Global Leading Market Research Publisher QYResearch announces the release of its latest report “Smart Ultra-thin TV – Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2021-2025) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Smart Ultra-thin TV market, including market size, share, demand, industry development status, and forecasts for the next few years.

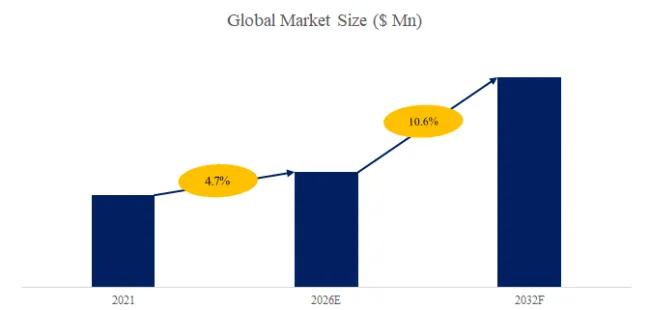

The global market for Smart Ultra-thin TV was estimated to be worth US$ 3763 million in 2025 and is projected to reach US$ 6199 million, growing at a CAGR of 7.5% from 2026 to 2032.

In 2024, global Smart Ultra-thin TV production reached approximately 1.94 million units , with an average global market price of around US$ 1800 per unit. Smart Ultra-thin TV can be defined as an ultra-thin television set equipped with internet connectivity and a built-in operating system, which allows users to stream online content, browse the web, and access various apps and services directly on the screen.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6097226/smart-ultra-thin-tv

1. Industry Pain Points and the Shift Toward Smart Ultra-thin Televisions

Traditional televisions were bulky, required external streaming devices (Roku, Apple TV, Fire Stick), and offered limited connectivity. Smart ultra-thin TVs address these limitations by combining ultra-slim form factors (often <10mm thickness) with internet connectivity and built-in operating systems (webOS, Tizen, Google TV, Roku TV). Users can stream Netflix, YouTube, Disney+, and other services directly on the screen without external devices, browse the web, and access thousands of apps. For consumers, the value proposition is clear: a sleek, wall-mountable display that serves as the central hub for all home entertainment. For manufacturers, ultra-thin design has become a key differentiator in the premium TV market.

2. Market Size, Production Volume, and Growth Trajectory (2024–2032)

According to QYResearch, the global smart ultra-thin TV market was valued at US$ 3.763 billion in 2025 and is projected to reach US$ 6.199 billion by 2032, growing at a CAGR of 7.5%. In 2024, global production reached approximately 1.94 million units with an average selling price of US$ 1,800 per unit. Market growth is driven by three factors: consumer preference for wall-mountable, space-saving designs; increasing adoption of 4K and 8K content requiring high-resolution displays; and replacement cycles (smart TVs replaced every 5–7 years vs. 8–10 years for older models).

3. Six-Month Industry Update (October 2025–March 2026)

Recent market intelligence reveals four notable developments:

- OLED vs. QLED competition: LG (OLED) and Samsung (QLED) continue to dominate the ultra-thin premium segment. OLED offers perfect blacks and thinner panels (<4mm); QLED offers higher brightness and no burn-in risk. Both segments grew 10–12% in 2025.

- 8K adoption slow but steady: 8K ultra-thin TVs (Samsung, Sony, LG, TCL) remain niche (5% of market) due to limited native 8K content, but prices have dropped from US$ 5,000+ to US$ 2,500–4,000. 8K segment grew 25% year-over-year.

- Mini-LED backlight expansion: TCL, Hisense, and Sony launched ultra-thin TVs with Mini-LED backlighting (thousands of small LEDs vs. hundreds in standard FALD), offering OLED-like contrast at lower cost. Mini-LED segment grew 40% in 2025.

- Chinese brand share gain: TCL and Hisense increased combined market share in North America and Europe from 15% to 22% in 2025, offering competitive ultra-thin models at 20–30% below Samsung/LG pricing.

4. Competitive Landscape and Key Suppliers

The market includes Korean, Japanese, Chinese, and American brands:

- LG (South Korea): Leader in OLED ultra-thin TVs (wallpaper-thin panels <4mm).

- Panasonic (Japan), Samsung (South Korea – leader in QLED ultra-thin), Sceptre (US), Seiki (US), Sharp (Japan), Sony (Japan – premium OLED and LED), TCL (China – fastest-growing), Upstar (US), Vizio (US – value leader), Hisense (China), Hair (China – Haier group), Philips (Netherlands – TP Vision), Toshiba (Japan – now Hisense).

Competition centers on three axes: panel technology (OLED vs. QLED vs. Mini-LED vs. standard LED), thickness (mm at thinnest point), and smart OS (webOS, Tizen, Google TV, Roku TV).

5. Segment-by-Segment Analysis: Size and Application

By Screen Size

- Above 40 Inch: Entry-level ultra-thin. Declining share as consumers prefer larger screens.

- 40–50 Inch: Budget segment. Account for ~15% of units, ~10% of value.

- 50–60 Inch: Mid-range sweet spot. Most popular size for residential living rooms. Account for ~35% of units, ~30% of value.

- 60–70 Inch: Premium segment. Fastest-growing (CAGR 10.0%). Account for ~30% of units, ~35% of value. Large-screen content (sports, movies) driving demand.

- Above 70 Inch: High-end segment. 75″, 85″, 98″ models. Account for ~15% of units, ~25% of value. Ultra-thin design more challenging at large sizes.

By Application

- Residential: Largest segment (~85% of market). Living rooms, home theaters, bedrooms. Preference for 55–75 inch sizes, premium picture quality.

- Commercial: (~15% of market). Hotels, conference rooms, digital signage, restaurants. Preference for larger sizes (65–85 inch), durability, and commercial-grade features (anti-burn-in, longer warranty).

User case – Residential wall-mounted installation: A homeowner replaced a 55″ traditional TV (thickness 50mm) with a 65″ LG OLED ultra-thin TV (thickness 5mm). The ultra-thin profile allowed the TV to sit flush against the wall (5mm gap vs. 50mm), creating a “picture frame” aesthetic. The homeowner also eliminated an external streaming stick (built-in webOS).

6. Exclusive Insight: Manufacturing – Ultra-Thin Panel Engineering Challenges

Achieving ultra-thin profiles (<10mm) requires significant engineering innovation:

Thickness Reduction Techniques:

| Component | Traditional TV | Ultra-thin TV | Engineering Solution |

|---|---|---|---|

| Panel | 5–8mm | 2–4mm | OLED self-emissive (no backlight) or edge-LED |

| Backlight | 10–20mm (FALD) | 2–5mm | Edge-LED or Mini-LED with thin light guide plate |

| Chassis | 10–15mm (stamped steel) | 3–6mm (extruded aluminum) | Structural aluminum, carbon fiber reinforcements |

| Electronics | Single large PCB | Multiple small PCBs + flexible circuits | Distributed board design, flex cables |

Technical challenge: Heat dissipation in ultra-thin chassis. Traditional TVs use backside vents and convection cooling; ultra-thin TVs have minimal air gap. Solutions include:

- Heat-spreading graphite sheets (Samsung, LG)

- Aluminum chassis as heat sink (Sony, TCL)

- Active cooling (micro-fans) in thicker base modules (where electronics housed)

User case – Heat management comparison: A teardown analysis of 65″ ultra-thin TVs found that LG OLED (5mm thick) uses a graphite heat spreader across the entire rear panel, maintaining surface temperature below 45°C at maximum brightness. Samsung QLED (7mm thick) uses aluminum chassis with fins, achieving 48°C. Budget ultra-thin TVs (TCL, Hisense at 9mm) with no active cooling reached 55–60°C, causing accelerated LED degradation and shorter lifespan.

7. Regional Outlook and Strategic Recommendations

- Asia-Pacific: Largest market (45% share). China (TCL, Hisense, Hair), Japan (Sony, Panasonic, Sharp), South Korea (Samsung, LG). Fastest-growing region (CAGR 8.5%). Premium segment strong in urban centers.

- North America: Second-largest (30% share). US (Vizio, TCL, Samsung, LG, Sony). Strong demand for 65–85 inch models. Value segment (Vizio, TCL) strong.

- Europe: Stable market (20% share). Germany, UK, France, Italy. Philips, Samsung, LG, Sony strong. Preference for European design aesthetics.

- Rest of World: Latin America, Middle East. Smaller but growing.

8. Conclusion

The smart ultra-thin TV market is positioned for strong growth through 2032, driven by consumer demand for sleek, wall-mountable designs, built-in streaming, and larger screen sizes. Stakeholders—from panel manufacturers to TV brands—should prioritize OLED and Mini-LED for premium contrast, optimize heat dissipation for ultra-thin form factors, and offer multiple smart OS options (webOS, Tizen, Google TV) for consumer preference. By enabling internet connectivity and built-in OS in ultra-thin designs, smart ultra-thin TVs have become the centerpiece of modern home entertainment.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

E-mail: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp