1. AI Short Drama Market Summary

AI short dramas refer to short video storylines generated or created with the assistance of artificial intelligence technology. They typically range from 1 to 5 minutes in length and encompass virtual characters, automated script generation, voice-over narration, and scene rendering. Their core characteristics are high automation, low cost, rapid production, and the ability to be personalized according to user preferences. Compared to traditional short dramas, AI short dramas not only lower the creative threshold but also enable real-time iteration and optimization of content on social media and video platforms, thus meeting the demand for fragmented content consumption.

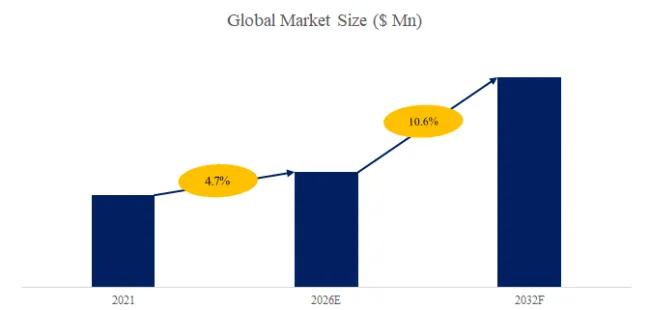

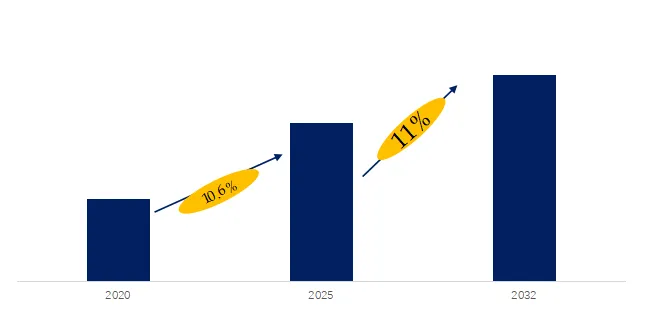

According to the latest research report from QYResearch, in terms of market size, the global AI Short Drama market size is projected to grow from USD 865 million in 2025 to USD 1.8 billion by 2032, at a CAGR of 11.00 % during the forecast period.

Figure00001. Global AI Short Drama Market Revenue Growth Rate, 2021-2032

Above data is based on report from QYResearch: Global AI Short Drama Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

2 Introduction of Major Manufacturers of AI Short Drama

| Serial Number | Company |

| 1 | Vigloo |

| 2 | Dashverse |

| 3 | BitRing |

| 4 | Bona Film Group |

| 5 | Huayi Brothers |

| 6 | Guomai Culture |

| 7 | Xinmei Hongxing |

| 8 | Timeaxis |

| 9 | Xinghe Yingchuang |

| 10 | Xuanjia Technology |

| 11 | China Wit Media |

| 12 | Hangzhou Liao Culture |

Source: Third-party data, QYResearch Research Team

According to a survey by QYResearch’s Leading Enterprise Research Center, global AI Short Drama manufacturers include Vigloo, Dashverse, BitRing, Bona Film Group, Huayi Brothers, etc. By 2025, the top five global manufacturers will hold approximately 33% of the market share.

Introduction to Key Companies

Company 1

| Vigloo | Description |

| Company Introduction | Vigloo is an emerging technology company specializing in AI content generation and short-form drama entertainment, dedicated to applying artificial intelligence technology to film and television creation and content distribution. By integrating generative AI, virtual character modeling, and automated editing technologies, the company has created an efficient content production system, significantly reducing the cost and time required for short-form drama production. Targeting global mobile internet users, Vigloo focuses on fragmented entertainment consumption scenarios, promoting the integration of short videos and narrative content, and exploring intelligent and scalable digital content production and monetization models. |

| Product Introduction | Vigloo’s AI micro-drama product centers on automatically generated narrative content. Through AI scriptwriting, virtual actors, and an intelligent editing system, it automates the entire process of short drama production from concept to final product. The platform allows users to input themes or keywords, and the system generates scripts, storyboards, and video content suitable for various genres such as romance, suspense, and urban dramas. The product emphasizes high-frequency updates and personalized recommendations to meet users’ fragmented viewing needs, while also supporting multilingual output and global distribution, driving the large-scale production and commercial application of AI-driven short-form drama content. |

Source: Third-party data, QYResearch Research Team

Company 2

| Dashverse | Description |

| Company Introduction | Dashverse is a technology company focused on AI-powered interactive entertainment and digital content innovation, dedicated to building an immersive content creation and consumption platform. The company combines generative artificial intelligence, virtual reality, and real-time interactive technologies to provide users with entirely new entertainment experiences. Dashverse emphasizes user participation and content co-creation, lowering the barrier to entry through technology so that ordinary users can participate in story creation and content production. Its business encompasses AI video generation, interactive short dramas, and a virtual character ecosystem, driving the entertainment industry towards intelligence and personalization. |

| Product Introduction | Dashverse’s AI micro-drama product emphasizes an “interactive story experience,” where users are not only viewers but also participate in the plot’s development. The platform uses AI to generate multi-branch scripts, adjusting the story’s direction in real time based on user choices to achieve a personalized viewing experience. The system combines virtual character generation and voice synthesis technologies to quickly generate video content and supports real-time feedback and plot iteration. This product is suitable for mobile entertainment and social sharing scenarios, enhancing interactivity and immersion to increase user stickiness and explore new models of AI-driven content entertainment. |

Source: Third-party data, QYResearch Research Team

Company 3

| BitRing | Description |

| Company Introduction | BitRing is an innovative company focused on the integration of digital entertainment and blockchain technology, dedicated to building a decentralized content ecosystem. BitRing combines AI-generated content technology with blockchain-based rights confirmation mechanisms to provide creators with an integrated solution for content production, distribution, and revenue management. BitRing emphasizes content copyright protection and creator incentives, using technology to achieve transparent revenue distribution and digital asset management, driving the digital entertainment industry towards decentralization and intelligence. |

| Product Introduction | BitRing’s AI-powered micro-drama product integrates generative AI and blockchain technology to achieve automatic generation and copyright confirmation of short drama content. The platform rapidly produces various types of short drama content through AI scriptwriting and video generation tools, while simultaneously putting works on the blockchain to ensure copyright ownership and revenue distribution. Users can both watch and participate in creation, earning revenue incentives through the platform. The product supports multi-terminal distribution and digital asset trading, creating a closed loop of “creation-distribution-monetization” and exploring innovative business models combining AI content and Web3. |

Source: Third-party data, QYResearch Research Team

3 AI Short Drama Industry Chain Analysis

| Industry Chain | Description |

| Upstream | The upstream of AI-powered micro-dramas primarily includes AI technology providers, data suppliers, virtual character modeling companies, and film and television material libraries. AI algorithm providers offer generative scriptwriting, natural language processing, speech synthesis, motion capture, and virtual actor rendering technologies, enabling efficient and automated production of micro-dramas. Data suppliers provide a wealth of training materials, including text, audio, video, and user behavior data, to enhance the realism and diversity of the generated content. Furthermore, the upstream also encompasses copyright content providers, IP licensing agencies, and creative design companies, providing resource guarantees for the micro-drama’s plot construction, character design, and scene design, and providing the technological foundation and content support for the midstream production stage. |

| Midstream | The midstream stage is the core production and integration phase of AI-powered micro-dramas, including content production companies, virtual actor operation teams, and platform developers. Production companies integrate upstream technologies and materials, generating scripts, virtual character movements, voices, and scenes through AI to form complete micro-drama content; virtual actor teams are responsible for character image maintenance, movement optimization, and interactive scene design to enhance the audience’s immersive experience. Platform developers publish the works to short videos, social media, or mobile applications, achieving multi-channel distribution and user interaction. Meanwhile, the midstream also involves content quality monitoring, algorithm optimization, and user data analysis, enabling micro-dramas to maintain high-efficiency production while continuously improving audience experience and content innovation. |

| Downstream | The downstream mainly consists of micro-drama distribution platforms, operators, and end users. Short video platforms, social media, and mobile applications provide content display and interactive interfaces, allowing viewers to watch, comment, share, and participate in plot interactions at any time. Operators are responsible for user management, promotion, traffic optimization, and fan economy operations, such as advertising placement, membership fees, virtual merchandise sales, and IP derivative development, realizing the commercial value of the content. The downstream also includes collecting audience feedback, behavioral data, and preference analysis, providing references for midstream production teams to optimize scripts, virtual characters, and interactive designs, achieving a closed-loop industry chain. The downstream directly determines the user experience, traffic scale, and market commercial potential of micro-dramas. |

Source: Third-party data, QYResearch Research Team

4 AI Short Drama Industry Development Trends, Opportunities, Obstacles and Industry Barriers

Development Trends:

1. Generative AI Technology Drives Content Innovation. Globally, AI-powered micro-dramas are rapidly developing based on generative artificial intelligence technology, including AI scriptwriting, virtual actor modeling, automatic voice-over, and intelligent special effects. AI can efficiently generate diverse plots and characters, significantly reducing creation costs while accelerating content production, leading to explosive growth in the micro-drama market.

2. Short Video Platforms Drive Market Expansion. With the global popularity of short video platforms, AI-powered micro-dramas have gained widespread dissemination channels. The short duration, fragmented format, and strong interactivity of the content meet users’ fast-paced viewing needs, driving the commercialization of the micro-drama industry and user growth, while simultaneously fostering deep ecological cooperation between platforms and content creators.

3. The Trend of Virtual IP and Multimedia Integration. AI-powered micro-dramas combine virtual idols, game IPs, and social interaction to achieve cross-media integration. Virtual actors and interactive plots not only enhance the audience experience but also create new models for derivative product development, advertising placement, and the fan economy, driving the industry chain towards diversification.

Development Opportunities:

1. Reduced Production Costs and Barriers: Traditional film and television production requires a large number of actors, sets, and shooting equipment. AI micro-dramas, however, can quickly complete content production through virtual actors and generative scripts, reducing manpower, time, and set costs, and providing opportunities for small and medium-sized production companies and individual creators.

2. Significant Cross-Platform Commercialization Potential: AI micro-dramas can quickly adapt to short videos, social media, live streaming platforms, and mobile applications, expanding multi-channel commercialization paths. Models such as product placement, paid content, and fan donations make micro-dramas a new profit growth point, driving innovation in the global entertainment industry.

3. Driving the Development of Virtual Idols and the Fan Economy: Virtual actors and AI characters can interact with viewers, enhancing immersive experiences and fan loyalty. Through derivative products, IP licensing, and cross-platform interactive activities, AI micro-dramas drive the development of the virtual idol economy, creating new cultural and commercial value.

Hindering Factors:

1. Technological Maturity and Creative Limitations. Despite the rapid development of AI-generated content, plot innovation, character emotional expression, and scene detail still fall short of traditional film and television standards. Technological limitations may lead to content homogenization or a lack of depth, impacting audience experience and long-term user retention.

2. Copyright and Legal Risks. When AI-generated short dramas use existing source material, IP, or data for training, there are risks related to copyright ownership and intellectual property disputes. The lack of clear legal regulations may restrict the rapid development of the industry and increase the legal responsibilities of creators and platforms.

3. Audience Awareness and Acceptance. Some users have limited acceptance of virtual actors and AI-generated content, preferring live actors or high-quality original content. Insufficient user trust and emotional identification may affect the traffic, monetization, and market penetration of AI-generated short dramas.

Barriers:

1. AI Technology and Data Barriers: Leading companies possess high-precision AI generation technology, virtual actor modeling, and large-scale training data, enabling them to rapidly produce high-quality micro-dramas. This technological accumulation and data advantage form a significant barrier, making it difficult for new entrants to match their creative efficiency and content quality in the short term.

2. IP and Content Ecosystem Barriers: Companies build fan bases and business cooperation networks by accumulating virtual characters, IP licensing, and multi-platform content ecosystems. This mature ecosystem is difficult for new entrants to replicate, forming a long-term competitive advantage in the industry.

3. Platform and Distribution Channel Barriers: Partnerships with short video platforms, social media, and mobile applications, as well as priority traffic and recommendation mechanisms, are important competitive barriers for AI micro-drama companies. Mastering distribution channel advantages allows for rapid user and traffic acquisition, posing significant challenges for new entrants in promotion and monetization.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading Global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are Globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp