QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Button Mushroom Products- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Button Mushroom Products market, including market size, share, demand, industry development status, and forecasts for the next few years.

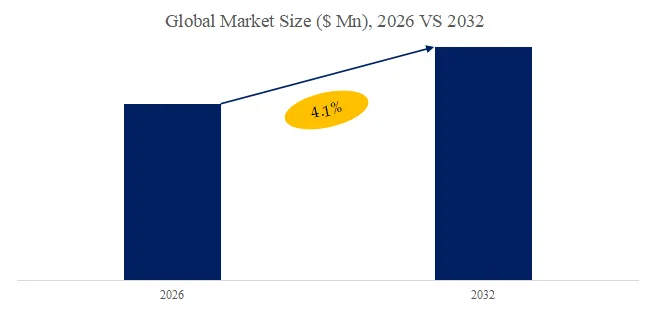

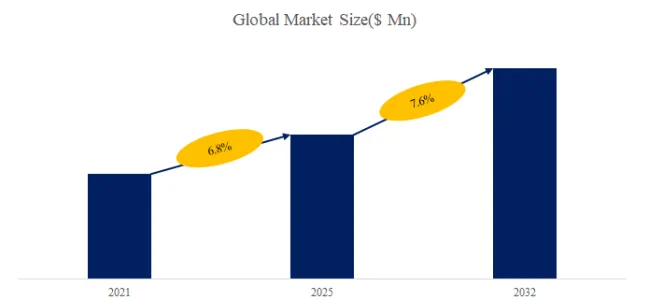

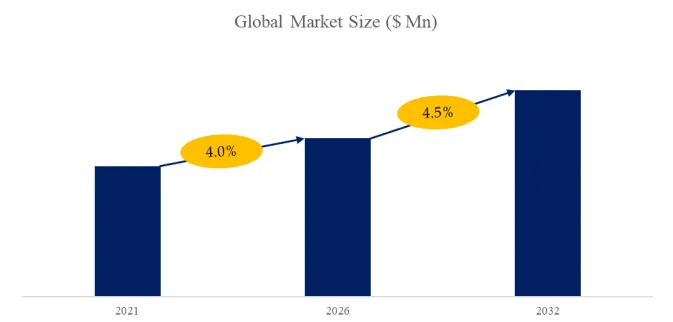

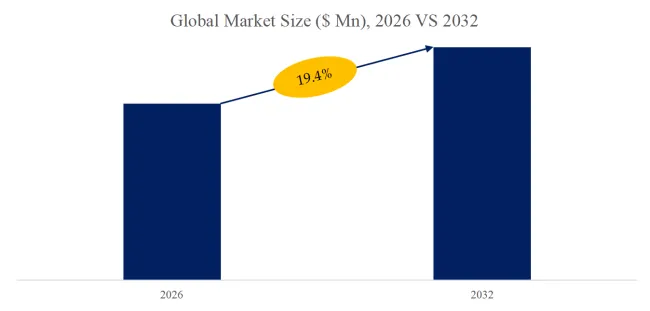

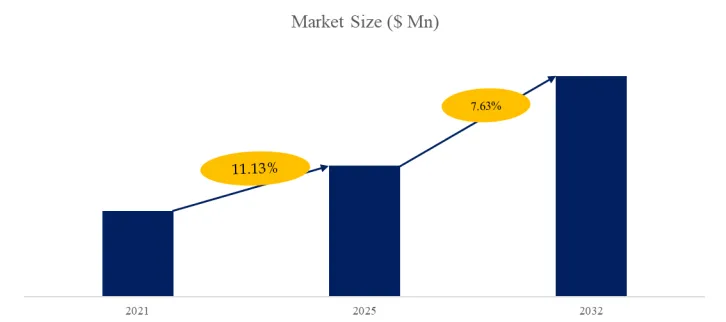

The global market for Button Mushroom Products was estimated to be worth US$ 18000 million in 2025 and is projected to reach US$ 30363 million, growing at a CAGR of 7.6% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6634699/button-mushroom-products

Button Mushroom Products Market Summary

Definition and Scope

Button mushroom products refer to various processed mushroom products made from Agaricus bisporus, the most widely cultivated and consumed mushroom variety globally. The product range includes fresh market products for direct consumers, primary processed products, and deeply processed products used as food industry ingredients.

From a product form perspective, button mushroom products can be classified by processing depth. Fresh button mushrooms are the most basic form, sold through fresh produce channels. Canned button mushrooms represent one of the oldest and most industrialized processing categories. Frozen button mushrooms preserve freshness and nutritional content through rapid freezing technology. Dried button mushrooms include hot-air dried, freeze-dried, and sun-dried products. Pickled button mushrooms are produced through traditional processing methods in certain regions. Additionally, deeply processed products continue to expand, including mushroom seasonings and sauces, ready-to-eat snack products, mushroom extracts and dietary supplements, and mushroom protein and functional polysaccharides as novel food ingredients.

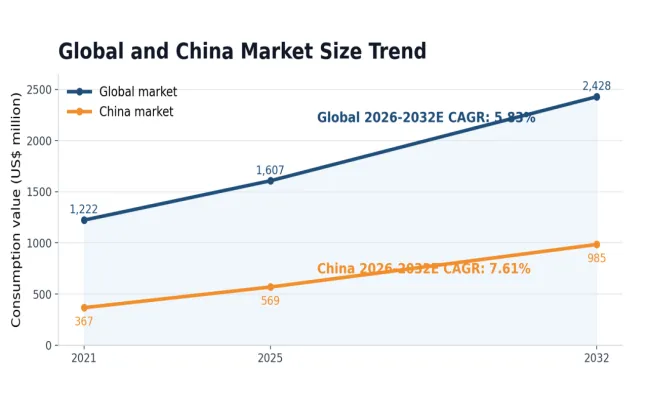

Figure00001. Global Button Mushroom Products Market Size (US$ Million), 2021-2032

Above data is based on report from QYResearch: Global Button Mushroom Products Market Report 2022-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

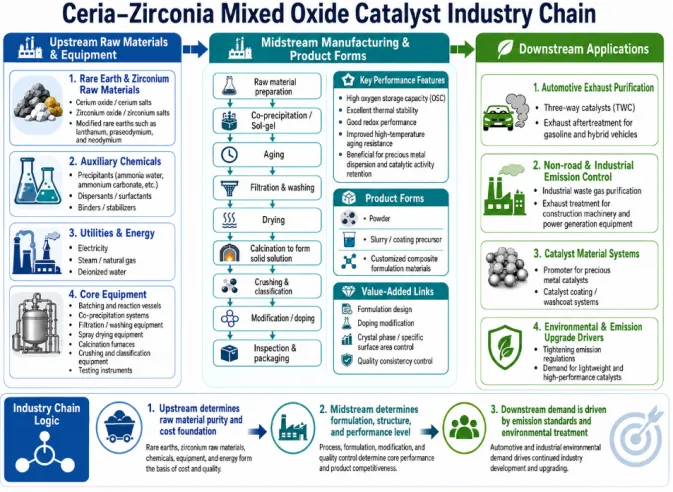

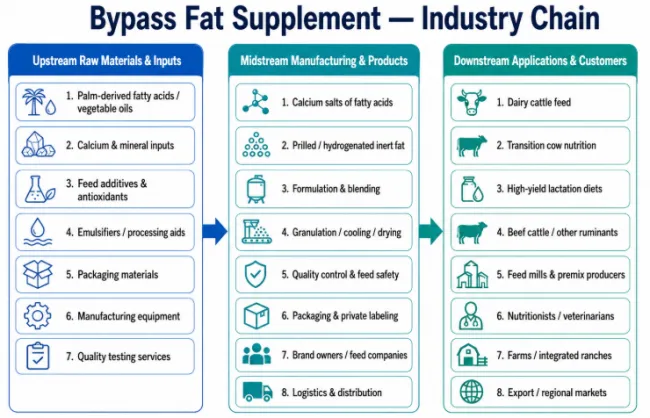

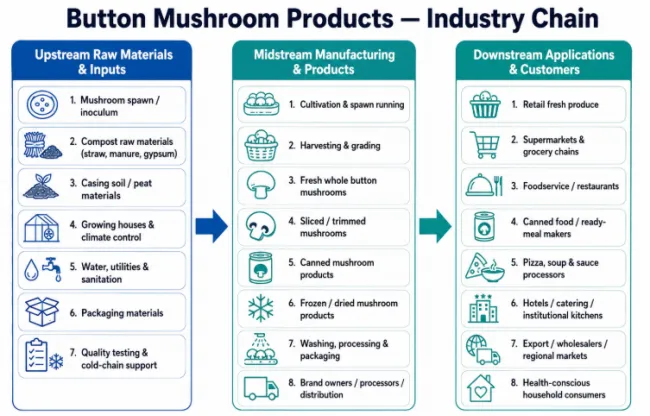

Industry Chain Analysis

Upstream segment: spawn research and development and substrate material suppliers.

The upstream segment includes spawn breeding and propagation enterprises, along with suppliers of raw materials for substrate production. Spawn genetic quality directly determines cultivation yield, fruiting uniformity, disease resistance, and commercial traits. Substrate raw materials include wheat straw, chicken manure, gypsum, calcium carbonate, and various nutritional additives. Large-scale industrial mushroom cultivation enterprises typically operate their own substrate fermentation facilities.

Midstream segment: mushroom cultivation, harvesting, and primary processing.

The midstream segment encompasses the entire production process from substrate inoculation, spawn running, casing, fruiting management to harvesting and post-harvest handling. Participants include traditional small-scale growers, specialized grower cooperatives, and industrial-scale year-round production facilities. Post-harvest handling capacity is a critical indicator of technical capability, as harvested mushrooms must enter pre-cooling quickly to prevent opening, browning, and moisture loss.

Downstream segment: food processing enterprises, food service operators, and retail channels.

The downstream segment includes food processing enterprises as major buyers of processed mushroom products, food service operators as important customers for fresh and primary processed products, and retail channels covering traditional fresh produce markets, supermarkets, e-commerce platforms, and community fresh food stores.

Value distribution and future trends.

Midstream large-scale enterprises with superior spawn resources and industrial cultivation technology hold core industry positions. Future trends include continued substitution of traditional cultivation with industrial farming, product category expansion and value addition through deep processing, brand building extending from processed to fresh products, and evolving global trade flows driven by emerging market demand growth.

Figure00002. Button Mushroom Products Industrial Chain

Above data is based on report from QYResearch: Global Button Mushroom Products Market Report 2022-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

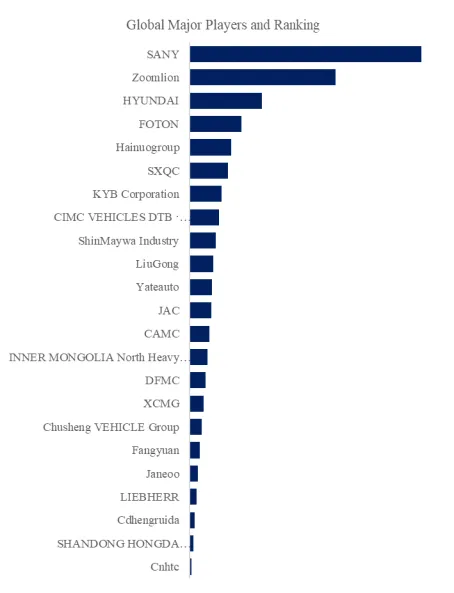

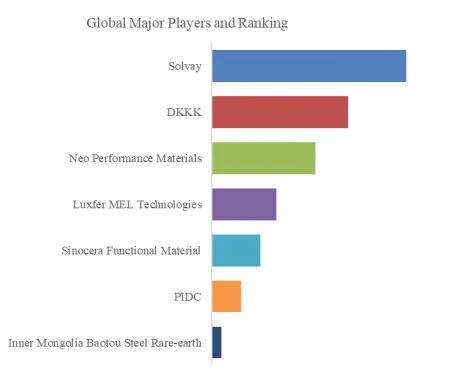

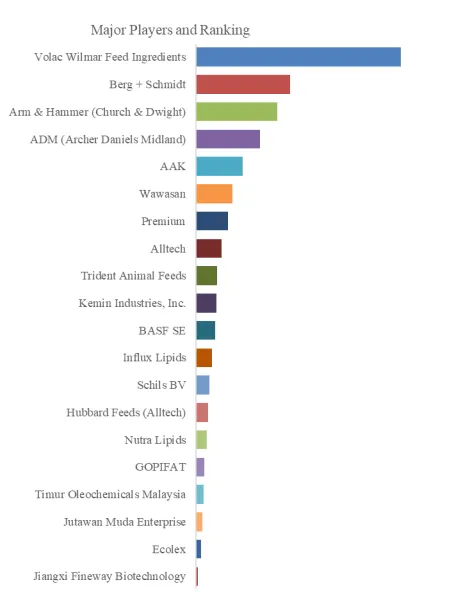

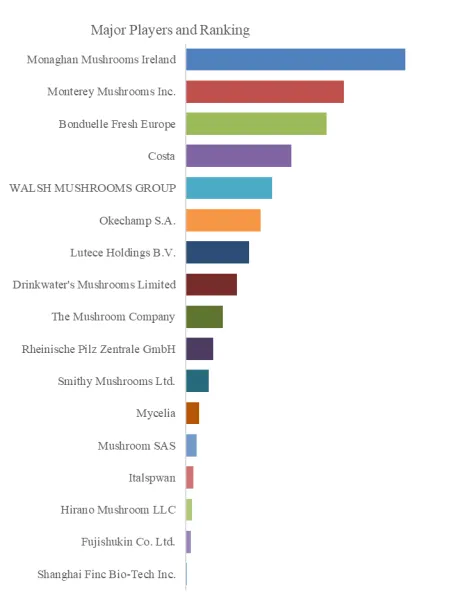

Figure00003. Global Button Mushroom Products Top 17 Players Ranking and Market Share (Ranking is based on the revenue of 2025, continually updated)

Above data is based on report from QYResearch: Global Button Mushroom Products Market Report 2025-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

Overall Industry Development Overview

The global button mushroom products market is in a mature stage of steady growth. Button mushroom is currently the edible mushroom species with the highest global output and widest consumption coverage, occupying a core position in the edible mushroom industry. The stable expansion of this market is jointly driven by multiple factors: consumers’ continuously increasing focus on healthy diets, the plant-based food trend’s attention to mushroom protein and flavor substances, stable demand from the food processing industry for standardized button mushroom raw materials, and consumption upgrading brought by the expansion of the middle class in emerging markets.

From the perspective of industry development stage, the supply side of button mushroom products is undergoing a structural transition from traditional greenhouse cultivation to industrialized year-round production. In developed markets such as Europe and North America, industrialized cultivation has already become dominant, and the high standardization and automation of the production process have significantly improved product quality stability and food safety assurance. In Asia-Pacific and other emerging market regions, traditional greenhouse cultivation still accounts for a considerable proportion, but investment in industrialized projects is accelerating. This structural transformation has not only changed the supply pattern of button mushroom products, but also created new requirements for supporting industries such as strain breeding, substrate production, and post-harvest handling.

From the perspective of regional structure, the global button mushroom products market features both concentrated production areas and dispersed consumption markets. China is the world’s largest button mushroom producer and accounts for a considerable share of global output. Europe’s major producing countries include the Netherlands, France, and Poland, with the Netherlands holding a global leading position in industrialized cultivation technology and breeding research. The North American market is led by the United States, where fresh button mushroom products account for the main share of edible mushroom consumption. On the consumption side, North America, Europe, and Asia-Pacific are the main consumer markets for button mushroom products. Among them, per capita consumption of button mushrooms in Asia-Pacific still has considerable room for growth, indicating significant market potential.

Key Development Characteristics

Characteristic 1: The structural replacement of traditional greenhouse cultivation by industrialized cultivation continues to deepen.

Industrialized button mushroom cultivation uses computer control systems to simulate and optimize the environmental conditions required for mushroom growth, enabling continuous and stable production regardless of season and climate. Compared with traditional greenhouse cultivation, this production model has clear advantages in yield per unit area, product quality consistency, food safety assurance, and resource utilization efficiency. In mature European and North American markets, industrialized cultivation already accounts for the vast majority of button mushroom output. In emerging markets such as Asia-Pacific, industrialized capacity is also expanding rapidly. This structural replacement trend has had a profound impact on the competitive landscape of the button mushroom industry. Industrialized enterprises have established strong competitive advantages in both fresh product markets and deeply processed raw material markets by relying on stable supply capability and controllable product quality. Traditional greenhouse growers are gradually shifting toward differentiated directions such as high-quality specialty products or localized small-scale supply.

Characteristic 2: Branding and origin-based differentiation of fresh products are becoming increasingly evident.

As consumers pay greater attention to the quality of edible mushroom products, fresh button mushrooms are shifting from undifferentiated bulk commodities to differentiated products with brand attributes. Brand-oriented operations help consumers form quality trust and purchase preference among many choices by establishing unified product grading standards, quality traceability systems, and corporate visual identity systems. Origin labeling has also become an important part of branding. The flavor characteristics formed by specific production areas through unique climate conditions, cultivation substrates, and processing traditions are being developed into differentiated selling points. Some high-end fresh button mushroom products have begun emphasizing sustainable cultivation methods, traceable supply chains, product freshness, and quantified taste indicators.

Characteristic 3: Innovation in ready-to-eat and convenient button mushroom products is accelerating category expansion.

The consumption scenarios of traditional button mushroom products were mainly limited to home cooking and catering side dishes, with fresh products, canned products, and frozen products as the main forms. In recent years, with faster-paced lifestyles and more diverse consumption scenarios, innovation in ready-to-eat button mushroom snacks has accelerated significantly. Sliced, dried, and seasoned button mushroom chips have entered the snack market with their crispy texture and portable packaging. Pre-prepared and frozen button mushroom meal packs provide convenient solutions for home cooking and group meal services. Bottled or pouched seasoned button mushroom sauces expand the application boundaries of button mushrooms in the condiment sector. This diversification of product forms expands the consumption scenarios of button mushroom products and attracts more attention from younger consumer groups.

Characteristic 4: Extraction and utilization of functional components are pushing the industry toward higher added value.

Button mushrooms are rich in dietary fiber, fungal polysaccharides, ergosterol, and various trace elements. The health value of these functional components is receiving increasing attention. Button mushroom polysaccharides are considered potential immune modulators and have application prospects in functional foods and dietary supplements. Ergosterol in button mushrooms can be converted into vitamin D2 after ultraviolet irradiation, making button mushrooms a good raw material for natural vitamin D fortified foods. Some leading enterprises have started to use extraction and purification of functional components from button mushrooms as a direction for business expansion, developing high-value-added products such as button mushroom polysaccharide capsules, button mushroom protein powder, and vitamin D fortified button mushroom powder. This development trend is pushing the button mushroom industry from traditional food processing toward functional ingredients and dietary supplements.

5. Favorable Factors for Industry Development

Favorable factor 1: The global healthy eating trend drives growth in consumption of button mushroom products.

Button mushrooms have nutritional characteristics such as high protein, low fat, and low calories. They are rich in dietary fiber, B vitamins, selenium, potassium, and other minerals. Their nutritional value and health attributes are highly aligned with contemporary consumers’ pursuit of healthy diets. As consumers pay increasing attention to ingredient labels on processed foods, button mushrooms are being re-recognized as natural ingredients and clean-label raw materials in the food industry. In the plant-based food wave, the umami flavor and meat-like texture of button mushrooms make them ideal raw materials for the development of meat substitutes. Several multinational food companies have launched plant-based burger patties and minced meat products using button mushrooms as a main ingredient.

Favorable factor 2: Stable demand from the food processing industry for standardized button mushroom raw materials supports growth in the processed products market.

Canned and frozen button mushroom products are important raw materials in the food processing industry. The use of standardized, ready-to-use button mushroom ingredients continues to increase in industrialized food categories such as pizza, prepackaged salads, soups, and ready-to-eat meal boxes. The strict requirements of restaurant chains for ingredient specifications, quality, and safety during menu standardization further promote procurement demand for sorted and preprocessed button mushroom products with uniform specifications. This stable demand from the food processing and catering industries provides continuous growth momentum for the button mushroom processed products market.

Favorable factor 3: Mature industrialized cultivation technology reduces production costs and improves supply stability.

The promotion of industrialized cultivation technology allows button mushroom production to overcome climate and seasonal restrictions, achieving stable and balanced year-round supply. The highly controllable production environment significantly improves yield per unit area and the proportion of premium-quality mushrooms, while both fixed and variable costs per unit of product show a downward trend. Lower production costs strengthen the price competitiveness of button mushroom products in the market and provide a more economical raw material source for large-scale production of processed and deeply processed products. Improved supply stability also enhances the procurement confidence of downstream food processing enterprises and catering customers.

Favorable factor 4: Consumption upgrading driven by the expanding middle class in emerging markets provides long-term growth space.

Economic growth and the continued expansion of middle-class groups in emerging markets are driving upgrades in food consumption structures. In regions such as Asia-Pacific, Latin America, and the Middle East, rising per capita income and faster lifestyles have significantly increased consumers’ acceptance and purchase frequency of edible mushroom products. In these markets, button mushrooms, as ingredients with high nutritional value and diverse cooking methods, are shifting from occasionally consumed premium ingredients to common categories in daily diets. Growth potential in per capita consumption provides long-term demand support for the expansion of the global button mushroom products market.

Unfavorable Factors for Industry Development

Unfavorable factor 1: Post-harvest preservation and distribution losses of fresh button mushrooms constrain profitability.

After harvest, button mushrooms have active respiration and lose moisture quickly. Under normal temperature conditions, cap opening and browning progress rapidly. Fresh products require full cold-chain distribution, and temperature and humidity must be strictly controlled in every stage from harvest pre-cooling and refrigerated transportation to end-shelf display. Even with a well-developed cold chain, the shelf life of fresh button mushrooms remains relatively short. Producers must arrange harvesting and shipment volumes based on accurate sales forecasts. Distribution losses, including weight reduction caused by moisture loss, mechanical damage during transportation, and returns of unsold products after shelf-life expiration, account for a considerable proportion of the total cost of fresh products and directly affect the profitability of fresh button mushroom operations.

Unfavorable factor 2: Traditional greenhouse cultivation faces dual pressure from environmental regulations and rising labor costs.

As industrialized cultivation accelerates, the operating environment for traditional greenhouse growers is becoming tighter. Environmental regulations impose higher requirements on agricultural waste treatment and cultivation substrate disposal, increasing compliance costs for small-scale growers. The continued outflow of rural labor and annual increases in minimum wage standards place significant labor cost pressure on the labor-intensive greenhouse cultivation model. In response to these challenges, traditional greenhouse growers either integrate resources through cooperative models to improve standardization or shift toward differentiated competitive strategies such as high-value specialty products or local direct sales.

Unfavorable factor 3: Tariff barriers and quarantine restrictions in international trade affect market circulation.

International trade in button mushroom products is significantly affected by importing countries’ quarantine regulations and tariff policies. Tariff levels for processed products such as canned button mushrooms vary across countries, and tariff fluctuations directly affect export competitiveness and import costs. In terms of quarantine, fresh button mushrooms, as fresh agricultural products, face stricter entry inspection requirements. Some countries impose import restrictions on fresh mushroom products from specific production areas. These trade barriers increase uncertainty in export operations and make processed products more resilient than fresh products in international trade.

Unfavorable factor 4: Consumer perception and competition from seasonal substitute products divert part of demand.

In some consumer markets, consumers lack a clear understanding of the nutritional differences and cooking characteristics between button mushrooms and other common edible mushroom varieties such as shiitake and oyster mushrooms. Button mushrooms are often viewed as general-purpose ingredients that can be easily replaced by other edible mushrooms. This unclear perception causes button mushrooms to face demand diversion pressure from lower-priced or locally distinctive edible mushroom varieties at retail terminals. At the same time, in specific seasons, the large-scale availability of fresh seasonal vegetables also partially substitutes button mushrooms on household dining tables.

Entry Barriers

Barrier 1: Investment threshold and operational management barriers of industrialized cultivation.

Building a modern industrialized button mushroom cultivation facility requires substantial upfront capital investment. Temperature and humidity control systems, ventilation systems, lighting systems, and cultivation rack systems in mushroom rooms require relatively high equipment investment. Construction of substrate fermentation tunnels is also costly. In addition to hardware investment, industrialized cultivation requires professional operational management capabilities, including optimization of substrate formulas, precise control of environmental parameters, integrated pest and disease management, and accurate determination of harvesting timing. These operational management capabilities need to be accumulated through long-term production practice and represent a high technical threshold for new entrants without an edible mushroom cultivation background.

Barrier 2: Technical and intellectual property barriers in strain breeding.

Superior button mushroom strains are the prerequisite for high-yield and high-quality products. Strain breeding involves multiple technical steps, including wild collection, spore isolation, single-spore hybridization, and molecular marker-assisted selection. The research and development cycle is long and requires considerable investment. Leading strain breeding institutions protect their core assets through patented strains and trade secrets, making it difficult for new entrants to obtain commercially competitive superior strains in a short period of time. In countries and regions where the button mushroom industry is relatively developed, the strain supply segment has already formed a high level of industry concentration. New entrants have limited options for strain sources and need to pay licensing fees to strain suppliers.

Barrier 3: Market barriers in fresh product channel development and brand building.

Fresh button mushroom sales channels mainly include fresh food supermarkets, wet markets, and catering supply chains, all of which have relatively high entry thresholds. The supplier admission process of large chain supermarkets includes comprehensive evaluation of product quality, supply capability, food safety management systems, and price competitiveness. New entrants often need to go through a long assessment period before gaining access. Catering supply chain customers prefer to establish long-term partnerships with large suppliers that can provide stable sources and uniform product specifications. In terms of brand building, fresh button mushroom products require continuous brand investment and market promotion to establish differentiated brand recognition in consumers’ minds. This is a major challenge for new entrants with limited resources.

Barrier 4: Food safety and quality consistency control barriers for processed products.

Button mushroom processed products, especially canned and frozen products, belong to food categories with relatively high food safety risks. Producers need to establish and maintain food safety management system certifications and quality management system certifications. Strict quality control is required in every step from raw material acceptance and processing control to finished product inspection. Consistency in product quality across batches is one of the core demands of downstream customers. This requires enterprises to establish standardized operating procedures in raw material grading, process parameter setting, online inspection, and other stages. The potential risk of food safety incidents and the need to protect corporate quality reputation together form high entry barriers in the processed products market.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Button Mushroom Products market is segmented as below:

By Company

Bonduelle Fresh Europe

Costa

Drinkwater’s Mushrooms Limited

Lutece Holdings B.V.

Monaghan Mushrooms Ireland

Monterey Mushrooms Inc.

Okechamp S.A.

The Mushroom Company

WALSH MUSHROOMS GROUP

Mycelia

Smithy Mushrooms Ltd.

Rheinische Pilz Zentrale GmbH

Italspwan

Mushroom SAS

Hirano Mushroom LLC

Fujishukin Co. Ltd.

Shanghai Finc Bio-Tech Inc.

Segment by Type

White Button Mushroom

Brown Button Mushroom (Crimini/Baby Bella)

Portobello Mushroom (Mature)

Segment by Application

Supermarkets & Hypermarkets

Specialty Grocery / Health Food Stores

Food Service Distributors

Online Retail / E-commerce

Industrial B2B Direct

Each chapter of the report provides detailed information for readers to further understand the Button Mushroom Products market:

Chapter 1: Introduces the report scope of the Button Mushroom Products report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Button Mushroom Products manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Button Mushroom Products market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Button Mushroom Products in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Button Mushroom Products in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Button Mushroom Products competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Button Mushroom Products comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Button Mushroom Products market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Button Mushroom Products Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Button Mushroom Products Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Button Mushroom Products Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp