Global Leading Market Research Publisher Global Info Research announces the release of its latest report “Oil and Gas Equipment Forgings – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”.

For oil and gas operators, equipment failure in upstream operations is not merely an inconvenience—it is a safety, environmental, and financial catastrophe. A single wellhead component failure can cost US$ 1-3 million in direct remediation, plus regulatory fines and production downtime measured in weeks. The root cause often traces back to oil and gas equipment forgings—the forged steel components that form the pressure-containing boundaries of wellheads, Christmas trees, fracturing manifolds, and deepwater equipment. These critical components must withstand extreme pressures (exceeding 20,000 psi), hydrogen sulfide (sour service) corrosion, Arctic temperatures (-60°C), and 30+ year service life requirements. This report delivers the data-driven intelligence required to navigate this strategically vital component market, addressing the core needs of procurement executives, quality managers, and energy infrastructure investors.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/5764718/oil-and-gas-equipment-forgings

Market Size & Growth Trajectory (2026-2032)

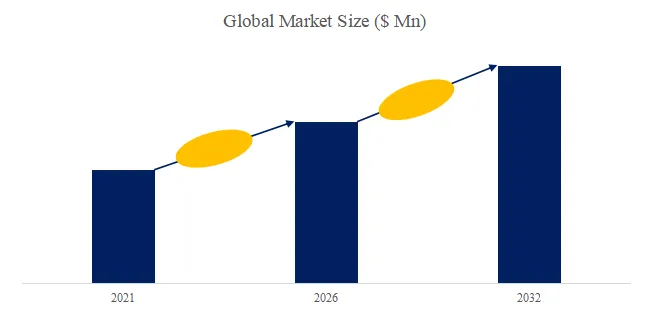

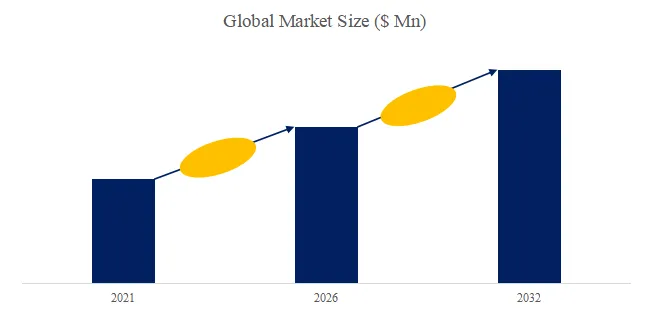

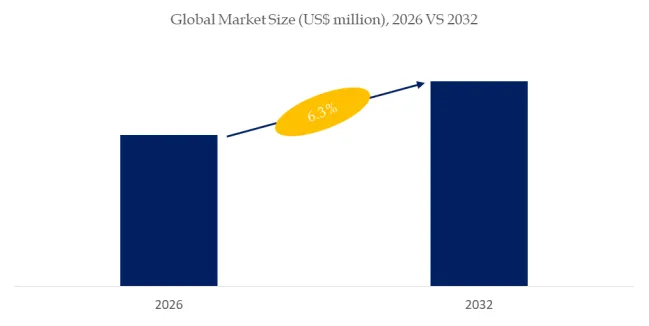

Based on historical analysis (2021-2025) and forecast calculations (2026-2032), the global market for Oil and Gas Equipment Forgings was valued at approximately US$ 2,850 million in 2025 and is projected to reach US$ 3,980 million by 2032, growing at a compound annual growth rate (CAGR) of 4.9% from 2026 to 2032. This growth is driven by three primary factors: (1) increasing complexity of oil and gas extraction (deepwater, ultra-deepwater, and high-pressure/high-temperature HPHT reservoirs) requiring higher-grade forgings; (2) aging upstream infrastructure replacement cycle (equipment installed during 2005-2010 shale boom reaching 15-20 year design life); and (3) renewed offshore drilling activity following the post-COVID recovery in oil prices. In the first half of 2026, preliminary data indicates a 6.8% year-on-year increase in oil and gas forging shipments, with deepwater equipment components and fracturing equipment components growing at the fastest rates.

Product Definition & Technology Landscape

Oil and Gas Equipment Forgings are engineered metal components produced through open-die or closed-die forging processes, designed to contain high-pressure hydrocarbons in upstream production environments. These components are manufactured from low-alloy steels (ASTM A694 F65, AISI 4140, 4330V), stainless steels (17-4 PH, 316L), and nickel-based alloys (Inconel 625, 718) depending on service conditions.

Primary Forging Types and Their Applications:

Wellhead and Christmas Tree Components represent the largest segment by value. These forgings include casing heads, tubing heads, adapters, and valve bodies that control flow from the wellbore. They must meet NACE MR0175/ISO 15156 requirements for sour service (H2S resistance) and API 6A specifications for pressure ratings (2,000-20,000 psi). Typical forgings range from 4 to 16 inches in diameter with wall thicknesses of 1-4 inches. This segment represents approximately 40% of market value.

Deepwater Equipment Components are the most technically demanding segment. These forgings include subsea tree bodies, connectors, and manifold components rated for water depths exceeding 3,000 meters. They require specialized low-temperature toughness (minimum 60J at -46°C) and exceptional cleanliness (ultrasonic testing to ASTM A388 Level 1). Subsea forgings often use duplex stainless steels (F51, F53) for corrosion resistance. This segment represents approximately 25% of market value.

Fracturing Equipment Components include manifolds, swivels, and plug valves used in hydraulic fracturing operations. These forgings face extreme pressure cycling (15,000 psi pulsed up to 30,000 psi) and abrasive slurry flow. High-cycle fatigue resistance and wear-resistant bore coatings are critical requirements. This segment has grown rapidly with the shale revival, representing approximately 20% of market value.

Drilling Equipment Components include top drive components, rotary table forgings, and blowout preventer (BOP) parts. These require high impact toughness (minimum 50J at -20°C) and compliance with API Spec 16A. This segment represents the remaining 15% of market value.

Why Forging Quality Determines Operational Safety: A single wellhead forging failure during hydraulic fracturing can release high-pressure frac fluid, causing surface equipment damage and environmental releases. NACE MR0175 compliance requires verification of sulfide stress cracking resistance through standardized H2S exposure testing. Leading operators now require 100% ultrasonic inspection (ASTM A388) plus magnetic particle inspection (ASTM E709) on all pressure-containing forgings, with acceptance criteria significantly stricter than API minimums.

Key Industry Characteristics & Strategic Implications

Extreme Sector Differentiation: Onshore vs. Underwater/Deepwater Equipment

While both onshore and underwater applications require oil and gas equipment forgings, the technical requirements and supply chain dynamics differ substantially.

In Underwater/Deepwater Mining Equipment (subsea applications), accounting for approximately 35% of market value, forgings must withstand seawater corrosion (requiring duplex stainless steel or nickel alloy cladding), extreme hydrostatic pressure, and challenging inspection logistics (no visual access once installed). Subsea equipment design life extends to 30+ years with zero maintenance access. Forgings require full traceability from steel melt to final machining, with documentation packages exceeding 1,000 pages per component. Key players serving this segment include Ellwood Group Incorporated, Siderforgerossi Group, and Aubert & Duval.

In Onshore Mining Equipment (surface production and fracturing), representing approximately 65% of market value, forgings face less severe corrosion challenges but must accommodate wider temperature ranges (-40°C to +80°C) and more frequent pressure cycling (frac operations cycle 50-100 times per well). Onshore supply chains are more regionalized, with shorter lead times (6-12 months) and lower documentation requirements. Key players include FRISA, Scot Forge, and Patriot Forge.

The HPHT and Sour Service Capacity Constraint

Global production capacity for high-pressure (15,000+ psi) and sour service (H2S-resistant) forgings is concentrated among fewer than 12 forging manufacturers worldwide capable of producing the required metallurgical quality. A 2026 industry survey by the International Association of Drilling Contractors identified HPHT-compatible wellhead forgings as a critical supply chain constraint for deepwater projects in the Gulf of Mexico and offshore Brazil.

Technology Integration: NACE Compliance and Inclusion Control

Leading forging manufacturers have invested heavily in steelmaking capabilities to achieve the material cleanliness required for sour service applications. Vacuum degassing (VD) reduces hydrogen content (target below 1.5 ppm) and oxygen content (target below 20 ppm), while calcium treatment modifies inclusion morphology to resist H2S cracking. In Q1 2026, Ellwood Group Incorporated announced expanded NACE MR0175 qualification coverage for its 10,000-ton press facility, enabling production of 18-inch diameter wellhead forgings meeting the most stringent sour service Class 3 requirements.

User Case Study: Subsea Wellhead Forgings for Gulf of Mexico

Project: Shenandoah Deepwater Development, Gulf of Mexico (water depth: 1,750 meters)

Challenge: Project required 24 subsea wellhead forging sets (including tubing head housings, casing hangers, and adapters) rated for 20,000 psi working pressure and NACE MR0175 Class 3 sour service. Delivery window was 24 months from contract award.

Solution (2025-2026): Ellwood Group Incorporated supplied forgings using vacuum degassed AISI 4330V steel modified with 0.25% molybdenum for enhanced H2S resistance. Each forging underwent 100% ultrasonic inspection (ASTM A388 Level 1) and hardness testing (max 22 HRC for sour service compliance).

Results (verified by project documentation):

All 24 forging sets passed first-pass ultrasonic inspection (zero rejections), compared to industry average of 8-12% rejections for similar HPHT sour service specifications. Hardness across all forgings was maintained within 18-22 HRC range, meeting NACE Class 3 requirements. Delivery was completed 15 days ahead of schedule. The Shenandoah project achieved first oil in August 2026, 4 months ahead of initial schedule, with zero wellhead-related equipment failures in the first 6 months of operation.

Recent Policy and Technology Developments (Last 6 Months)

Regulatory Update (March 2026): The Bureau of Safety and Environmental Enforcement (BSEE) revised its Well Control Rule, requiring that all wellhead and Christmas tree forgings installed on US Outer Continental Shelf projects must be traceable to a specific steel heat and manufacturer, with NDT records retained for 30 years. This has accelerated adoption of digital tracking systems among forging suppliers.

Technology Breakthrough (April 2026): A research consortium including Vallourec and Daido Steel demonstrated the first large-diameter (24-inch) wellhead forging produced using hydrogen-direct reduced iron (H-DRI) feedstock, reducing CO2 emissions by 78% compared to conventional blast furnace routes. The forging met all API 6A PR2 performance requirements. Commercial availability is expected by 2028.

Corporate Announcement (February 2026): Baker Hughes announced in its annual report that it had qualified new forging suppliers in India and Saudi Arabia to diversify its wellhead component supply chain. The company expects 40% of its wellhead forgings to come from non-Chinese sources by 2027, up from 15% in 2024.

Policy Incentive (January 2026): The US Department of Energy announced US$ 50 million in funding for domestic forging capacity expansion under the Advanced Energy Manufacturing and Recycling Grant Program, prioritizing projects producing HPHT and sour service forgings for oil and gas and geothermal applications.

Exclusive Industry Observation: Standard vs. Custom Forging Production

A unique analytical framework introduced in this report distinguishes between standardized forging production (API-spec wellhead components produced to industry norms like API 6A) and custom-engineered production (project-specific deepwater or HPHT components with unique geometries, material grades, and testing requirements).

For standardized production, efficiency and API certification drive competitiveness. Manufacturers optimize press utilization, maintain API Q1 quality systems, and stock common sizes for rapid delivery. Lead times are shorter (4-8 months) and unit costs are lower (typically US$ 5,000-10,000 per metric ton). Margin pressure from low-cost competitors is significant.

For custom-engineered production, engineering capability and quality consistency are paramount. Manufacturers must accommodate specialized steel grades (including nickel alloys), complex geometries (including integral flanges and connector profiles), and customer-specific inspection plans. Lead times are longer (12-18 months) and unit costs are higher (US$ 12,000-25,000 per metric ton). Customer relationships are deeper and switching costs are substantial.

Leading manufacturers—including Ellwood Group, Siderforgerossi, and Aubert & Duval—have developed hybrid models: standardized blanks for onshore wellhead components combined with custom finishing and testing for deepwater projects, optimizing both utilization and differentiation.

Strategic Outlook and Analyst Recommendations

The Oil and Gas Equipment Forgings market is undergoing a fundamental transformation, driven by increasing well complexity, supply chain regionalization, and decarbonization pressures. Key strategic priorities for industry stakeholders include:

For Oil and Gas Operators and OEMs (Baker Hughes, Schlumberger, Halliburton, NOV):

- Extend wellhead forging lead times to 18+ months for deepwater HPHT projects and qualify multiple forging suppliers per component family to mitigate concentration risk.

- Implement digital tracking of material certificates and NDT data to accelerate quality documentation review (currently 8-10 weeks per wellhead assembly).

- Specify green steel (H-DRI-based) grades where available to align with Scope 3 decarbonization targets.

For Forging Manufacturers:

- Investment in vacuum degassing and NACE MR0175 qualification will differentiate premium suppliers from commodity producers, enabling access to higher-margin deepwater and HPHT contracts.

- Carbon footprint verification (third-party audited, product-level) is becoming a competitive requirement for European and North American operators; early adopters will capture green premium pricing (estimated 10-15%).

- Regional capacity expansion in North America (driven by DOE grants) and Saudi Arabia (driven by Aramco In-Kingdom Total Value Add program) offers subsidies covering 15-30% of capital costs.

For Energy Investors:

- Monitor HPHT and sour service forging capacity utilization as a leading indicator for deepwater project execution risk and potential wellhead delivery delays.

- Value manufacturers with hybrid standard-custom production models at higher multiples (projected 11-14x EBITDA versus 7-9x for pure standardized players).

- Track OEM supplier diversification announcements—qualification of new non-Chinese forging suppliers creates mid-term investment opportunities in India, Saudi Arabia, and Eastern Europe.

As upstream oil and gas investment recovers and well complexity continues to increase, oil and gas equipment forgings will remain a critical supply chain node and value capture point. Companies and investors who understand the technical, capacity, and policy dynamics of this specialized upstream oil and gas component segment will be best positioned to capitalize on the ongoing energy supply expansion.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

Global Info Research

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp