Introduction (Covering Core User Needs: Pain Points & Solutions):

Global Leading Market Research Publisher QYResearch announces the release of its latest report “Sticky Gel Carrier Boxes – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032″. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Sticky Gel Carrier Boxes market, including market size, share, demand, industry development status, and forecasts for the next few years.

For semiconductor manufacturers, medical device producers, and jewelry designers, handling and transporting small, fragile, or contamination-sensitive components presents persistent challenges: mechanical clips can scratch or damage surfaces; loose components shift during transport causing impact damage; electrostatic discharge (ESD) can destroy sensitive electronics. Sticky gel carrier boxes utilize a tacky, non-residue gel pad (typically silicone or polyurethane-based) that securely holds components in place via light adhesion, preventing movement during transport while allowing easy removal with tweezers or vacuum pickup tools. These boxes are designed to be cleanroom-compatible, ESD-safe, and free from silicone oil migration or outgassing that could contaminate sensitive surfaces. As semiconductor device geometries shrink (3nm, 2nm, 1.4nm), medical implantable devices demand zero-defect handling, and high-value jewelry requires damage-free transport, sticky gel carrier boxes are transitioning from niche product to essential packaging for precision component logistics.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)

https://www.qyresearch.com/releases/5985530/sticky-gel-carrier-boxes

1. Market Sizing & Growth Trajectory (With 2026–2032 Forecasts)

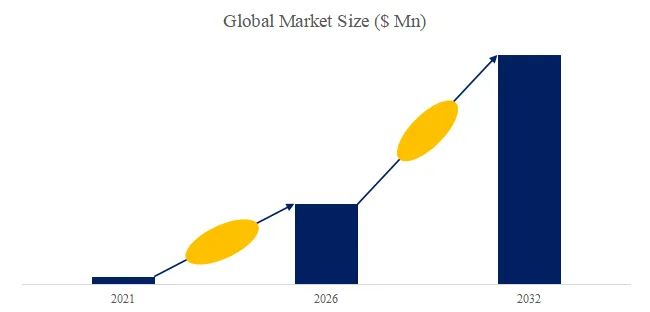

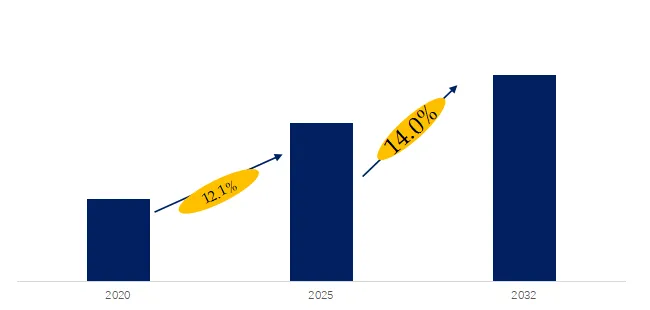

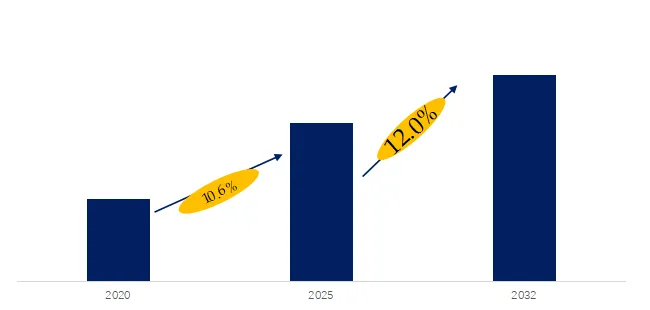

The global market for Sticky Gel Carrier Boxes was estimated to be worth approximately US$80 million in 2025 and is projected to reach US$160 million by 2032, growing at a CAGR of 10.5% from 2026 to 2032. This above-average growth is driven by three converging factors: (1) increasing semiconductor wafer and die production (400+ fabs globally), (2) demand for contamination-free handling of medical components (implants, surgical tools, diagnostic devices), and (3) growth in high-value jewelry and watch component manufacturing.

By size format, 55mm x 56mm sticky gel carrier boxes dominate with approximately 50% of market revenue (standard for small dies, chips, components). 75mm x 56mm accounts for 30% (larger dies, wafers, multiple components), and others for 20%. By application, semiconductor accounts for approximately 60% of market revenue, medical for 20%, jewelry for 15%, and others for 5%.

2. Technology Deep-Drive: Gel Adhesion Properties, Cleanroom Compatibility, and ESD Safety

Technical nuances often overlooked:

- Adhesive gel pads for wafer and die handling gel properties: Tack level (low, medium, high) – adjustable by gel formulation. Adhesion force: 5-50 g/cm² (peel test). No residue (clean release). Non-outgassing (low VOC, no silicone oil migration). Temperature range: -40°C to +150°C (storage, transport). UV stable. Shelf life: 2-5 years.

- Contamination-free sample transport box features: ESD-safe (surface resistivity 10⁶-10⁹ ohms, static dissipative). Cleanroom compatible (Class 10-100,000). Low particle generation (ISO Class 5-7). Chemical resistance (acids, bases, solvents). Autoclavable (some models). Reusable (10-100 cycles). Anti-static lid and base.

Recent 6-month advances (October 2025 – March 2026):

- MSE Supplies launched “MSE Sticky Gel Carrier Box” – 55mm x 56mm, low-tack gel, ESD-safe. For semiconductor die transport. Price US$10-30 per box (reusable).

- Gel-Pak introduced “Gel-Pak UltraGel” – high-tack gel for heavy components (jewelry, medical devices). 75mm x 56mm. Cleanroom packaged. Price US$15-40 per box.

- Ted Pella commercialized “Ted Pella Sticky Gel Box” – medium-tack, autoclavable, for laboratory and medical applications. Price US$12-35 per box.

3. Industry Segmentation & Key Players

The Sticky Gel Carrier Boxes market is segmented as below:

By Size Format (Box Dimensions):

- 55mm x 56mm – Standard for small dies, chips, components. Price: US$10-30 per box. Largest segment.

- 75mm x 56mm – Larger dies, multiple components, wafers. Price: US$15-40 per box.

- Other – Custom sizes (wafer trays, 2-inch, 4-inch, 6-inch, 8-inch). Price: US$20-100 per box.

By Application (End-Use Sector):

- Semiconductor (wafer dies, chips, LEDs, MEMS, sensors, photonics) – 60% of 2025 revenue. Low-tack, ESD-safe, cleanroom compatible.

- Jewelry (diamonds, gemstones, precious metals, watches) – 15% of revenue. Medium/high-tack, no residue, transparent lid (visual inspection).

- Medical (implants, surgical tools, diagnostic components) – 20% of revenue. Cleanroom compatible, autoclavable, biocompatible gel.

- Other (aerospace, defense, automotive, electronics) – 5%.

Key Players (2026 Market Positioning):

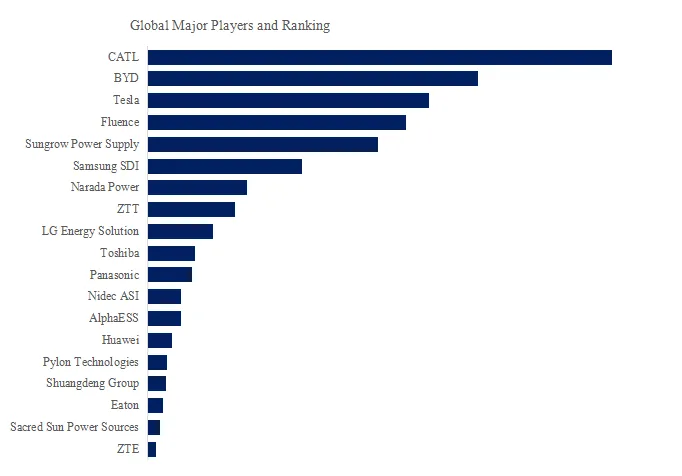

Global Leaders: Gel-Pak (USA), MSE Supplies LLC (USA), Ted Pella (USA), SPI Supplies (USA), MTI (USA), MicrotoNano (Netherlands), Nisshin EM (Japan), Nanoscience Instruments (USA), PI-KEM (UK), CrysPack (Ukraine), Hiner-pack (China), Labtech (China), Zhengzhou TCH Instrument (China).

独家观察 (Exclusive Insight): The sticky gel carrier box market is concentrated with Gel-Pak (≈25-30% market share), MSE Supplies (≈15-20%), and Ted Pella (≈10-15%) as top players. Gel-Pak (USA) is the pioneer and leader in sticky gel technology (patented gel formulations). MSE Supplies (USA) offers broad product line (wafer trays, die boxes). Ted Pella (USA) serves microscopy and laboratory markets. SPI Supplies (USA) and MTI (USA) serve semiconductor and materials science. Nisshin EM (Japan) leads in Asia-Pacific. Chinese manufacturers (Hiner-pack, Labtech, Zhengzhou TCH) are emerging with lower-cost products (30-50% below Western equivalents) but often lack cleanroom packaging and ESD certification. Gel tack levels: low tack (1-5 g/cm²) for small, light components (dies, chips). Medium tack (5-15 g/cm²) for medium components (LEDs, MEMS, medical). High tack (15-50 g/cm²) for heavy components (jewelry, large dies, tools). Cleanroom compatibility: Class 10-100 (semiconductor), Class 1,000-10,000 (medical), Class 100,000 (general). ESD-safe (surface resistivity 10⁶-10⁹ ohms) is mandatory for semiconductor (ESD-sensitive devices). Non-outgassing gel (no silicone oil migration) critical for optical components (lenses, photonics) and MEMS (stiction). Reusability: 10-100 cycles (gel retains tack, box stays clean). Box materials: anti-static polypropylene (PP) or polycarbonate (PC), conductive or dissipative. Gel pads are replaceable (some boxes have replaceable gel inserts). Shelf life: 2-5 years (unopened), 1-2 years (opened, regularly used). Storage: cool, dry, away from UV light.

4. User Case Study & Policy Drivers

User Case (Q1 2026): TSMC (Taiwan) – semiconductor foundry. TSMC adopted Gel-Pak sticky gel carrier boxes for die transport between fab and assembly (2025). Key performance metrics:

- Die damage rate: 0.01% (gel box) vs. 0.05% (mechanical clip tray) – 80% reduction

- Particle contamination: <10 particles >0.3μm (gel box) vs. <100 (clip tray) – 90% reduction

- ESD damage: 0 (gel box, ESD-safe) vs. 2 per million (clip tray) – eliminated

- Throughput (manual handling): 50% faster (gel pickup vs. clip release)

- Cost per box: US$25 (gel) vs. US$10 (clip tray) – 150% premium, justified by damage reduction (US$1,000 per die)

Policy Updates (Last 6 months):

- SEMI (Semiconductor Equipment and Materials International) – Wafer handling standard (December 2025): Recommends sticky gel carrier boxes for die transport (contamination control, ESD protection). Non-compliant methods discouraged.

- ISO 14644 (Cleanroom standards) – Handling devices (January 2026): Requires cleanroom-compatible handling devices (low particle generation, non-outgassing). Sticky gel boxes meet Class 10 requirements.

- China MIIT – Semiconductor packaging guideline (November 2025): Encourages sticky gel carrier boxes for advanced packaging (2.5D, 3D, fan-out). Domestic manufacturers (Hiner-pack, Labtech, Zhengzhou TCH) benefit.

5. Technical Challenges and Future Direction

Despite strong growth, several technical challenges persist:

- Higher cost: Sticky gel boxes cost 2-5× conventional plastic trays (US$10-40 vs. US$2-10). High-volume, low-value components may not justify cost premium.

- Gel contamination (silicone): Some gel formulations contain silicone oil (migrates to component surface, interferes with subsequent processing (bonding, coating). Silicone-free gels available (higher cost, 20-50% premium).

- Tack degradation over time: Gel tack reduces with repeated use (10-100 cycles), dust accumulation, UV exposure. Gel replacement or box replacement required.

独家行业分层视角 (Exclusive Industry Segmentation View):

- Discrete semiconductor and advanced packaging applications (dies, MEMS, LEDs, photonics) prioritize ESD-safe, low-tack, non-outgassing, cleanroom Class 10. Typically use Gel-Pak, MSE Supplies, Ted Pella, SPI Supplies, MTI, MicrotoNano, Nisshin EM, Nanoscience Instruments. Key drivers are damage reduction and contamination control.

- Flow process medical and jewelry applications (implants, diamonds, gemstones) prioritize no-residue, high-tack, autoclavable, transparent lid (visual inspection). Typically use PI-KEM, CrysPack, Hiner-pack, Labtech, Zhengzhou TCH. Key performance metrics are component security and ease of inspection.

By 2030, sticky gel carrier boxes will evolve toward RFID-enabled tracking and automated handling. Prototype boxes (Gel-Pak, MSE Supplies) integrate RFID tags for inventory management (die location, batch number, process history). Automated handling (robotic pick-and-place) with vacuum pickup tools (gel adhesion compatible). The next frontier is “dissolvable gel” – water-soluble gel for temporary bonding during processing (dissolves in final cleaning step). As adhesive gel pads for wafer and die handling enable contamination-free transport and contamination-free sample transport protects sensitive components, sticky gel carrier boxes will remain essential for semiconductor, medical, and jewelry industries.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666 (US)

JP: https://www.qyresearch.co.jp