computing. Supermicro emphasizes rapid delivery of innovative products, sustainable green computing, and comprehensive application-optimized design to help customers build efficient and scalable IT infrastructure, while maintaining a leading position in the server and storage markets.

Supermicro’s Rack-scale AI Solution for Datacenter is centered on its Rack Scale Solutions portfolio, delivering pre-integrated, fully configured and validated plug-and-play rack systems, categorized into rack-scale air-cooled solutions and rack-scale liquid-cooled solutions. Rack-scale air-cooled solutions are designed for traditional air-cooled environments, supporting high-density GPU server integration, NVLink high-speed interconnects, and all-flash storage to enable efficient deployment for AI training and inference workloads; rack-scale liquid-cooled solutions address higher power density and performance requirements by leveraging direct-to-chip liquid cooling technologies, including Coolant Distribution Units, cold plates, manifolds, and end-to-end thermal management, delivering optimized heat transfer and improved energy efficiency, while supporting leading-edge hardware such as NVIDIA HGX Blackwell, B200, H100/H200, and AMD Instinct accelerators to enable rapid deployment and stable operation of large-scale AI superclusters. The company ensures seamless transition from design to on-site deployment through a seven-stage integration process and emphasizes a single-vendor responsibility model to reduce complexity and total cost of ownership.

Supermicro’s rack-scale AI solution is a pre-integrated, high-density computing system built around Rack Scale Solutions and conforms to the definition of a Rack-scale AI Solution for Datacenter, optimizing AI training and inference workloads through rack-level form factors and delivering plug-and-play, fully configured and validated single-rack or multi-rack systems. The solution provides end-to-end integration services through a seven-stage process spanning design, assembly, testing, and deployment, supports large-scale AI clusters such as xAI Colossus with 100,000 NVIDIA Hopper GPUs, and ensures rapid delivery through factory-scale manufacturing capacity of up to 5,000 racks per month; core components include high-density GPU servers (such as 4U 8-GPU systems equipped with NVIDIA HGX B200/H100/H200 or AMD Instinct MI300X/MI325X), processors (4th Gen Intel Xeon Scalable or AMD EPYC), networking (NVLink switches, 1:1 GPU networking, and management switches), cooling (CDUs and vertical/horizontal CDMs supporting liquid cooling), and power (33 kW power racks); key features include high-density optimization (up to 72 NVIDIA Blackwell GPUs or 64 latest-generation GPUs per rack with 1:1 networking and all-flash NVMe storage), customization support (in collaboration with OEM partners, offering air or liquid cooling options and software management), integrated cooling (direct liquid cooling reducing data center power costs by 40%, noise by 55%, and cooling infrastructure power by 89%), and electrical control (optimized cabling, power distribution, monitoring, and automation); the benefits include accelerated deployment, reduced TCO, improved energy efficiency and scalability, and support for large-scale AI training and inference, HPC workloads, and turnkey supercluster transformations, ensuring stable operation in high-power environments; specifications highlight AI/LLM racks (48U/50U supporting 64–72 GPUs, 8–18 server nodes, 1 CDU, 1–2 vertical CDMs, 0–8 horizontal CDMs, and 2–9 switches), enterprise racks (48U with 76-node BigTwin), and high-density HPC racks (48U with 80-blade SuperBlade), compatible with NVIDIA, AMD, and Intel hardware, with L12 testing validation and global support.

4.2. AMD

AMD is a semiconductor company centered on high-performance and adaptive computing, with its enterprise business primarily spanning key domains such as data centers, cloud computing, high-performance computing, and artificial intelligence. According to AMD’s official press releases, Investor Day materials, and annual reports, its overall business strategy is built around the coordinated evolution of CPUs, GPUs, and accelerated computing platforms, emphasizing the deep integration of general-purpose computing and accelerated computing to deliver scalable and customizable compute platforms for cloud service providers, hyperscale data center operators, and enterprise customers. At the enterprise level, AMD consistently underscores an open ecosystem and platform-oriented approach, repeatedly stating in official communications that its products and solutions are designed to support diverse software stacks and system architectures, enabling customers to flexibly deploy computing resources across different scales and application scenarios; at the same time, AMD positions the data center as a long-term strategic priority and has clearly articulated in public disclosures that its enterprise business is not focused solely on single-chip performance, but rather on energy efficiency, scalability, and long-term sustainable operations across the entire platform lifecycle.

With respect to rack-scale AI capabilities for data centers, AMD has consistently positioned its Instinct accelerator family together with EPYC processors as the core components of a Rack-scale AI Solution for Datacenter in official announcements and joint statements with partners, and delivers rack-scale offerings for large-model training and inference through close collaboration with system OEMs and cloud service providers. In terms of form factors, AMD’s publicly disclosed solutions currently fall into two primary categories: rack-scale air-cooled solutions and rack-scale liquid-cooled solutions. Rack-scale air-cooled solutions focus on enabling high-density AI deployments within existing data center infrastructure, emphasizing coordinated design and standardized integration of compute, networking, and power delivery within the rack to reduce deployment complexity and accelerate time to delivery; rack-scale liquid-cooled solutions are primarily targeted at higher-power and higher-density AI workloads and are described in official technical materials as a critical pathway for supporting next-generation large-scale AI training, improving energy efficiency and alleviating thermal density constraints through the introduction of liquid cooling and high-power delivery at the rack level. Across its enterprise disclosures, AMD repeatedly emphasizes that its rack-scale AI solutions are not isolated hardware assemblies, but are advanced through system-level integration, open standards, and alignment with overall data center architectures, reflecting a strategic shift in AI infrastructure from competition at the single-chip level toward competition in platforms and system capabilities.

AMD’s rack-scale AI solution is a pre-integrated, high-density computing system centered on the “Helios” platform and aligns with the definition of a Rack-scale AI Solution for Datacenter, optimizing AI training and inference workloads through rack-level form factors and delivering plug-and-play, fully configured and validated single-rack or multi-rack systems. The solution is designed based on Meta’s OCP Open Rack for AI (ORW) open standard and incorporates core components including AMD Instinct™ MI450 series GPUs (up to 432 GB of HBM4 memory per GPU and 19.6 TB/s of bandwidth), AMD EPYC™ CPUs, Pensando™ DPUs, and scalable networking, ensuring an end-to-end open and programmable infrastructure; key features encompass seamless integration—from AI acceleration with AMD Instinct GPUs to data processing with EPYC CPUs and high-speed data access enabled by Pensando networking—high-density optimization (up to 72 GPUs per rack delivering 1.4 exaFLOPS FP8 and 2.9 exaFLOPS FP4 performance, 31 TB of total HBM4 memory, and 1.4 PB/s of aggregate bandwidth), customization support (compatibility with OEM/ODM partners such as HPE and Broadcom and support for UALoE standard Ethernet scaling), integrated cooling (support for direct liquid cooling to address high-power-density environments), and electrical control (custom cabling, power distribution, monitoring, and automation); the benefits include accelerating AI transformation from enterprise deployments to gigawatt-scale data centers, improving energy efficiency and interoperability, and delivering breakthrough performance to support trillion-parameter model training, large-scale inference, and agentic AI applications; specifications highlight next-generation CDNA architecture, leading-class memory capacity and bandwidth, and enhanced system design and customer enablement capabilities through the acquisition of ZT Systems, ensuring efficient and scalable operation across both cloud and enterprise environments.

4.3. HIPER Global

HIPER Global is a compute solutions architecture company serving global technology and defense OEM customers, with its core business centered on the design, engineering, and delivery of customized computing platforms and systems for diverse industries. The company provides end-to-end compute solutions ranging from server platforms, storage, and embedded systems to rack-scale equipment, while supporting the full lifecycle from architectural design and engineering manufacturing to global delivery and lifecycle services, enabling customers to address complex computing requirements across AI, high-performance computing, automation, broadcast media, and data center environments. As a vendor-agnostic solution provider, HIPER Global emphasizes the development of open-standards-based, high-density, and high-reliability hardware systems tailored to customer needs, meeting the rapidly evolving demands for innovation while working alongside industry partners to advance the deployment and operation of next-generation computing infrastructure.

In the area of Rack-scale AI Solution for Datacenter, HIPER Global focuses on integrating high-performance compute and thermal management through rack-scale technologies to support densely deployed computing environments, helping customers transform large-scale data and AI workloads into manageable infrastructure capabilities. Its rack-scale AI solutions include rack-level air-cooled solutions designed to address moderate-density AI and high-performance computing thermal requirements through optimized airflow and structural design, incorporating integrated air-cooling management components to maintain system performance and stability, as well as rack-level liquid-cooled solutions that utilize closed-loop liquid cooling technologies to enhance thermal efficiency and energy utilization under high-density, high-heat-flux AI compute nodes, representing an increasingly important approach in AI and high-performance computing as traditional air cooling reaches its limits. By combining these rack-scale thermal management technologies with its high-density compute platforms, HIPER Global delivers scalable and reliable rack-level AI infrastructure capabilities for data centers, AI acceleration platforms, and related industries.

HIPER Global’s rack-scale AI solutions are pre-integrated, high-density computing systems purpose-built for data centers and aligned with the definition of Rack-scale AI Solution for Datacenter, namely optimizing AI training and inference workloads through rack-based form factors and delivering plug-and-play, fully configured, and validated single-rack or multi-rack systems. These solutions are manufactured using precision replication processes to ensure strict adherence to requirements, encompassing core components such as L12 hybrid cloud, full cloud solutions, proprietary racks, high-density systems, custom development, integrated cooling, and electrical control panels; key characteristics include pre-integrated design enabling seamless deployment from design through delivery, high-density optimization to maximize performance within constrained space, cooling, and power envelopes, custom support compatible with proprietary hardware and software, integrated cooling for temperature control in high-density environments, and electrical control with customized cabling, power distribution, monitoring, and automation; the resulting benefits include efficient and scalable data center transformation, support for rapid rollout of common scenarios alongside customization for unique requirements, and reliable operation under demanding conditions; while specific compute density or power specifications are not detailed, the solutions emphasize subcomponent-level optimization and scalable form factors suitable for cloud-driven AI workloads, offering hybrid cloud configurations to support emerging technologies.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Rack-scale AI Solution for Datacenter market is segmented as below:

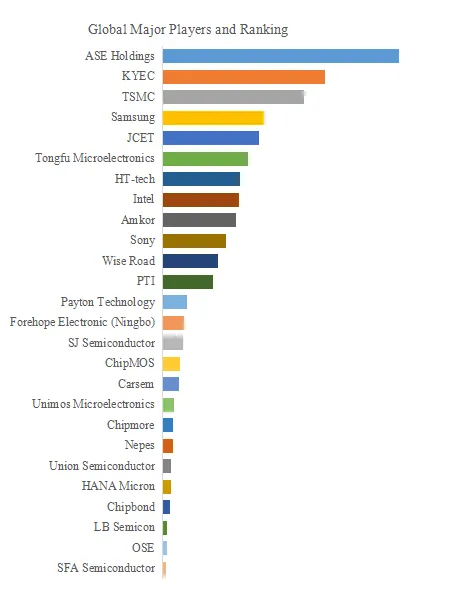

By Company

Supermicro

NVIDIA

Hewlett Packard Enterprise

d-Matrix

Qualcomm

Dell

GigaIO

Vertiv

Astera Labs

Penguin Solutions

HIPER Global

SourceCode

GIGABYTE

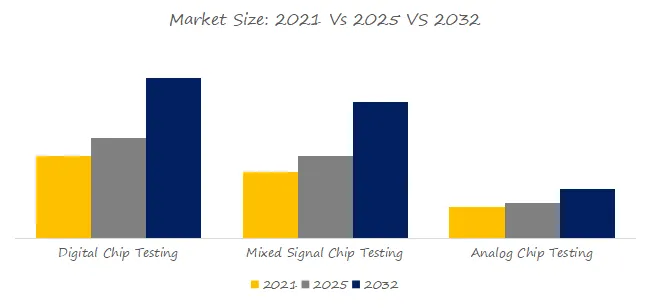

Segment by Type

Rack-scale Air-cooling Solution

Rack-scale Liquid-cooling Solution

Segment by Application

Oil & Gas

Scientific Research

Finance

Automotive

Healthcare

Others

Each chapter of the report provides detailed information for readers to further understand the Rack-scale AI Solution for Datacenter market:

Chapter 1: Introduces the report scope of the Rack-scale AI Solution for Datacenter report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Rack-scale AI Solution for Datacenter manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Rack-scale AI Solution for Datacenter market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Rack-scale AI Solution for Datacenter in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Rack-scale AI Solution for Datacenter in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Rack-scale AI Solution for Datacenter competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Rack-scale AI Solution for Datacenter comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Rack-scale AI Solution for Datacenter market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Rack-scale AI Solution for Datacenter Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Rack-scale AI Solution for Datacenter Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Rack-scale AI Solution for Datacenter Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp