QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “IPM Motors- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global IPM Motors market, including market size, share, demand, industry development status, and forecasts for the next few years.

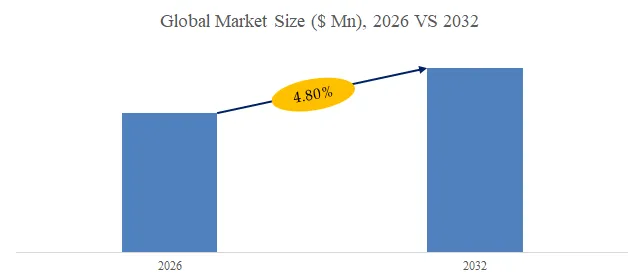

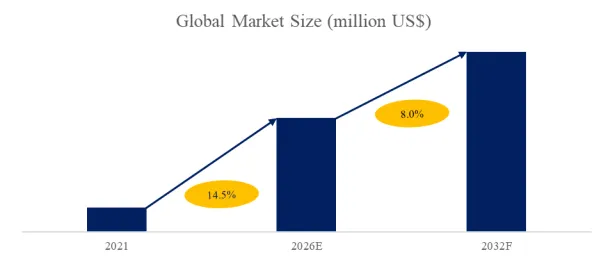

The global market for IPM Motors was estimated to be worth US$ 14670 million in 2025 and is projected to reach US$ 20010 million, growing at a CAGR of 4.6% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6073302/ipm-motors

IPM Market Summary

Intelligent Power Modules (IPMs) are best understood as highly integrated power-electronics building blocks that combine power switches, gate-drive circuitry, and core protection functions inside one module package for inverter and motor-drive systems. In commercial practice, the main product categories are IGBT-IPM, MOSFET-IPM, SiC-IPM, and GaN-IPM. Their application base is still centered on variable-speed motor control: Infineon positions CIPOS™ IPMs for roughly 20 W to 5 kW across dishwashers, fans, air conditioners, washing machines, refrigerators, air purifiers, HVAC, and industrial drives; onsemi positions IPMs for consumer, industrial, and automotive applications across about 50 W to 10 kW; ST’s SLLIMM family targets appliance and industrial motor drives; and TI’s 650 V three-phase GaN IPM shows that the category is now extending into next-generation high-efficiency motor platforms. From an industry-chain perspective, upstream is mainly power semiconductor dies, driver/control ICs, and packaging materials; midstream is module design, manufacturing, packaging, testing, and application support by IDMs and module specialists; downstream is concentrated in home appliances, industrial control, automotive systems, and selected energy or specialty equipment.

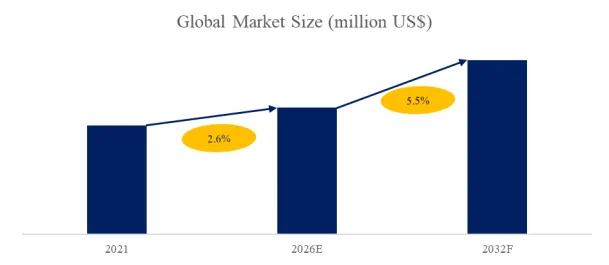

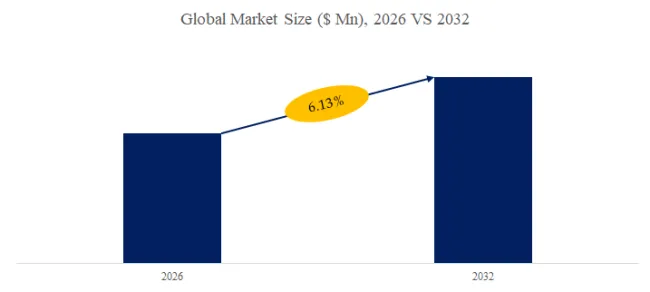

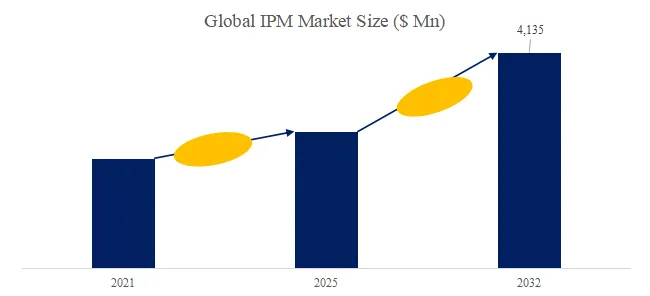

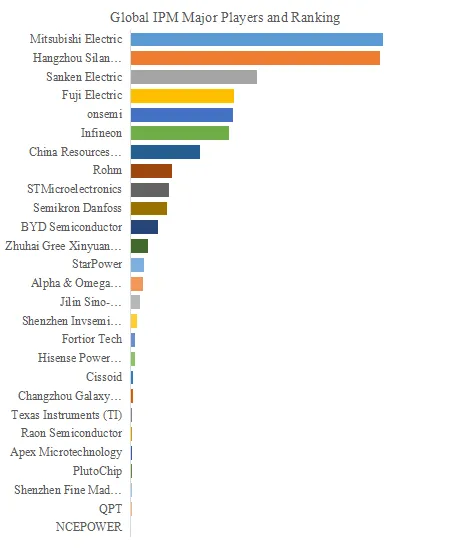

The global IPM market grows from US$2.108 billion in 2021 to US$4.135 billion in 2032, which indicates a solid medium-term expansion path while the internal market mix is changing. IGBT-IPM remains the dominant product type throughout the forecast period, but its revenue share declines from 93.25% in 2021 to 85.82% in 2032, while MOSFET-IPM gains share and SiC-/GaN-IPM move from niche positions into visible commercialization. By application, home appliances remain the largest demand base, but automotive is the strongest growth engine, and industrial control stays as a stable second pillar. Competition is also being reshaped: in the supplied dataset, Mitsubishi Electric leads the market in the early years, but by 2026 Silan Micro rises to the top position, while China Resources Microelectronics also expands rapidly, indicating that the market is shifting from a historically Japan/Western-led structure toward a dual-pole pattern combining global incumbents and fast-scaling Chinese suppliers. That market evolution is consistent with what leading suppliers are doing in practice: Mitsubishi Electric has launched Full-SiC and Hybrid-SiC SLIMDIP samples for appliances, onsemi has introduced 1200 V SiC SPM 31 IPMs, TI has commercialized a 650 V three-phase GaN IPM, and Infineon is pushing more integrated motor-control-plus-IPM platforms through iMOTION™.

At the regional and strategic level, our report shows an especially sharp production shift toward China, while Japan, Europe, and North America lose share over time; this implies that the industry’s manufacturing center of gravity is moving decisively into China even as Europe and Japan remain important for high-specification demand and technology benchmarking. The main growth drivers are also clear. First, regulatory pressure on electric motors and variable-speed drives supports continued inverter penetration, especially in HVAC and industrial systems under frameworks such as EU Ecodesign Regulation 2019/1781. Second, electric-vehicle growth is broadening IPM demand from traction-adjacent systems into compressors, pumps, fans, onboard charging peripherals, and thermal management; the IEA reports that global electric-car sales exceeded 17 million in 2024, surpassing 20% of new-car sales. Third, industrial automation remains a major structural driver: IFR reports 542,076 industrial robots were installed globally in 2024. Fourth, home appliances and heat pumps remain the industry’s most stable volume base, and suppliers such as onsemi explicitly position IPMs as key components in inverter compressors and fans for heat-pump systems. Taken together, the global IPM industry is moving toward higher integration, smaller packages, more software/tool support, and a gradual widening from silicon-dominated mass markets toward SiC and GaN in higher-efficiency and higher-power-density applications, while future growth will be increasingly determined by automotive electrification, industrial automation, appliance/HVAC inverter upgrades, and the continued build-out of China’s domestic supply chain.

According to the new market research report “Global Intelligent Power Modules (IPM) Market Report 2025-2031”, published by QYResearch, the global Intelligent Power Modules (IPM) market size is projected to reach USD 4.13 billion by 2032, at a CAGR of 6.2% during the forecast period.

Figure00001. Global IPM Market Size (US$ Million), 2020-2031

Above data is based on report from QYResearch Semiconductor Research Center: Global IPM Market Report 2025-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

Figure00002. Global IPM Top 27 Players Ranking and Market Share (Ranking is based on the revenue of 2024, continually updated)

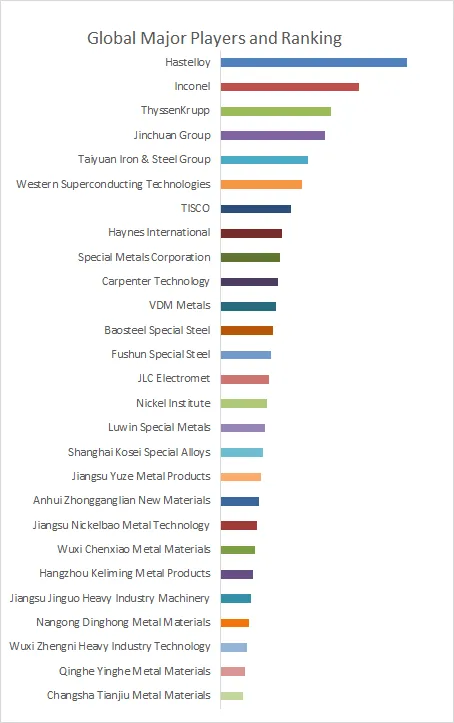

Above data is based on report from QYResearch Semiconductor Research Center: Global IPM Market Report 2025-2031 (published in 2025). If you need the latest data, plaese contact QYResearch.

According to QYResearch, the global key manufacturers of Intelligent Power Modules (IPM) include Mitsubishi Electric, Hangzhou Silan Microelectronics, Sanken Electric, Fuji Electric, onsemi, Infineon, China Resources Microelectronics Limited, Rohm, STMicroelectronics, Semikron Danfoss, etc. in 2025, the global top 10 players had a share approximately 86.0% in terms of revenue.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The IPM Motors market is segmented as below:

By Company

Nidec

Yaskawa

Nissei Corporation

VARCHEA

Reuland

Lafert Melbourne

DAIKIN

e+a Elektromaschinen und Antriebe

Benevelli

MAHLE

Inovance

14668.058

Segment by Type

1-25 KW

25-100 KW

100-300 KW

Above 300 KW

Segment by Application

Automobile

HVAC

Others

Each chapter of the report provides detailed information for readers to further understand the IPM Motors market:

Chapter 1: Introduces the report scope of the IPM Motors report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of IPM Motors manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various IPM Motors market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of IPM Motors in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of IPM Motors in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth IPM Motors competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides IPM Motors comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides IPM Motors market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global IPM Motors Market Outlook, In‑Depth Analysis & Forecast to 2032

Global IPM Motors Market Research Report 2026

Global IPM Motors Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Brushless IPM Motors Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp