QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Hedione- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Hedione market, including market size, share, demand, industry development status, and forecasts for the next few years.

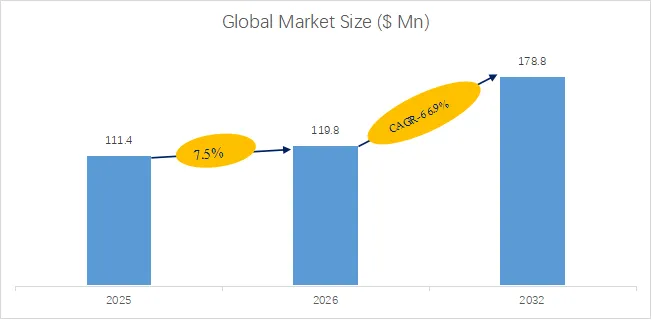

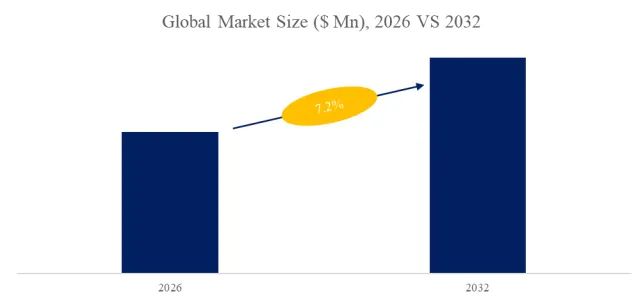

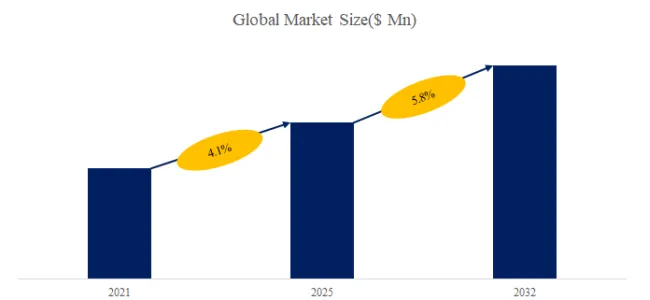

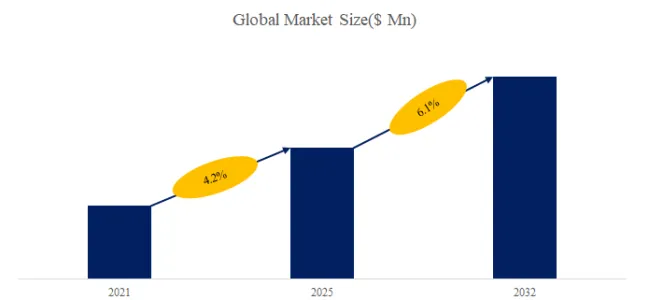

The global market for Hedione was estimated to be worth US$ 199 million in 2025 and is projected to reach US$ 276 million, growing at a CAGR of 4.8% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6263331/hedione

Product Definition and Market Size

Hedione (Methyl dihydrojasmonate) is an exceptionally important synthetic fragrance material, appearing as a colorless to pale yellow liquid. It possesses a fresh, elegant, and long-lasting scent characterized by notes of jasmine and citrus. Primarily utilized in high-end perfumes, cosmetics, and personal care products, it serves as a core ingredient in many renowned fragrances and is frequently employed to recreate the sensation of natural floral scents.

According to QYResearch Chemical and Materials Research Center, the global Hedione market will reach US$ 276 million by the end of 2032, growing at a CAGR of 4.8% during 2026-2032.

Figure00001. Global Hedione Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch Chemical and Materials Research Center. If you need the latest data, plaese contact QYResearch.

Industry Chain Overview

The upstream segment relies primarily on basic raw materials derived from the petrochemical industry; the core synthesis pathways typically utilize cyclopentanone, valeraldehyde, or adipic acid as starting materials. Through the application of sophisticated catalytic techniques—involving a series of complex reactions such as condensation, addition, and esterification—a molecular backbone possessing a jasmine-like aroma is constructed. Furthermore, with the rise of green chemistry, several leading enterprises have begun exploring bio-based raw materials in an effort to reduce the carbon footprint associated with their production processes.

In the midstream segment, Methyl Dihydrojasmonate stands out as a fragrance ingredient subject to rigorous requirements regarding isomer ratios, olfactory purity, color stability, and batch-to-batch consistency. The core competitive advantage in this sector lies in the precise control of isomer ratios. The aromatic quality of Methyl Dihydrojasmonate is highly contingent upon the content of its “cis” isomer; products with a high cis-isomer content (such as Hedione HC) can exhibit an aromatic intensity several times greater than that of standard grades.

In the downstream segment, Methyl Dihydrojasmonate imparts a transparent, elegant white-floral jasmine aroma accented by a fresh citrus nuance. It is frequently employed in perfumery to enhance the floral presence, diffusion, and luminosity of a fragrance; at the consumer end, demand is highly concentrated within the broader flavors and fragrances industry.

Competitive Landscape

According to QYResearch, the global market for methyl dihydrojasmonate exhibits an oligopolistic competitive landscape. The market is highly concentrated among a select few international fragrance giants—who possess core manufacturing processes—and a rapidly emerging group of Chinese fine chemical enterprises. Key market participants include Wanxiang Technology, dsm-firmenich, NHU, Kao, and IFF; notably, the top three manufacturers collectively account for approximately 60% of the total market share. Leveraging their first-mover advantages in synthesis processes, patent protection, and global sales networks, these companies have long dominated the market—with firms such as Firmenich, in particular, possessing deep technical expertise in high-end product lines, such as high cis-methyl dihydrojasmonate.

The companies listed below are key players driving global market growth with their innovative solutions and extensive product portfolios.

1. Wanxiang Technology

Headquarters: Jiangsu, China

Main Business: Established in 2001, Wanxiang Technology Group is a leading fragrance and flavor enterprise headquartered in Huai’an, Jiangsu. The company specializes in the R&D, production, and sales of both synthetic and natural aromatic ingredients. Its key products—including Methyl Dihydrojasmonate and Amberone—are widely utilized in the daily chemical, food, and beverage industries, serving a global clientele that includes international leaders such as Givaudan and Firmenich.

2. dsm-firmenich

Headquarters: Maastricht, the Netherlands, and Kaiseraugst, Switzerland

Main Business: dsm-firmenich is a global, science-driven company formed in 2023 through the merger of DSM—a Dutch nutrition and health enterprise—and Firmenich—a Swiss giant in the fragrance and flavor industry. The company focuses on the fields of nutrition, health, and beauty, leveraging biotechnology and natural ingredients. Its operations span fragrances, food textures, animal nutrition, and health care, positioning it as a world leader in healthy living and sustainability.

3. Kao

Headquarters: Tokyo, Japan

Main Business: Founded in Japan in 1887, Kao is a global giant in daily-use chemicals and health care products with a history spanning over 130 years. Headquartered in Tokyo, the company’s business encompasses beauty care, health care, fabric and home cleaning products, chemical products, and other related fields.

4. NHU

Headquarters: Zhejiang, China

Main Business: Established in 1999 and listed on the Shenzhen Stock Exchange in 2004, NHU is a world-leading manufacturer of vitamins, fragrances and flavors, and new polymer materials. The company focuses on the sectors of nutrition and health, daily chemical care, transportation, and environmental protection. It operates four modern production bases and is recognized as one of China’s top 100 fine chemical enterprises.

Market Drivers, Challenges, Prospects

Market Drivers:

The continuous expansion of the downstream high-end perfume and niche fragrance sectors serves as the primary demand driver for Methyl Dihydrojasmonate (MDJ). Fundamentally, MDJ is a classic floral-diffusing ingredient within the flavor and fragrance industry. In modern perfume formulations, its inclusion levels typically range from 5% to 35%; it blends seamlessly with a wide array of floral, citrus, and woody notes, thereby enhancing the overall spatial diffusion and transparency of the fragrance. The industry’s growth directly benefits from the expansion of the global perfume market—particularly within the high-end, niche, and fashion fragrance segments.

In contrast to the potential allergenic components found in natural jasmine absolute, synthetic MDJ boasts exceptional chemical purity and extremely low allergenic potential. Against the backdrop of increasingly stringent global cosmetic regulations—such as the IFRA standards in the EU—fragrance brands are increasingly favoring the use of synthetic monomers, which offer superior safety profiles and greater batch-to-batch consistency.

Challenges:

Customers place stringent demands on batch-to-batch stability, isomer control, and olfactory consistency, thereby establishing a significant technical barrier. The isomer ratio, purity, and olfactory consistency of methyl dihydrojasmonate directly impact the end-use experience. For fragrance clients, raw materials of this nature typically necessitate long-term sample retention, consistency tracking, and application validation. Consequently, the industry barrier lies not merely in the successful synthesis of the compound, but—more critically—in the ability to consistently and reliably deliver reproducible and verifiable olfactory performance over the long term.

Prospects:

Standard methyl dihydrojasmonate and high-cis methyl dihydrojasmonate exhibit distinct differences in terms of intensity and application positioning. Consequently, the future focus of industry competition is expected to gradually shift away from the mere supply of standard commodities toward high-performance, high-cis variants; bio-based versions; and differentiated products characterized by superior purity and stability. Overall, this compound is therefore poised to remain a classic aromatic raw material within the flavors and fragrances industry—one characterized by a long product lifecycle and stable demand, yet increasingly defined by an emphasis on quality enhancement and product differentiation.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Hedione market is segmented as below:

By Company

dsm-firmenich

Takasago

ZEON

Kao

IFF

Bedoukian Research

Zhejiang NHU

Wanxiang Technology

Segment by Type

Purity 95%-98%

Purity ≥98%

Other

Segment by Application

Perfume

Daily Chemicals

Food

Other

Each chapter of the report provides detailed information for readers to further understand the Hedione market:

Chapter 1: Introduces the report scope of the Hedione report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Hedione manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Hedione market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Hedione in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Hedione in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Hedione competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Hedione comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Hedione market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Hedione Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Hedione Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Hedione Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp