1. Robotic Combat Platform Market Summary

Robotic combat platforms refer to autonomous or remotely controlled unmanned vehicle systems capable of performing military or tactical missions in ground environments. They are typically equipped with sensors, communication equipment, weapon modules, or auxiliary combat tools, and can perform tasks such as reconnaissance, bomb disposal, fire support, and logistical transport. Their core characteristic is reducing the direct exposure of personnel to battlefield risks while improving mission efficiency and response speed. These platforms can provide decision support for individual soldiers or squads and can also be integrated into larger-scale joint tactical networks to achieve remote command and autonomous collaboration.

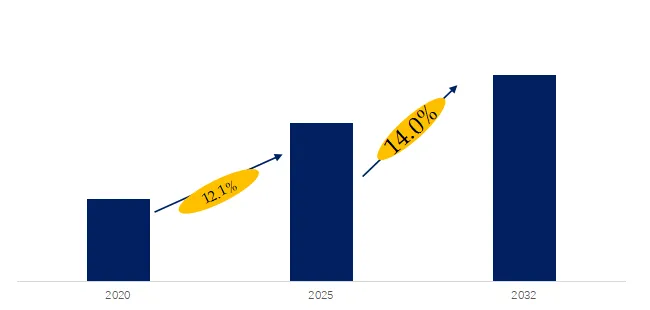

According to the latest research report from QYResearch, in 2025, global Robotic Combat Platform production reached approximately 3,900 million units, with an average global market price of around US$650,000 per unit, the industry’s gross profit margin is approximately 39%. In terms of market size, the global Robotic Combat Platform market size is projected to grow from USD 2.56 billion in 2025 to USD 6.41 billion by 2032, at a CAGR of 14% during the forecast period.

Figure00001. Global Robotic Combat Platform Market Revenue Growth Rate, 2021-2032

Above data is based on report from QYResearch: Global Robotic Combat Platform Market Report 2026-2032 (published in 2025). If you need the latest data, plaese contact QYResearch.

2 Introduction of Major Manufacturers of Robotic Combat Platform

| Serial Number | Company |

| 1 | Milrem Robotics |

| 2 | Pratt Miller |

| 3 | Textron Systems |

| 4 | Oshkosh Defense |

| 5 | IAI |

| 6 | Kalashnikov Concern |

| 7 | QinetiQ |

| 8 | Hanwha Defense |

| 9 | Elbit Systems |

| 10 | North Industries Corporation |

| 11 | Aselsan |

| 12 | Howe & Howe Technologies |

| 13 | General Dynamics Land Systems |

Source: Third-party data, QYResearch Research Team

According to a survey by QYResearch’s Leading Enterprise Research Center, global Robotic Combat Platform manufacturers include Milrem Robotics, Pratt Miller, Textron Systems, Oshkosh Defense, IAI, etc. By 2025, the top five global manufacturers will hold approximately 33% of the market share.

Introduction to Key Companies

Company 1

| Milrem Robotics | Description |

| Company Introduction | Founded in 1917 and headquartered in the United States, Oshkosh Defense is a leading global manufacturer of military and special-purpose vehicles. The company focuses on the research and development and production of highly mobile tactical vehicles, logistics support vehicles, and armored vehicles, serving the U.S. Military and the international defense market. Oshkosh Defense is renowned for its innovative engineering and durable design. Its products are widely used in battlefield transport, tactical operations, and rescue operations, while incorporating intelligent systems to enhance vehicle survivability and mission efficiency in complex environments, aiming to provide comprehensive vehicle solutions for modern military operations. |

| Product Introduction | Oshkosh Defense’s robotic combat vehicle product is its “Unmanned Tactical Vehicle” series. Combining remote control and autonomous navigation technologies, these vehicles can perform reconnaissance, transport, and support missions in complex terrain. Equipped with high-performance sensors, lidar, and autonomous driving algorithms, the vehicles achieve obstacle avoidance, path planning, and battlefield environmental awareness. The system supports remote operation and semi-automatic modes, reducing personnel exposure risk and improving operational flexibility and mission efficiency. This series is designed to provide unmanned tactical support for modern military operations, enhancing troop battlefield survivability while ensuring safety redundancy and mission reliability. |

Source: Third-party data, QYResearch Research Team

Company 2

| Pratt Miller | Description |

| Company Introduction | General Dynamics Land Systems (GDLS), a subsidiary of General Dynamics Corporation and headquartered in Michigan, is a leading global manufacturer of armored fighting vehicles. The company focuses on the research and development and production of land warfare equipment such as main battle tanks, armored personnel carriers, and armored reconnaissance vehicles, combining advanced electronic systems, fire control systems, and networked command and control technologies to enhance combat effectiveness and survivability. GDLS customers include the U.S. and international militaries, and its products are widely used in land combat and tactical support missions. GDLS also actively explores unmanned and intelligent vehicle technologies to meet the needs of modern military operations. |

| Product Introduction | GDLS’ robotic combat vehicle products include unmanned ground tactical platforms capable of performing reconnaissance, fire support, and logistical transport missions. These vehicles employ autonomous navigation systems, lidar, and sensor fusion technology to achieve real-time battlefield environment awareness and path planning. Control modes support remote operation and semi-autonomous mission execution to reduce soldier exposure risk while improving operational efficiency. This unmanned platform can integrate various weapons and mission modules, enhancing troop tactical flexibility and survivability, and represents a significant achievement for GDLS in promoting the intelligent and unmanned development of land warfare equipment. |

Source: Third-party data, QYResearch Research Team

Company 3

| Textron Systems | Description |

| Company Introduction | Israel Aerospace Industries (IAI), founded in 1953 and headquartered in Israel, is a globally renowned defense and aerospace company. Its business encompasses unmanned aerial vehicles (UAVs), missile systems, satellite technology, and robotic combat vehicles, boasting strong technological capabilities. IAI focuses on developing advanced autonomous systems, intelligent sensing and command and control technologies, providing diverse defense solutions for militaries worldwide. Its innovation capabilities are particularly evident in unmanned combat platforms, long-range reconnaissance, and autonomous combat systems, driving the development of modern, intelligent warfare equipment while providing high reliability and tactical flexibility. |

| Product Introduction | IAI’s robotic combat vehicles primarily consist of unmanned ground-based tactical platforms capable of performing reconnaissance, patrol, and fire support missions. Equipped with lidar, high-definition cameras, and advanced autonomous navigation systems, these vehicles enable obstacle avoidance and path planning in complex environments. Supporting remote operation and autonomous mission execution, they reduce personnel exposure to combat risks and improve operational efficiency and flexibility. These unmanned platforms can integrate weapon systems, sensors, and communication modules for urban warfare, border patrols, and battlefield support, representing a significant achievement of IAI in promoting the intelligentization of unmanned combat equipment. |

Source: Third-party data, QYResearch Research Team

3 Robotic Combat Platform Industry Chain Analysis

| Industry Chain | Description |

| Upstream | The upstream of robotic combat platforms mainly includes core technology R&D companies and key component suppliers. Core technologies encompass artificial intelligence decision-making algorithms, machine vision, sensor fusion, communication and navigation systems, and combat command and control software. These technologies determine the platform’s autonomous combat capability, target recognition accuracy, and tactical response speed. Key components include power systems, precision actuators, sensor modules, weapon interfaces, armor materials, and energy management equipment, providing hardware support and operational reliability for the entire platform. Furthermore, the upstream also includes simulation training systems, combat simulation software, and big data processing platforms, providing necessary data and technical support for platform R&D, testing, and tactical optimization, forming the foundational support link of the entire industry chain. |

| Midstream | The midstream segment encompasses the integrated design, system integration, and combat platform development of robotic combat platforms. System integrators efficiently integrate the artificial intelligence algorithms, sensors, weapon systems, and communication modules provided by the upstream to achieve autonomous combat, remote control, and multi-platform collaborative functions. During the integration process, midstream companies also need to conduct reliability testing, environmental adaptability testing, and combat simulations to ensure the platform operates stably under complex battlefield conditions. Meanwhile, the midstream also includes the development of command and control software and combat coordination platforms, enabling data interconnection and collaborative operations across multiple platforms and missions. This is the core link in transforming upstream technological achievements into actual combat capabilities. |

| Downstream | The downstream mainly involves the deployment, execution, and full lifecycle maintenance of robotic combat platforms. Military or security agencies are the primary users, and the platforms can be applied to various combat missions such as reconnaissance, strike, support, and defense. Downstream aspects also include platform maintenance, system upgrades, energy management, and data feedback and analysis to ensure the long-term stable and efficient operation of the platform. Combat training and tactical exercises are also key components, improving the collaboration efficiency between the platform and operators by simulating real combat environments. Furthermore, the downstream transmits combat data and user feedback back to the midstream and upstream to optimize algorithms and improve platform design, achieving a closed-loop industry chain and continuous iterative upgrades. |

Source: Third-party data, QYResearch Research Team

4 Robotic Combat Platform Industry Development Trends, Opportunities, Obstacles and Industry Barriers

Development Trends:

1. Accelerated Intelligent Autonomy: Global robotic combat platforms are evolving towards higher levels of intelligence and autonomy. AI decision-making systems, machine vision, sensor fusion, and automated mission planning are continuously being optimized, enabling platforms to independently complete reconnaissance, strike, and collaborative missions in complex battlefield environments. This reduces reliance on human operation and improves combat efficiency and reaction speed.

2. Multi-Platform Collaborative Operations: Future combat platforms are trending towards networking and collaboration, supporting simultaneous multi-platform, multi-mission operations. Unmanned ground vehicles, drones, and unmanned underwater platforms achieve information sharing and collaborative operations through a unified command and control system, improving overall combat effectiveness while reducing the operational risks associated with the destruction of a single platform.

3. Modular and Scalable Design: Robotic combat platforms adopt a modular and scalable design, allowing for rapid replacement of weapon systems, sensors, or communication modules to adapt to different tactical requirements. This flexibility not only reduces R&D costs and upgrade difficulty but also enhances the platform’s adaptability and long-term usability in diverse combat environments.

Development Opportunities:

1. Enhance battlefield efficiency and personnel safety. Robotic combat platforms can perform missions in dangerous areas, such as forward reconnaissance, fire support, and logistical transport, reducing the risk of soldier casualties. Unmanned warfare provides the military with flexible and efficient combat capabilities, representing a significant opportunity for the technological upgrade of modern warfare.

2. Drive the development of the military industry and related supply chains. The development of these platforms promotes the rapid growth of industries such as artificial intelligence, sensors, high-precision manufacturing, communication technology, and power systems. Upstream and downstream enterprises form a complete ecosystem, including component supply, system integration, software development, and maintenance services, creating new growth points for the global military industry.

3. Data value and tactical optimization. Combat platforms generate a large amount of battlefield data during mission execution, including target identification, movement trajectory, and combat effectiveness analysis. By training AI algorithms and optimizing tactical strategies with this data, not only is the platform’s combat performance improved, but a new data-driven strategic value chain is also formed.

Hindering Factors:

1. High Technological Barriers and Financial Pressure. Robotic combat platforms involve core technologies such as AI, machine vision, sensor fusion, weapon control, and power systems, resulting in long development cycles and high costs. Small and medium-sized enterprises (SMEs) and new entrants struggle to afford the massive investments, limiting market scaling and rapid deployment.

2. Inadequate Legal, Ethical, and International Standards. The use of unmanned combat platforms involves controversies related to international law, the law of war, and ethics, such as liability determination, civilian harm risks, and the ethical boundaries of autonomous weapons. The lack of globally unified regulations and standards may limit platform deployment and export market expansion.

3. Challenges in Adapting to Complex Environments. The reliability of platforms in complex terrain, extreme weather, or communication-constrained conditions remains a challenge. Perception errors, system delays, or malfunctions can affect mission execution, reduce operational efficiency, and increase the uncertainty and risk of military operations.

Barriers:

1. Core Technology Barriers: AI-powered autonomous decision-making, sensor fusion, tactical control algorithms, and communication command systems are the core technologies of the platform. Companies mastering these technologies can maintain a competitive advantage in the long term, making it difficult for new entrants to break through in the short term, thus creating high barriers to entry.

2. Data and Combat Experience Barriers: Robotic combat platforms require a large amount of real-world or simulated training data to optimize algorithms. Companies with abundant data and combat experience can continuously improve the intelligence level of their platforms, forming a strong data barrier that is difficult for new entrants to replicate.

3. Industry Ecosystem and Customer Barriers: Leading companies typically build a complete upstream and downstream ecosystem, including component suppliers, system integrators, maintenance services, and military partnerships. This complete ecosystem and long-term customer bonds create significant barriers for new entrants in terms of market access, resources, and customer acquisition.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading Global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are Globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 18 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp