QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report “Compensation Wire Rope- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032”. Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2026-2032), this report provides a comprehensive analysis of the global Compensation Wire Rope market, including market size, share, demand, industry development status, and forecasts for the next few years.

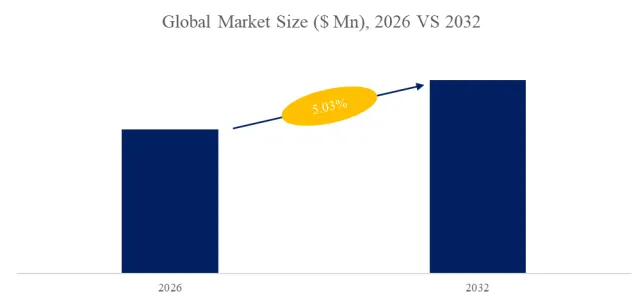

The global market for Compensation Wire Rope was estimated to be worth US$ 380 million in 2025 and is projected to reach US$ 525 million, growing at a CAGR of 4.8% from 2026 to 2032.

【Get a free sample PDF of this report (Including Full TOC, List of Tables & Figures, Chart)】

https://www.qyresearch.com/reports/6034524/compensation-wire-rope

Compensation wire rope is a key component used in vertical transportation equipment such as elevators and cranes. It is mainly used to compensate for the weight difference between the elevator car and the counterweight, ensuring that the elevator can maintain a stable and effective balance during operation. Its core function is to avoid abnormal operation of the elevator due to uneven load by compensating for load changes in the system, thereby improving the efficiency and safety of the elevator.

According to the latest QYResearch report, the global COMPENSATION WIRE ROPE market is expected to reach US$ 380 million in 2025, with a compound annual growth rate (CAGR) of 4.8%.

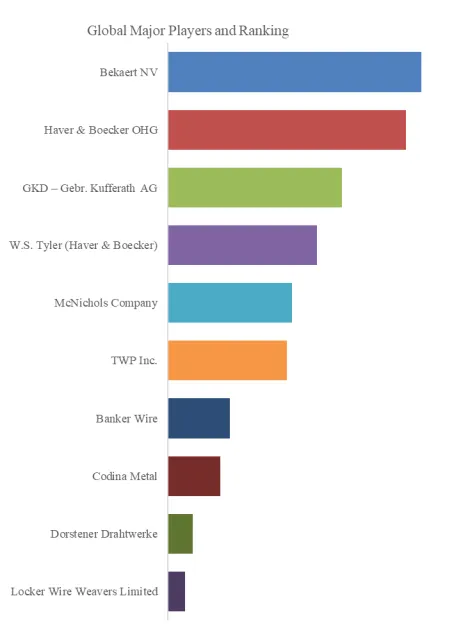

Manufacturing companies include Teufelberger-Redaelli, ArcelorMittal, Haggie, IPH Global, Kiswire, Bridon-Bekaert, DSR Wire, Gustav Wolf, Brugg, Usha Martin, Jiangsu Shenwang, Guizhou Wire Rope, BOMCO Steel Tube & Wire Rope, Juli Sling, Goldsun, Shanghai Junwei Steel Rope, Hubei Fuxing, Fasten Steel Rope, Dipa Steel Rope, Goldsun Wire Rope.

|

Company Name |

Description |

|

ArcelorMittal |

ArcelorMittal is one of the world’s largest steel groups, with operations spanning steelmaking and downstream long products, flat products, wire rod and processed wire solutions—providing a strong base for vertical integration across the “wire rod → wire → wire rope/specialty wire” value chain. Company information shows ArcelorMittal ROPES as a wire-rope unit supplying premium wire ropes for hoisting, mining, ropeways and mooring, highlighting corrosion-resistant and technologically advanced rope offerings. From an industry perspective, such integration typically supports tighter raw-material quality control, process consistency, and global engineering support and delivery capabilities. |

|

Haggie |

Haggie is a manufacturer whose core product is wire rope. Its products cover a wide range of applications including mining hoisting (including deep/vertical shaft mining wire rope), offshore oil and gas, lifting, fisheries, and general applications. The company emphasizes its “long-standing experience and large-scale production in the mining hoisting sector.” Typical capabilities of the manufacturer include: structural design and material selection for high-fatigue conditions, control of twisting and heat treatment/surface treatment processes in manufacturing, and customer-facing selection guidance, life prediction, and on-site technical services (especially common in the mining and heavy-duty sectors). |

|

Juli Sling |

For nearly 40 years, Juli Sling has redefined excellence as a China leader supplier of lifting and rigging equipment, delivering lifting slings, wire rope slings, ratchet straps, vessels ropes, shackle, chain, hook&ring, elevator link to industries where safety and reliability are critical—energy, infrastructure, defense, and maritime engineering. |

|

Safety Group |

SAFETY GROUP, formerly known as the state-owned Wuxi Steel Wire Rope Factory established in 1958, was listed on the Shanghai Stock Exchange in 2016 with the stock code: 603028. In 2019, Suzhou Wuzhong State-owned Assets participated in the holding. The company currently has 14 holding subsidiaries and has established multiple industrial cooperation bases across the country, mainly in Wuxi, Suzhou, Xuzhou, Chuzhou, Guangzhou, Changsha, Hong Kong, and other places. The business covers: steel wire ropes for elevators and construction machinery, solar cell, architectural design, EPC general contracting, rigging and lifting straps, and inspection and testing of special equipment. |

COMPENSATION WIRE ROPE Value Chain

Source: Secondary Sources, Expert Interviews and QYResearch, 2025

The upstream of the compensation wire rope industry chain is centered on steel billets and high-strength steel wire raw materials. Typical upstream raw material suppliers are large steel companies (global/regional representative suppliers include Baowu/Baosteel (China Baowu), ArcelorMittal, POSCO, etc.). These companies determine the grade and price fluctuations of steel wire raw materials; the midstream is the wire rope processing and rope-forming companies, which are responsible for wire drawing, rope strand design, braiding and surface treatment, and provide customized compensation ropes and inspection and maintenance services. Internationally renowned manufacturers include Bekaert (Belgium), Usha Martin (India), and KISWIRE (South Korea). Domestically, there are a large number of provincial state-owned enterprises and private professional wire rope factories that undertake midstream production and local customization (these companies mainly meet the engineering-level needs of bridges, ports, lifting, mining and wind power fields); downstream applications cover power, bridge and rail engineering, port lifting, mining and oil and gas platforms, wind power foundations and large machinery manufacturers. Typical downstream customers include power and infrastructure general contractors, lifting equipment manufacturers (such as Liebherr, domestic large lifting manufacturers), power and wind power equipment suppliers (such as Siemens Gamesa the key to upstream and downstream collaboration lies in raw material quality inspection, product standardization, third-party testing and certification, and long-term operation and maintenance services. These factors influence each other and jointly determine the ultimate project safety and lifecycle cost.

Market Drivers:

Key demand drivers come from high-rise and high-speed/long-travel elevators that require better balance, energy stability, and ride quality. Compensation ropes are used to balance the weight of hoist ropes and traveling cables across the travel path, helping maintain more stable tension and dynamic behavior—reducing vibration, improving energy efficiency, and enhancing ride comfort. In parallel, stringent elevator rope manufacturing/testing requirements reinforce attention to proper specification and replacement of compensation systems during modernization and maintenance cycles.

Restraint:

Restraints are driven by the combination of high-performance requirements, cost sensitivity, and long validation/retrofit cycles. In the hoistway, compensation ropes experience repeated bending, abrasion, vibration, and tension variation, influenced by humidity, lubrication, and contamination—demanding strong fatigue life, wear resistance, and dimensional stability. At the same time, the rope must fit existing traction, tensioning, and guidance designs; changes in construction/diameter/termination can trigger system-level checks and add field complexity, increasing modernization costs and extending replacement cycles—making buyers highly sensitive to price and downtime windows.

Opportunity:

Opportunities are supported by (1) elevator modernization cycles tied to urban renewal, especially in markets with large installed high-rise bases; (2) system-level optimization aimed at better ride comfort and lower energy use, creating value beyond the rope itself through engineering support around tensioning and traveling-cable management; and (3) clearer requirements on tolerances, constructions, and testing under standards, which favors suppliers with stable processes and traceable quality—helping them enter qualified supply chains and secure recurring aftermarket demand.

Barriers to Entry:

Entry barriers are defined by standards compliance, engineering-grade consistency, and OEM/aftermarket qualification lock-in. Compensation ropes must meet minimum manufacturing and testing requirements and demonstrate verifiable performance in breaking strength, fatigue behavior, and dimensional tolerances with strong lot-to-lot consistency. Because selection is closely tied to elevator OEM and maintenance ecosystems, new suppliers typically face lengthy approval, field qualification, and reliability data accumulation before accessing scaled procurement. In addition, termination know-how, tensioning-system fitment, and installation/service capabilities create “hidden barriers” that determine whether a supplier can move from trial supply to repeatable engineering delivery.

The report provides a detailed analysis of the market size, growth potential, and key trends for each segment. Through detailed analysis, industry players can identify profit opportunities, develop strategies for specific customer segments, and allocate resources effectively.

The Compensation Wire Rope market is segmented as below:

By Company

Teufelberger-Redaelli

ArcelorMittal

Haggie

IPH Global

Kiswire

Bridon-Bekaert

DSR Wire

Gustav Wolf

Brugg

Usha Martin

Jiangsu Shenwang

Guizhou Wire Rope

BOMCO Steel Tube &Wire Rope

Juli Sling

Goldsun

Shanghai Junwei Steel Rope

Hubei Fuxing

Fasten Steel Rope

Dipa Steel Rope

Goldsun Wire Rope

Safety Group

Segment by Type

Galvanized Steel Core

Fiber Core

Others

Segment by Application

Elevator

Lifting Equipment

Others

Each chapter of the report provides detailed information for readers to further understand the Compensation Wire Rope market:

Chapter 1: Introduces the report scope of the Compensation Wire Rope report, global total market size (valve, volume and price). This chapter also provides the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry. (2021-2032)

Chapter 2: Detailed analysis of Compensation Wire Rope manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc. (2021-2026)

Chapter 3: Provides the analysis of various Compensation Wire Rope market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments. (2021-2032)

Chapter 4: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.(2021-2032)

Chapter 5: Sales, revenue of Compensation Wire Rope in regional level. It provides a quantitative analysis of the market size and development potential of each region and introduces the market development, future development prospects, market space, and market size of each country in the world..(2021-2032)

Chapter 6: Sales, revenue of Compensation Wire Rope in country level. It provides sigmate data by Type, and by Application for each country/region.(2021-2032)

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc. (2021-2026)

Chapter 8: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 9: Conclusion.

Benefits of purchasing QYResearch report:

Competitive Analysis: QYResearch provides in-depth Compensation Wire Rope competitive analysis, including information on key company profiles, new entrants, acquisitions, mergers, large market shear, opportunities, and challenges. These analyses provide clients with a comprehensive understanding of market conditions and competitive dynamics, enabling them to develop effective market strategies and maintain their competitive edge.

Industry Analysis: QYResearch provides Compensation Wire Rope comprehensive industry data and trend analysis, including raw material analysis, market application analysis, product type analysis, market demand analysis, market supply analysis, downstream market analysis, and supply chain analysis.

and trend analysis. These analyses help clients understand the direction of industry development and make informed business decisions.

Market Size: QYResearch provides Compensation Wire Rope market size analysis, including capacity, production, sales, production value, price, cost, and profit analysis. This data helps clients understand market size and development potential, and is an important reference for business development.

Other relevant reports of QYResearch:

Global Compensation Wire Rope Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Compensation Wire Rope Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Global Compensation Wire Rope Market Research Report 2026

Global Elevator Compensation Wire Rope Market Outlook, In‑Depth Analysis & Forecast to 2032

Global Elevator Compensation Wire Rope Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

Elevator Compensation Wire Rope- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

Global Elevator Compensation Wire Rope Market Research Report 2026

About Us:

QYResearch founded in California, USA in 2007, which is a leading global market research and consulting company. Our primary business include market research reports, custom reports, commissioned research, IPO consultancy, business plans, etc. With over 19 years of experience and a dedicated research team, we are well placed to provide useful information and data for your business, and we have established offices in 7 countries (include United States, Germany, Switzerland, Japan, Korea, China and India) and business partners in over 30 countries. We have provided industrial information services to more than 60,000 companies in over the world.

Contact Us:

If you have any queries regarding this report or if you would like further information, please contact us:

QY Research Inc.

Add: 17890 Castleton Street Suite 369 City of Industry CA 91748 United States

EN: https://www.qyresearch.com

Email: global@qyresearch.com

Tel: 001-626-842-1666(US)

JP: https://www.qyresearch.co.jp